ReportKOCCA – Korea Creative Content Agency

2024 Netflix’s Growth Strategy and Investment Trends in the Korean Market

1 Jan 20244 pages~5 min full read

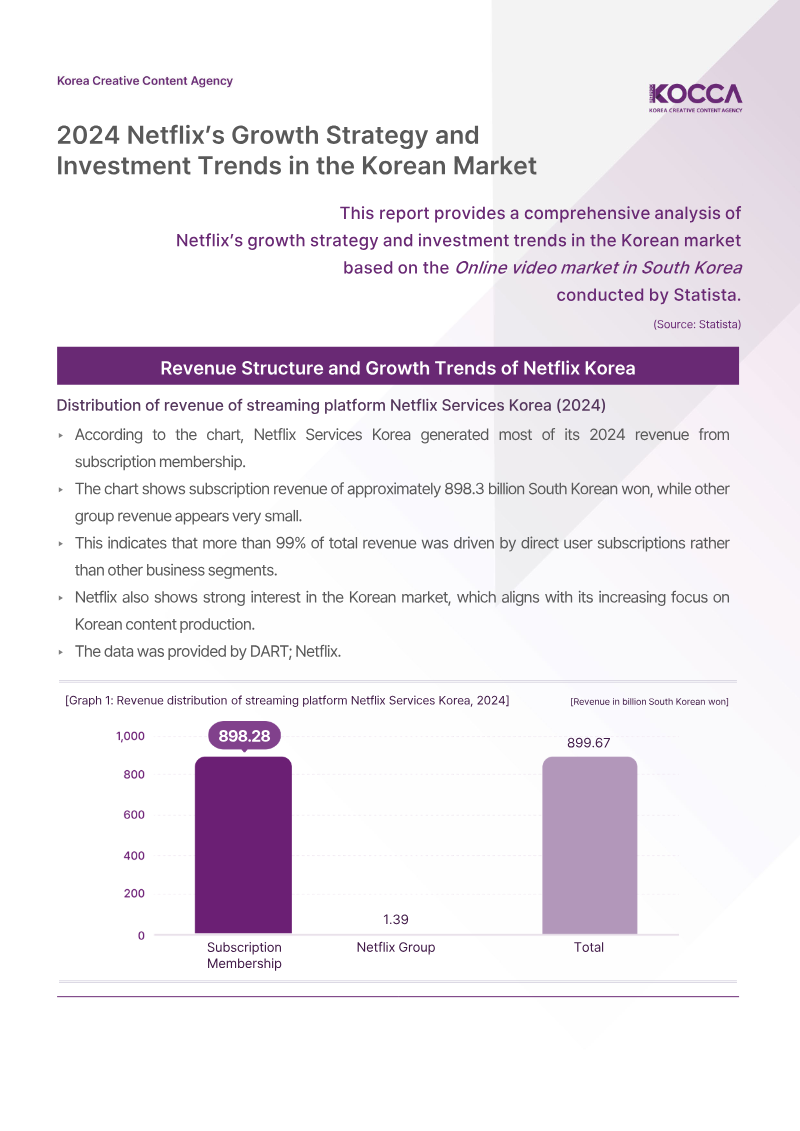

Netflix’s streaming revenue in South Korea grew more than five-fold between 2019 and 2024, rising from approximately 175.6 billion won to 898.3 billion won.

The company’s revenue model in South Korea is highly concentrated, with over 99% of income generated directly from user subscriptions.

Annual investment in Korean content saw a massive escalation, climbing from 15 billion won in 2016 to a peak of 550 billion won in 2021.

Netflix’s most rapid revenue growth occurred between 2020 and 2022, followed by a transition to a period of steadier, moderate expansion through 2024.

In 2020 alone, Netflix invested approximately 333 billion won into local productions to drive subscriber acquisition and retention.

The analysis evaluates Netflix’s strategic expansion and capital allocation within South Korea’s online video market, emphasizing how subscription‑driven revenue and localized content investment shape the company’s growth trajectory. By charting financial performance from 2019 through 2024, the study demonstrates that Netflix’s streaming revenue in the country surged from roughly 175.6 billion won to 898.3 billion won, a more than five‑fold increase that underscores a robust market penetration. Over 99 % of this income derives from direct user subscriptions, indicating an extremely concentrated revenue structure with minimal reliance on ancillary business lines.

Revenue growth exhibits a distinct phase pattern: the most pronounced acceleration occurred between 2020 and 2022, followed by a period of steadier, moderate expansion through 2023 and 2024. This temporal dynamic aligns with a parallel escalation in content spending, where annual investment in Korean productions rose from 15 billion won in 2016 to a peak of 550 billion won in 2021. Notably, 2020 alone saw an outlay of approximately 333 billion won, reflecting Netflix’s intensified focus on locally produced dramas and films to attract and retain subscribers.

The scope of the assessment is confined to the South Korean streaming sector, covering the years 2016‑2024 and drawing on secondary data from Statista, DART filings, and Korea Eximbank. The methodology relies on quantitative trend analysis of disclosed revenue figures and investment amounts, enabling a clear view of how subscription reliance and targeted content funding have jointly propelled Netflix’s market foothold in Korea.