Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

642 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Investment

Market Analysis

Global

Europe

Funding

Mergers & Acquisitions

Game Publishing

Game Development

Japan

PC

Console

Mobile

Germany

UK

Monetization

Employment

France

IPO

Clear

Filters

1

Investment

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

17 pages

Console/PC Games Investment Report September 2024

The 2023 fiscal year saw total deal value reach $69.5 billion, a 612% increase driven almost entirely by Microsoft’s $68.7 billion acquisition of Activision Blizzard.

While total deal value surged, the actual number of transactions fell by 25% compared to 2022, and investment volume dropped to $627.8 million across 161 deals.

M&A activity dominated the market with $68.8 billion across 39 deals, accounting for more than 99% of North American M&A value.

Investment

Mergers & Acquisitions

Global

+2

DDM

Sept 2024

Report

145 pages

State of Web3 in Saudi Arabia

Saudi Arabia captured 51% of all MENA Web3 venture capital funding in Q1 2024, totaling $429 million across 163 deals.

The government has committed $37.7 billion to esports and $13.3 billion to gaming, supported by major investment vehicles like Wa’ed’s $500 million fund and 500 Global’s $2.4 billion under management.

While the market is currently concentrated in consumer-facing sectors like DeFi, GameFi, and SocialFi, there is a significant supply gap for foundational infrastructure development.

Web3

Blockchain

Investment

+2

Adaverse

Jul 2024

Report

1 pages

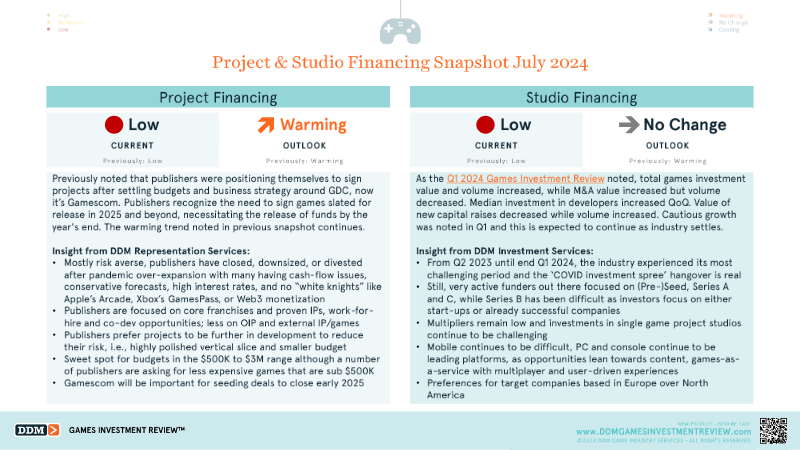

Project & Studio Financing Snapshot July 2024

Publishers are prioritizing low-risk projects with budgets between $500k and $3 million, though there is an emerging demand for titles under $500k.

Investment is heavily skewed toward early-stage (pre-seed/Series A) and late-stage (Series C) rounds, leaving Series B financing scarce.

Funding trends show a shift toward smaller, more frequent capital raises, evidenced by a decline in total new capital value despite an increase in deal count.

Investment

Funding

Market Analysis

+1

DDM

Jul 2024

Report

6 pages

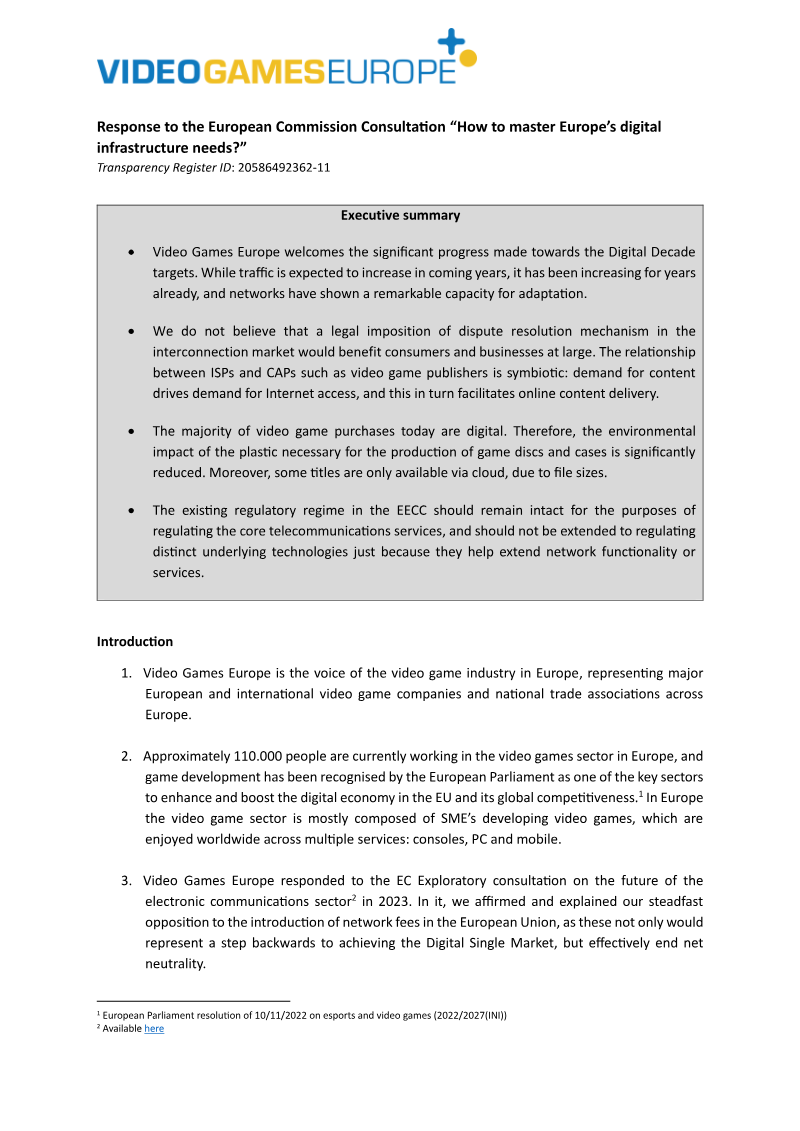

How to Master Europe’s Digital Infrastructure Needs?

Video Games Europe opposes new network fees or expanded regulation of cloud services, arguing these measures would threaten net neutrality, increase consumer costs, and damage European digital competitiveness.

The European video game industry generates €24.5 billion in annual revenue and employs approximately 110,000 people, with 53 percent of the European population participating in gaming.

Gaming traffic is significantly lower than video streaming, with typical online gameplay consuming 60–80 megabytes per hour and high-intensity titles rarely exceeding 300 megabytes per hour.

Europe

Cloud Gaming

Streaming

+3

Video Games Europe

Jun 2024

Report

15 pages

Mobile Games Annual Investment Report

Venture capital in 2023 prioritized early-stage mobile gaming ventures, specifically those integrating blockchain technology and decentralized infrastructure.

Andreessen Horowitz led investment activity by deploying 63 million dollars across eight deals, including a 33 million dollar seed round for Proof of Play.

Investment focus remained diverse, spanning social gaming, AI-driven development, and fantasy sports, exemplified by Lumikai’s 22 million dollar investment in Eloelo.

Investment

Market Analysis

Global

+1

DDM

Jun 2024

Report

19 pages

Q2'24 Gaming Deals Report: Gradual Recovery

Steam full-game sales grew 27% year-over-year in Q2 2024, driven primarily by strong performance from independent and mid-sized titles.

Asia led global early-stage investment with $320 million across 28 deals, while North America dominated late-stage venture capital with $239 million across seven deals.

BITKRAFT was the most active early-stage investor by volume with 18 rounds, while a16z Games led in total deal value with $124 million invested.

Market Analysis

Investment

Mergers & Acquisitions

+1

InvestGame

Jun 2024

Report

19 pages

Q2’24 Gaming Deals Report

Private investment in the gaming industry reached a new quarterly benchmark of $1 billion across 116 rounds in Q2 2024, signaling a stabilization of the market.

Steam full-game sales grew by 27% year-over-year, driven primarily by a strong performance from indie and AA titles.

Early-stage venture capital is fueling current market activity, while late-stage deal-making remains sluggish due to persistent economic headwinds.

Investment

Mergers & Acquisitions

Market Analysis

+1

InvestGame

Jun 2024

Presentation

15 pages

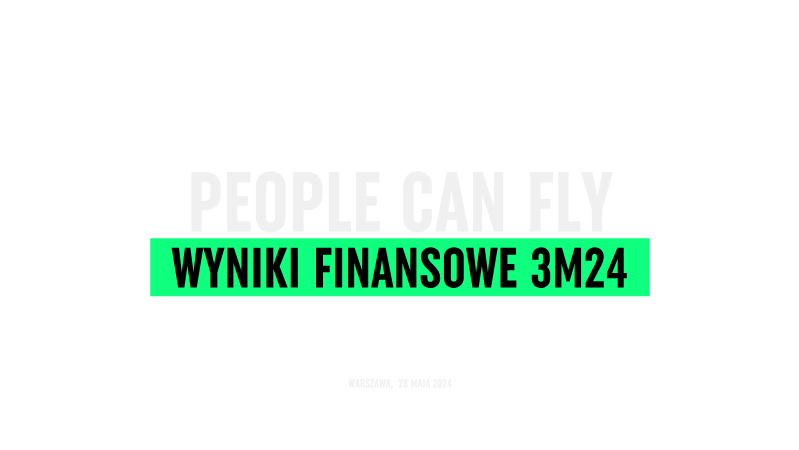

Financial Results Q1 2024

PCF Group achieved a net profit of 11.0 million PLN in Q1 2024, a significant turnaround from the 0.9 million PLN net loss recorded in Q1 2023.

Quarterly revenue grew to 56.9 million PLN, up from 34.9 million PLN in the prior year, driven by the release of Bulletstorm VR and progress on Project Maverick.

EBITDA rose to 11.0 million PLN, compared to 3.0 million PLN in Q1 2023, reflecting a disciplined cost approach alongside higher revenue.

Market Analysis

Investment

Europe

+1

PCF Group

May 2024

Report

49 pages

State of Play: Spring Edition

Mobile gaming is the industry's primary growth engine, with 1.9 billion players and projected annual revenue of $118 billion by 2027.

Regulatory changes like the EU's Digital Markets Act are dismantling app store walled gardens, enabling developers to bypass standard commission fees through alternative billing and direct-to-consumer commerce.

Cross-platform play is now a standard expectation, with 87% of multiplayer gamers participating and developers increasingly integrating 5G and mobile wallets to facilitate unified 'cross-pay' ecosystems.

Market Analysis

Investment

Mobile

+1

Xsolla

Mar 2024

Report

43 pages

Keywords Studios FY 2023 Results

Keywords Studios reported €780 million in revenue for 2023, representing 13% total growth and 9% organic growth despite currency headwinds and U.S. labor strikes.

The company achieved an adjusted operating margin of 15.6% and an EBITDA of €158.3 million, supported by a strong cash conversion rate of 82.3%.

Management is pursuing a revenue target exceeding €1 billion, supported by a €225 million investment in five acquisitions during 2023 and a $400 million revolving credit facility.

Market Analysis

Mergers & Acquisitions

Investment

+1

Keywords Studios

Mar 2024

Report

64 pages

Blockchain Game Alliance: State of the Industry 2024

The blockchain gaming industry is shifting from speculative models to 'fun-first' development, with 71% of professionals identifying player asset ownership as the primary value proposition.

Mainstream adoption is being driven by the entry of traditional giants like Sony and Ubisoft, though 66.3% of practitioners still cite public perceptions of scams as a significant barrier.

Operational barriers like onboarding complexity and poor user experience remain the top hurdles to mainstream growth, despite a notable decrease in the severity of these concerns since 2023.

Market Analysis

Blockchain

Investment

+1

Blockchain Game Alliance

Jan 2024

Report

27 pages

Global Sports Tech Report 2024

The provided source text contains no factual data, metrics, or findings from the Global Sports Tech Report 2024.

The content consists solely of a request for additional information rather than report substance.

No specific growth rates, company names, or dates are available to summarize.

Market Analysis

Mergers & Acquisitions

Investment

+1

Drake Star Partners

Jan 2024

Report

30 pages

Gaming Industry Report: Q4 2023

The global gaming industry reached a $184 billion valuation in 2023, reflecting a modest year-over-year growth of 0.6%.

Venture funding for the gaming sector dropped 33% quarter-over-quarter in Q4 2023 to $308 million, signaling a return to pre-pandemic capital levels.

Approximately 10,500 industry layoffs occurred in 2023 as companies prioritized operational efficiency, asset consolidation, and high-retention projects.

Market Analysis

Investment

Funding

+2

Konvoy

Jan 2024

Report

11 pages

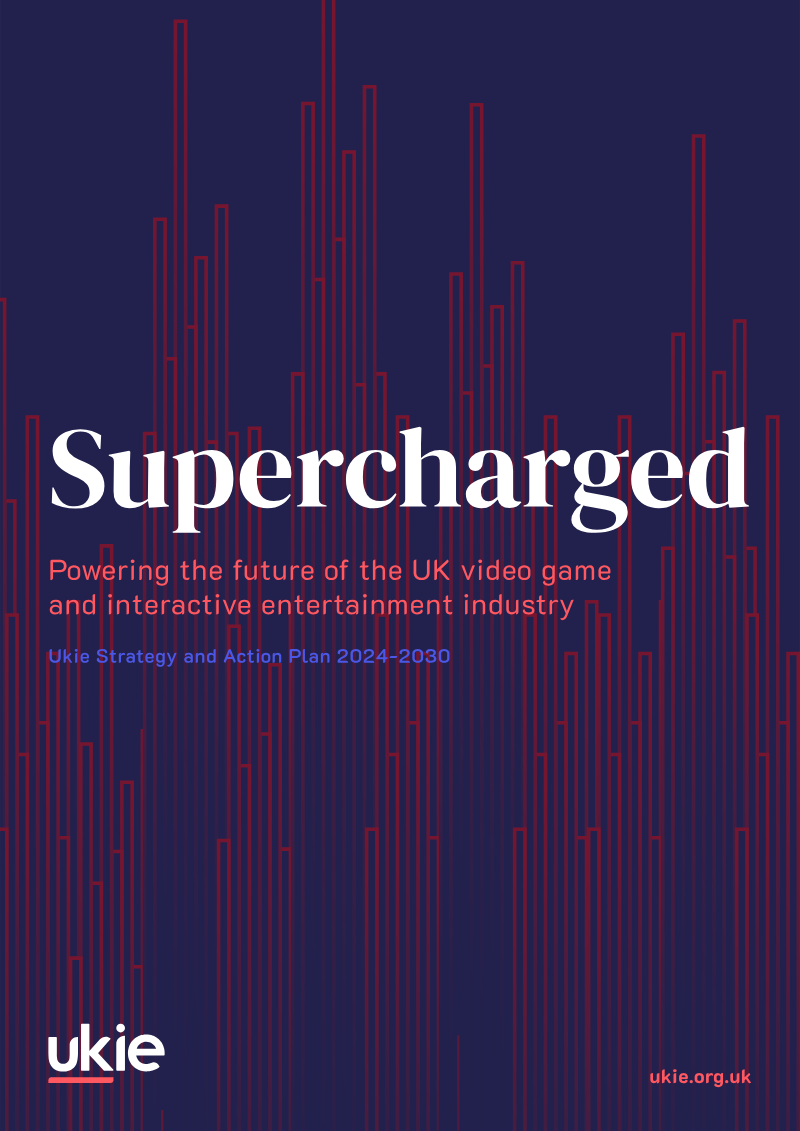

Supercharged: Powering the Future of the UK Video Game and Interactive Entertainment Industry

The UK video game industry has launched a five-year strategy aiming to establish the nation as the global leader in intellectual property and innovation by 2030.

The 2024-25 action plan prioritizes lobbying for more competitive tax reliefs, increased investment, and the introduction of a Digital Creativity GCSE.

Strategic efforts to strengthen the workforce include the expansion of the #RaiseTheGame diversity, equity, and inclusion programme and the creation of a sector-wide skills network.

Market Analysis

Marketing

Investment

+1

Ukie

Jan 2024

Report

6 pages

The Alumni Effect: A Deep Dive into Studios Founded by Ex-Rioters

Startups founded by former Riot Games employees have raised nearly $500 million across 27 companies since 2020.

Ex-Riot founders command a 53% premium in average round size, securing $11 million per round compared to the $7 million industry average.

Venture capital firms Andreessen Horowitz and Bitkraft Ventures are the primary backers, participating in deals worth $339.3 million and $236.3 million respectively.

Investment

Funding

Market Analysis

+1

InvestGame

Jan 2024

Report

33 pages

Q1 2024 Gaming Deals Report

The gaming industry is shifting toward disciplined, long-term profitability as high interest rates and macroeconomic pressures reduce late-stage financing and public listing activity.

Over $15 billion in dry powder remains available across more than 65 gaming-focused funds, ensuring a steady pipeline for early-stage seed investments despite broader capital constraints.

PC and console sectors show resilience through strong independent studio performance and consistent engagement on platforms like Steam, while mobile gaming faces a contraction due to privacy-related advertising headwinds.

Market Analysis

Mergers & Acquisitions

Investment

+2

InvestGame

Jan 2024

Report

24 pages

From Volatility to Stability: Q3 2024 Gaming Deals Report

The gaming industry has transitioned to a normalized market environment, with Q3 2024 private investment totaling approximately $1 billion across 120 rounds.

AA and indie publishers are outperforming the broader market, driving a 35% year-over-year growth in gross revenue while AAA titles remain stagnant.

Investor capital is shifting away from traditional content toward infrastructure, payment systems, and development tools.

Market Analysis

Mergers & Acquisitions

Investment

+3

InvestGame

Jan 2024

Report

44 pages

Annual Report 2024

Thunderful Group reported a net loss of SEK 887.5 million in 2024, driven by SEK 444 million in asset impairments and significant restructuring costs that resulted in an operating margin of -46.9%.

The company executed a major strategic pivot toward a pure gaming focus, involving a 20% workforce reduction and the divestment of non-gaming assets to halve interest-bearing net debt.

Net revenue declined 23.8% to SEK 292.8 million, while adjusted EBITA fell to a loss of SEK 383.9 million as the firm transitioned toward higher-margin publishing and co-development models.

Market Analysis

Investment

Diversity & Inclusion

+1

Thunderful

Jan 2024

Report

4 pages

2024 Netflix’s Growth Strategy and Investment Trends in the Korean Market

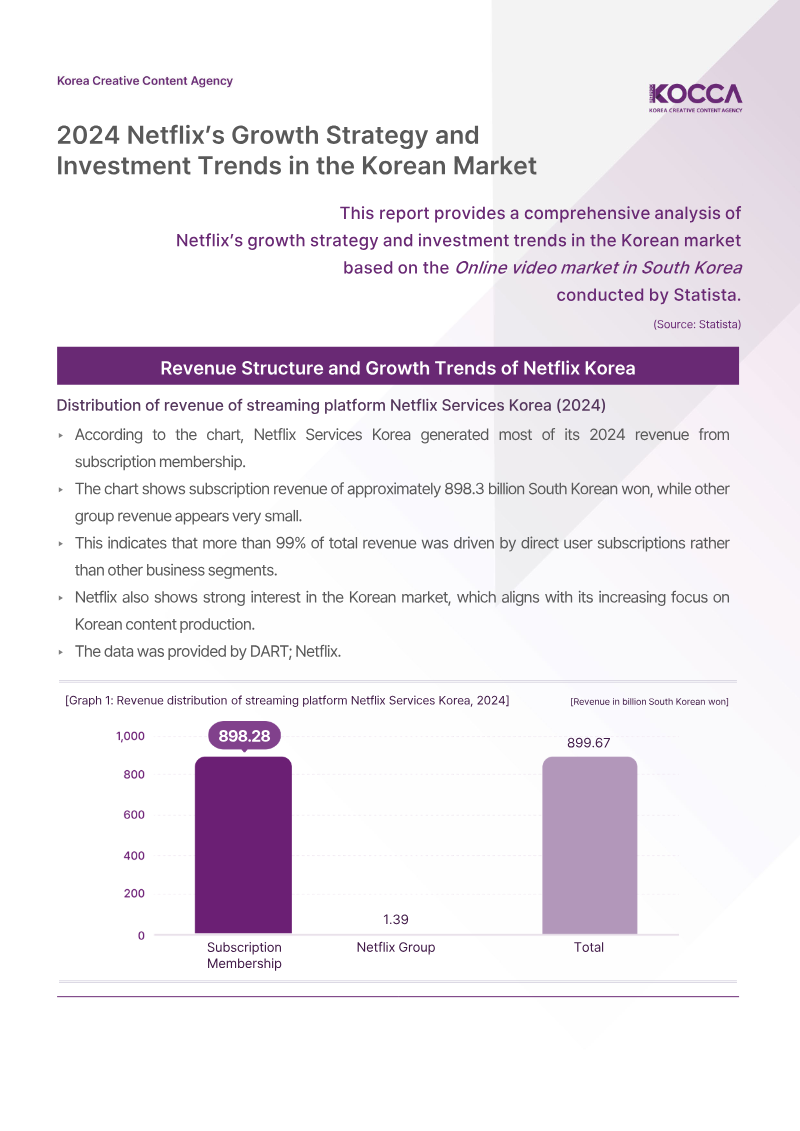

Netflix’s streaming revenue in South Korea grew more than five-fold between 2019 and 2024, rising from approximately 175.6 billion won to 898.3 billion won.

The company’s revenue model in South Korea is highly concentrated, with over 99% of income generated directly from user subscriptions.

Annual investment in Korean content saw a massive escalation, climbing from 15 billion won in 2016 to a peak of 550 billion won in 2021.

Investment

Streaming

Market Analysis

+1

KOCCA – Korea Creative Content Agency

Jan 2024

Report

72 pages

Serbian Gaming Industry Report 2023

The Serbian gaming industry generated €175 million in revenue in 2023, marking a 17% year-on-year increase.

The sector's workforce nearly doubled to approximately 4,300 professionals, supported by talent inflows from Russia, Ukraine, and Belarus.

The ecosystem now includes 38 active studios producing 81 titles, with a strategic shift occurring from mobile-first games toward core and original-IP projects.

Market Analysis

Monetization

Investment

+1

SGA

Jan 2024

Previous

1

…

27

28

29

…

33

Next