Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

63 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Streaming

Global

Market Analysis

Esports

PC

Mobile

Marketing

MOBA

Southeast Asia

Player Behavior

First-Person Shooter

Europe

Cloud Gaming

Battle Royale

Monetization

Advertising

South Korea

India

Clear

Filters

1

Streaming

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

13 pages

Interview with Sarah Chung, Senior Manager at Disney Company

The global success of Korean content is driven by a 'cocreator' fandom model, where streaming platforms leverage seamless localization tools to allow audiences to actively participate in cultural moments.

Korean productions must now compete for attention against both traditional OTT platforms and short-form ecosystems like TikTok and YouTube, necessitating a shift in how content is marketed and consumed.

To maintain global reach, studios must adopt a dual strategy of utilizing platforms with extensive international footprints while executing aggressive off-platform promotional campaigns.

Streaming

Market Analysis

USA

KOCCA – Korea Creative Content Agency

Jan 2025

Report

11 pages

Crypto on Live Streaming Mini‑Report

The number of unique crypto-focused streaming channels doubled in the six months leading to late 2024, with YouTube channels surging from 31 in July 2024 to over 200 by June 2025.

India has become a primary hub for crypto content, hosting four of the top ten global creators who stream primarily on YouTube.

Bitcoin remains the most discussed asset with over 500,000 chat mentions in the first half of 2025, while Solana has emerged as the dominant secondary interest with 171,000 mentions.

Streaming

Market Analysis

Cross-Platform

+3

Stream Hatchet

Nov 2024

Report

20 pages

Live Streaming Trend Report: Q3 2024

Total live-streaming viewership reached 8.5 billion hours in Q3 2024, marking a 12 percent year-over-year increase.

Kick emerged as the third-largest streaming platform with 534 million hours watched, representing a 103 percent growth rate and a 6.3 percent market share.

Twitch experienced a 4 percent decline in viewership during Q3 2024, even as it hosted record-breaking subscriber events like ironmouse’s 320,000-follower marathon.

Streaming

Market Analysis

Player Demographics

+1

Stream Hatchet

Sept 2024

Report

20 pages

Live Streaming Trends Report: Q2 2024

The live streaming industry saw a 10% year-over-year growth in Q2 2024, reaching 8.5 billion total hours watched.

Twitch's market share dropped from 70% to 60%, while YouTube Gaming and Kick captured 23.4% and 5.5% of the market, respectively.

Viewership is decentralizing, with the top 5% of streamers now holding 86% of the market share, down from 98% in 2019.

Streaming

Market Analysis

Player Demographics

+1

Stream Hatchet

Jul 2024

Report

20 pages

Live Streaming Trends Reports (Q2'24)

Live streaming viewership reached 8.5 billion hours in Q2 2024, representing a 10% year-over-year increase and the first significant growth surge since the post-pandemic decline.

Twitch’s market share of hours watched dropped from 70% in Q2 2023 to 60% in Q2 2024, while YouTube Gaming grew its share to 23.4%.

The streaming ecosystem is becoming less centralized, with the top 5% of streamers now holding 86% of the market share, down from 98% in 2019.

Streaming

Market Analysis

Global

Stream Hatchet

Jun 2024

Report

20 pages

Stream Hatchet Q2 2024 Report

Live streaming viewership reached 8.5 billion hours in Q2 2024, representing a 10% year-over-year increase.

Twitch's market share of hours watched declined from 70% in Q2 2023 to 60% in Q2 2024.

YouTube Gaming grew to a 23% market share, while the platform Kick captured 5.5% of the total viewership.

Streaming

Market Analysis

Player Behavior

+1

Stream Hatchet

Jun 2024

Report

6 pages

How to Master Europe’s Digital Infrastructure Needs?

Video Games Europe opposes new network fees or expanded regulation of cloud services, arguing these measures would threaten net neutrality, increase consumer costs, and damage European digital competitiveness.

The European video game industry generates €24.5 billion in annual revenue and employs approximately 110,000 people, with 53 percent of the European population participating in gaming.

Gaming traffic is significantly lower than video streaming, with typical online gameplay consuming 60–80 megabytes per hour and high-intensity titles rarely exceeding 300 megabytes per hour.

Europe

Cloud Gaming

Streaming

+3

Video Games Europe

Jun 2024

Report

292 pages

Reinvent India's Media & Entertainment Sector Is Innovating for the Future

The Indian media and entertainment sector reached a valuation of INR2.32 trillion in 2023 and is projected to exceed INR3 trillion by 2026, growing at a 10% CAGR.

Digital media is expected to overtake television as the dominant industry segment by 2024, supported by a projected expansion to nearly one billion active screens by 2030.

Online gaming has become the fourth-largest segment, surpassing filmed entertainment despite the implementation of a 28% GST mandate.

Market Analysis

Market Forecast

India

+1

Ernst & Young

Mar 2024

Report

28 pages

2023 Yearly Live Streaming Trends Report

The global live streaming market stabilized at 38.3 billion hours watched in 2023, characterized by Twitch's 4.9% decline and YouTube Gaming's 11% growth.

Kick emerged as the third-largest Western streaming platform within its first year, hosting nearly one million unique channels and displacing Facebook.

Esports viewership grew 9% year-over-year to 2.5 billion hours, with co-streaming now driving nearly 30% of total esports consumption.

Market Analysis

Streaming

Global

Stream Hatchet

Mar 2024

Report

24 pages

The Games We Watched: Lurkit’s Top 500 Streaming Report Q1 2024

The global game streaming market grew 10% year-over-year in Q1 2024, with the top 500 titles on Twitch generating 3.8 billion hours of watch time.

Market dominance by the top ten developers is softening, with their collective market share dropping from 63% to 59% compared to the previous year.

Grand Theft Auto V and League of Legends remain the market leaders, recording 479 million and 379 million hours watched respectively.

Streaming

Market Analysis

Lurkit

Mar 2024

Report

18 pages

Live-Streaming Trends Report: Q1 2024

Global live-streaming viewership reached 8.2 billion hours in Q1 2024, marking a 10% year-over-year increase and the first Q1 growth since 2021.

Twitch maintains a 69% market share, though its dominance is being challenged by YouTube Gaming, Kick, and Steam, the latter of which doubled its hours watched this quarter.

Twitch’s exit from South Korea triggered a successful migration of viewers to local platforms, specifically AfreecaTV and the rapidly growing Chzzk.

Streaming

Market Analysis

Global

Stream Hatchet

Mar 2024

Report

19 pages

Top 500 Titles on Twitch 2023

The top 500 Twitch titles generated nearly 15 billion hours of watch time in 2023, with 50% of that total concentrated in just 11 games.

Grand Theft Auto V was the most-watched title of 2023, accumulating 1.3 billion hours of viewership.

Fortnite led the industry in creator engagement with 2.8 million unique channels, more than double the count of its nearest competitor.

Streaming

Market Analysis

Global

Lurkit

Jan 2024

Report

4 pages

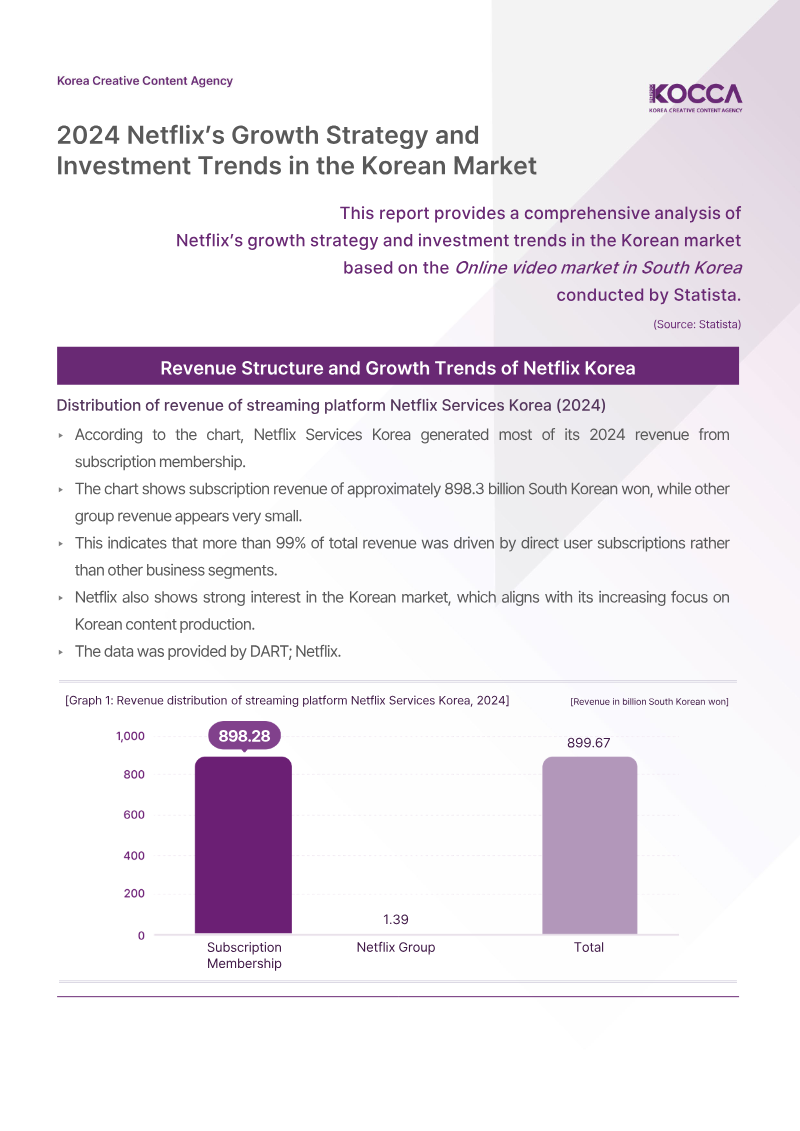

2024 Netflix’s Growth Strategy and Investment Trends in the Korean Market

Netflix’s streaming revenue in South Korea grew more than five-fold between 2019 and 2024, rising from approximately 175.6 billion won to 898.3 billion won.

The company’s revenue model in South Korea is highly concentrated, with over 99% of income generated directly from user subscriptions.

Annual investment in Korean content saw a massive escalation, climbing from 15 billion won in 2016 to a peak of 550 billion won in 2021.

Investment

Streaming

Market Analysis

+1

KOCCA – Korea Creative Content Agency

Jan 2024

Report

54 pages

Live Streaming Trends Annual Report 2024

Mobile streaming now accounts for nearly 50% of global viewership, driven by mobile-first infrastructure in Southeast Asia and Latin America.

Creators using cross-platform promotional strategies that integrate short-form video content achieve a 20% higher audience retention rate than those relying exclusively on live broadcasts.

Twitch remains the leader in community-driven content, while YouTube Gaming is capturing significant market share in competitive esports through its integrated VOD ecosystem.

Streaming

Market Analysis

Global

Stream Hatchet

Jan 2024

Report

54 pages

Save Point 2024: Recapping the Year’s Biggest Trends on Live Streaming

Simulcasting has become the industry-standard distribution model, with top creators achieving concurrent-viewer gains between 148% and 491% by broadcasting across multiple platforms simultaneously.

Co-streaming is now the primary driver of esports engagement, accounting for 44.4% of total viewership and 1.2 billion hours watched.

Kick experienced significant growth in 2024, surging 176% to reach 1.7 billion hours of viewership, bolstered by major events like the 1.4 million-viewer 'Stream Fighters 3'.

Streaming

Market Analysis

Global

+1

Stream Hatchet

Jan 2024

Report

276 pages

India's Media & Entertainment Sector: March 2024

India's media and entertainment sector is projected to reach INR 3.1 trillion ($37 billion) by 2026, growing at a 10% CAGR as online platforms overtake traditional television as the primary revenue driver.

Mobile-first consumption is the primary growth engine, supported by 904 million broadband subscriptions and 574 million smartphone users who spend over four hours daily on mobile media.

Gaming is a dominant market force, with Free Fire and BGMI accounting for 25% of in-app purchase revenue and esports viewership reaching 78% of the gaming population.

Market Analysis

India

Streaming

EY

Jan 2024

Report

54 pages

Save Point 2024: Recapping the Year's Biggest Trends in Live Streaming

The live streaming industry shifted toward a creator-led, multi-platform model in 2024, characterized by widespread simulcasting and the rise of alternative platforms like Kick following Twitch’s withdrawal from the Korean market.

Co-streaming has become a dominant force in competitive gaming, now accounting for nearly 45 percent of total esports viewership.

Large-scale, non-gaming spectacles like La Velada del Año 4 demonstrated that independent creators can now command millions of concurrent viewers, rivaling traditional broadcast media.

Market Analysis

Streaming

Esports

+1

Stream Hatchet

Jan 2024

Report

5 pages

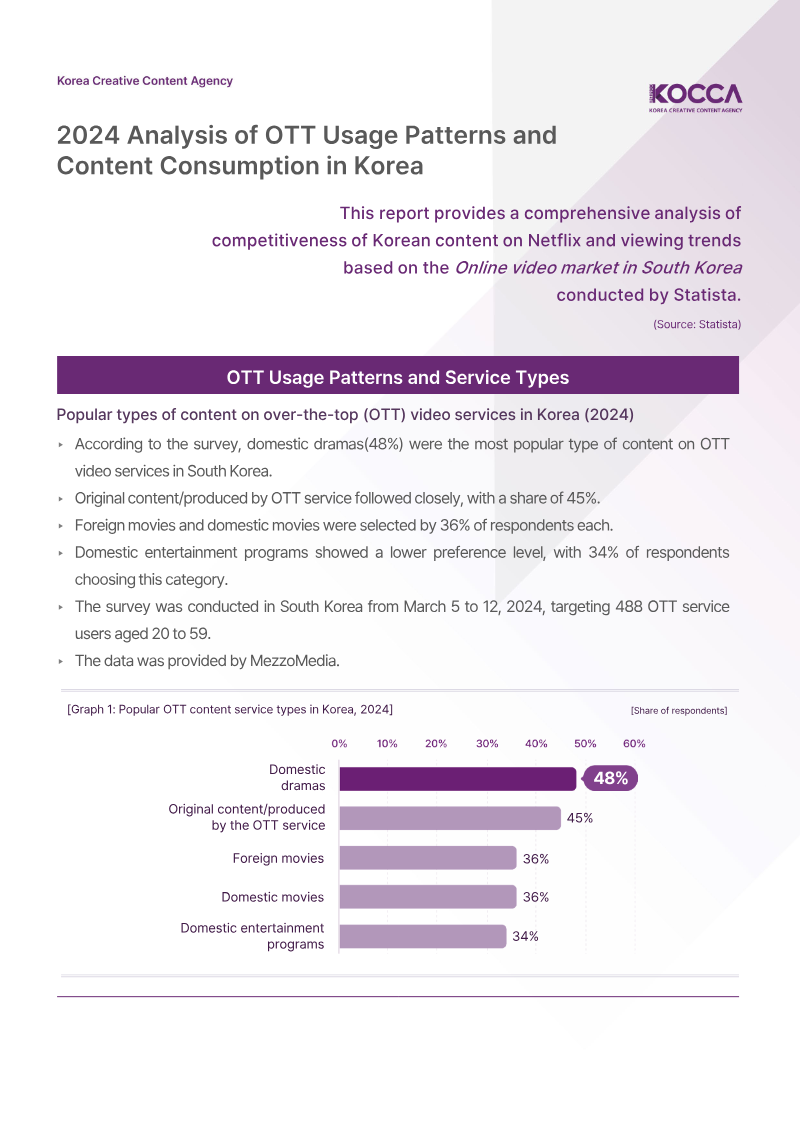

2024 Analysis of OTT Usage Patterns and Content Consumption in Korea

Cost is the primary driver for subscription churn, with 61% of users citing usage fees as the main reason for cancellation and 31% specifically noting fee increases.

Content scarcity is a major retention risk, as 51% of respondents cancel subscriptions due to a perceived lack of worthwhile content.

Domestic dramas (48%) and OTT-produced originals (45%) dominate the South Korean market, accounting for the vast majority of viewing share.

Market Analysis

South Korea

Streaming

+1

KOCCA – Korea Creative Content Agency

Jan 2024

Report

21 pages

Video Game Streaming Trends Report: Q1 2023

Total live-streaming viewership declined 16% year-over-year in Q1 2023, though total hours watched remain 46% higher than Q1 2020 levels.

Twitch and YouTube Live Gaming consolidated their market dominance to a combined 89% share, while Facebook Live viewership plummeted by 69%.

Cross-media synergy is a primary growth driver, evidenced by the HBO 'The Last of Us' series triggering a 107% increase in viewership for the franchise's games.

Streaming

Market Analysis

Global

+1

Stream Hatchet

Mar 2023

Report

18 pages

Esports Live-Streaming Trends Report: Q1 2023

Esports live-streaming viewership grew 15% year-over-year in Q1 2023 to 651 million hours, bucking the broader industry trend of declining live-streaming viewership.

Audience interest is highly concentrated, with the top 30 tournaments accounting for 68% of total esports hours watched.

Twitch holds 62% of the total esports market share, while YouTube maintains 30% and has successfully captured 34% of viewership for large-scale events with an average minute audience over 80,000.

Market Analysis

Esports

Streaming

+1

Stream Hatchet

Mar 2023

Previous

1

2

3

4

Next