ReportDDM

Project & Studio Financing Snapshot July 2024

1 Jul 20241 pages~2 min full read

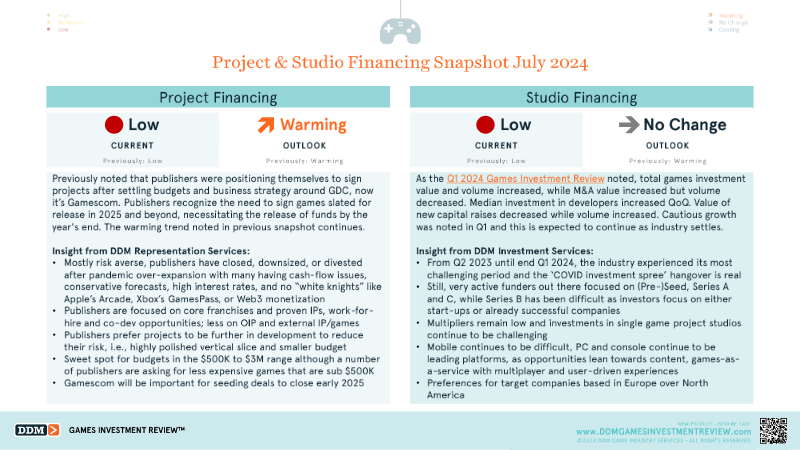

Publishers are prioritizing low-risk projects with budgets between $500k and $3 million, though there is an emerging demand for titles under $500k.

Investment is heavily skewed toward early-stage (pre-seed/Series A) and late-stage (Series C) rounds, leaving Series B financing scarce.

Funding trends show a shift toward smaller, more frequent capital raises, evidenced by a decline in total new capital value despite an increase in deal count.

PC and console titles—specifically those featuring games-as-a-service, multiplayer, or user-generated content—are currently prioritized over mobile projects.

Investors are showing a geographic preference for European-based studios over North American counterparts.

Despite a volatile Q1 2024, the overall financing environment remains constrained, with publishers focusing on core franchises and proven IP to mitigate post-pandemic cash-flow pressures.

The snapshot evaluates financing conditions for game projects and development studios as of mid‑2024, highlighting a persistently constrained capital environment while noting modest signs of warming in project funding. Publishers remain risk‑averse after pandemic‑driven over‑expansion, with many having reduced staff, divested assets, and facing cash‑flow pressures compounded by high interest rates and the absence of large platform backers. Consequently, they prioritize core franchises, proven IP and work‑for‑hire arrangements, demanding projects that are further along in development, feature polished vertical slices, and fall within a budget sweet spot of roughly $500 k to $3 million, though an emerging demand for sub‑$500 k titles is evident. The upcoming Gamescom event is expected to catalyze deal flow for releases slated for 2025 and beyond.

Studio financing remains low with no change in outlook, reflecting cautious growth after a volatile Q1 2024 period in which total investment value and volume rose, M&A value increased while deal count fell, and median developer investment grew quarter‑over‑quarter. New capital raises saw a decline in total value but an increase in deal count, underscoring a shift toward smaller, more frequent funding rounds. Investors continue to focus on early‑stage (pre‑seed, Series A) and later‑stage (Series C) opportunities, while Series B financing proves scarce as capital gravitates toward either nascent start‑ups or already successful entities.

Geographically, funders exhibit a preference for European‑based studios over North American counterparts, and platform trends show mobile projects facing heightened difficulty, whereas PC and console titles dominate, especially those built around games‑as‑a‑service, multiplayer, and user‑generated content models. Overall, the financing landscape is characterized by conservative publisher behavior, modest but steady studio investment, and a strategic emphasis on later‑stage, lower‑risk projects as the industry settles post‑pandemic.