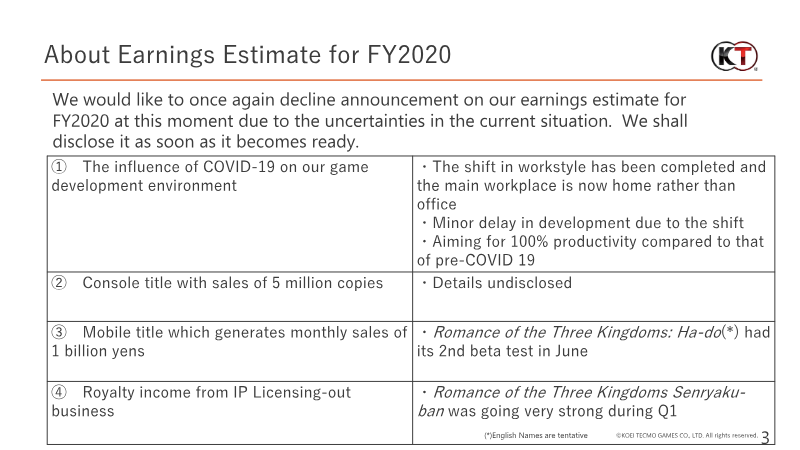

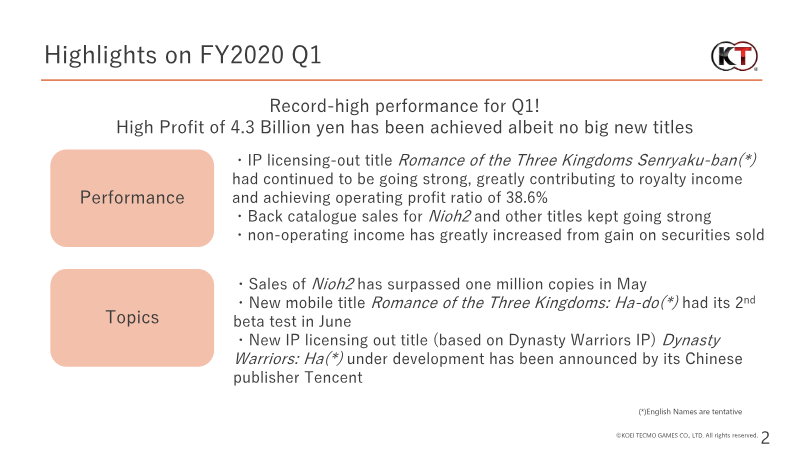

Market Analysis

Report

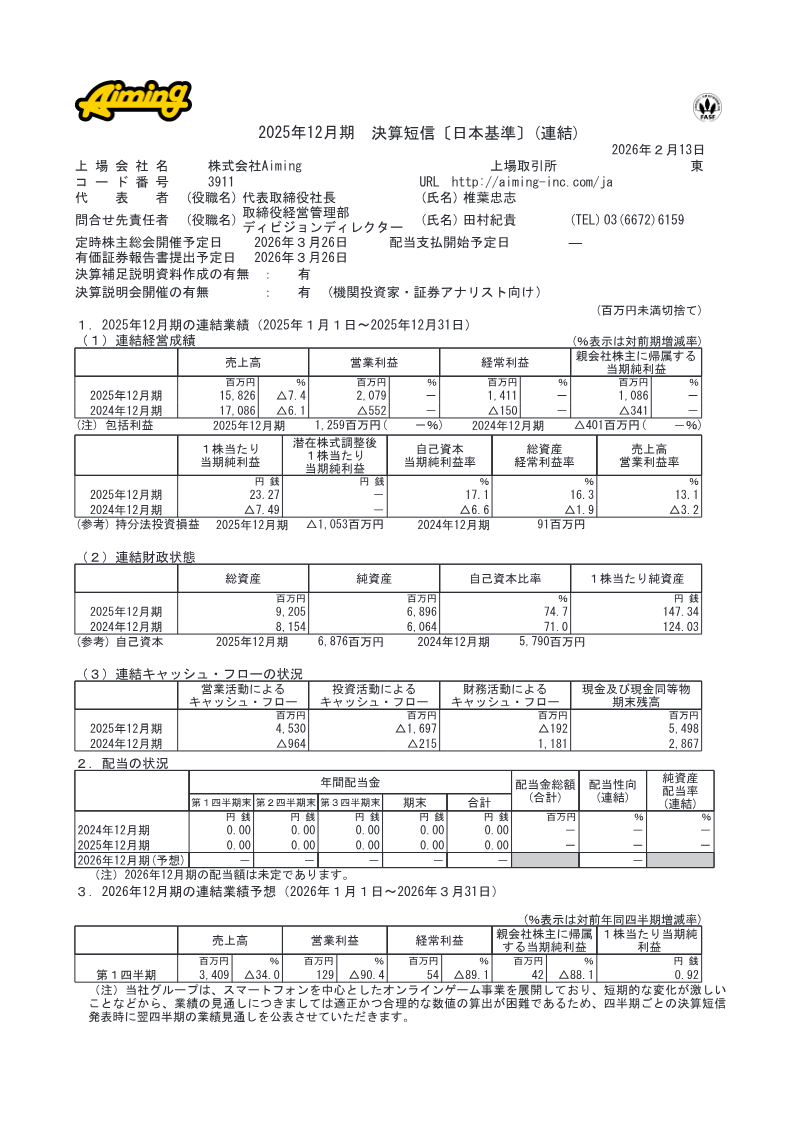

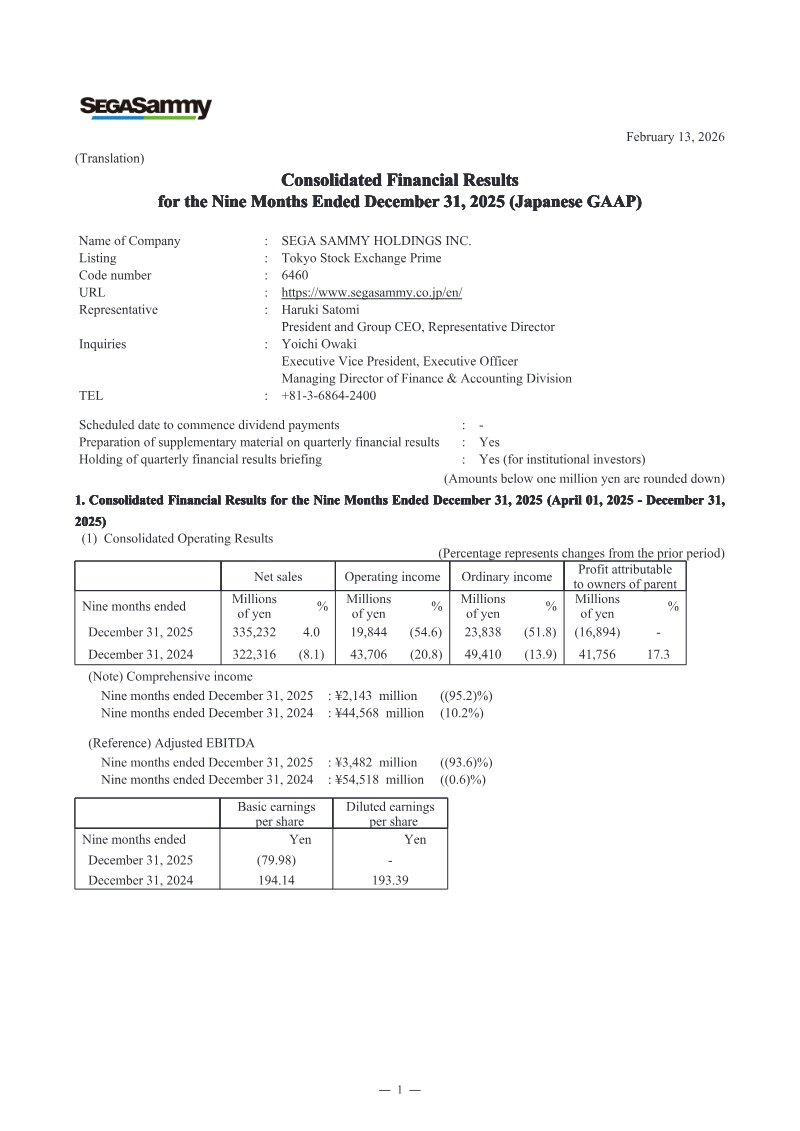

Consolidated Financial Results: FY2026/3 Q3

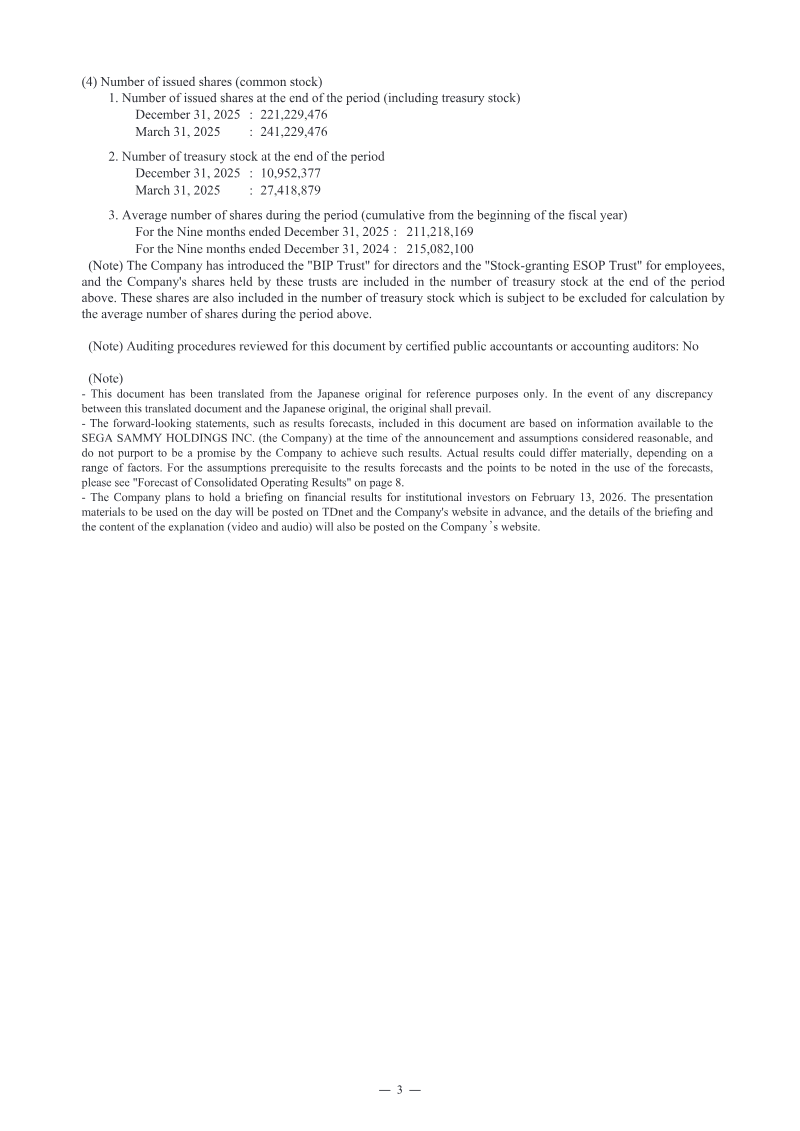

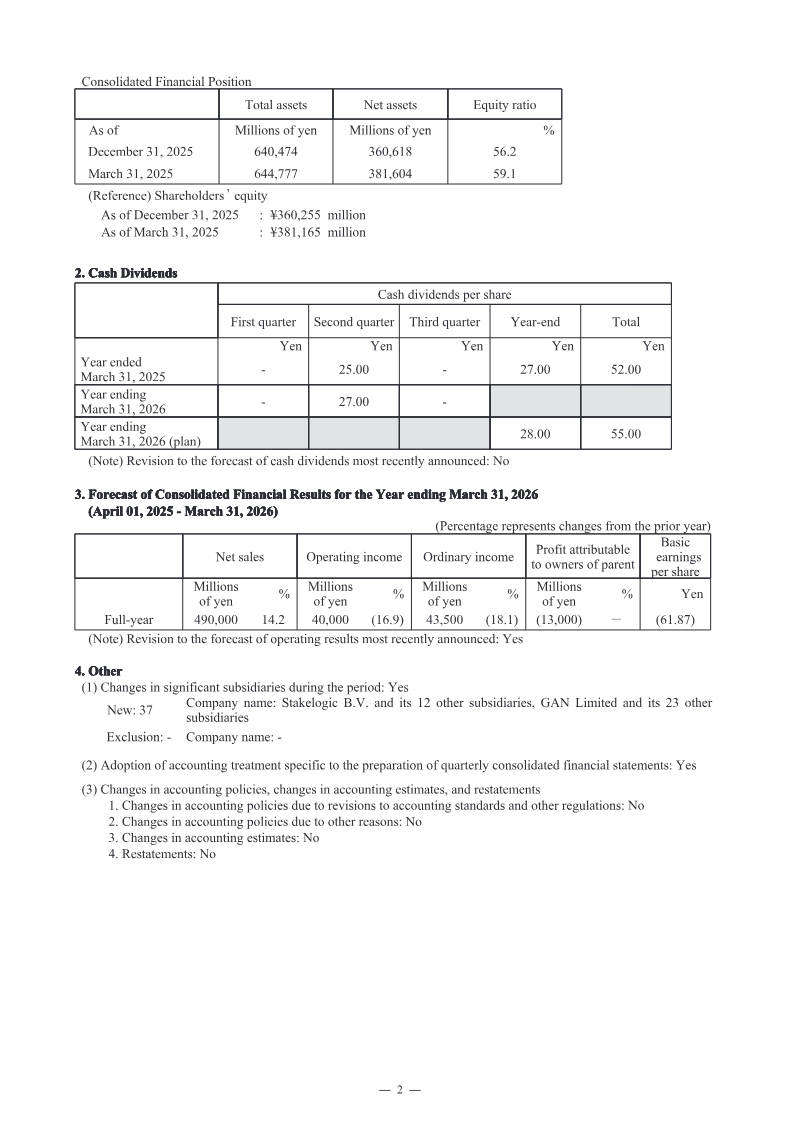

The quarterly consolidated financial results for SEGA SAMMY HOLDINGS INC. cover the nine‑month period ending December 31, 2025, within a fiscal year that ends March 31, 2026. Net sales rose 4 % to ¥335,232 million from ¥322,316 million in the prior year. Operating income fell sharply by 54.6 % to ¥19,844 million, driven largely by a ¥31,380 million impairment loss on goodwill and other intangible assets related to the Rovio subsidiary. Ordinary income declined 51.8 % to ¥23,838 million, and profit attributable to owners of parent turned a loss of ¥16,894 million. Adjusted EBITDA contracted 93.6 % to ¥3,482 million from ¥54,518 million, reflecting the extraordinary impairment and restructuring costs. Basic earnings per share shifted from a profit of ¥194.14 to a loss of ¥79.98. Segment performance varied: Entertainment Contents sales increased modestly (1.5 %) but ordinary income fell 34.3 % to ¥24,676 million; Pachislot & Pachinko sales declined 4.0 % with ordinary income dropping 46.0 %; Gaming revenue surged 438.5 % to ¥16,795 million but incurred a loss of ¥247 million due to consolidation of newly acquired GAN and Stakelogic. The Group’s balance sheet shows total assets at ¥640,474 million and net equity of ¥360,618 million, with the equity ratio at 56.2 %. Current liabilities rose to ¥109,254 million, lowering the current ratio to 35.1 %. Treasury stock increased from ¥54,866 million to ¥26,459 million as the company retired 20 million shares and subsequently acquired up to 12 million shares at a maximum cost of ¥20 billion. The results reflect significant impairment impacts, a shift in capital allocation policy toward shareholder returns, and ongoing adjustments to the Gaming and Entertainment segments amid new acquisitions.

Sega Sammy Holdings

Report

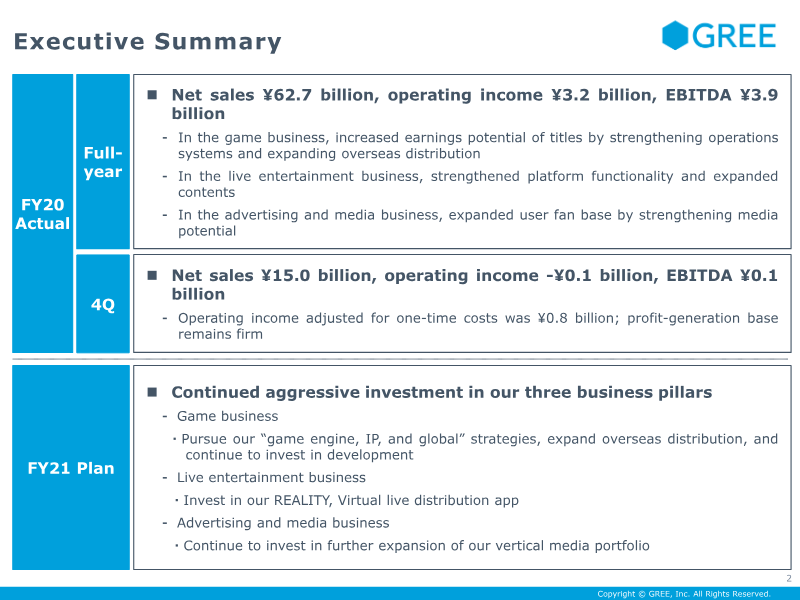

Summary of main questions and answers at the FY2019 Second Quarter GREE results briefing held on February 4, 2019 PDF

The briefing focused on the performance and strategic outlook of GREE’s flagship title “Another Eden” following its overseas launch on January 29, 2019. Early sales data indicate a strong start abroad, with overseas user numbers already surpassing domestic figures. The company attributes this success to effective advance marketing and anticipates that limited overseas development costs—primarily translation—will translate into significant profit contributions. Marketing hypotheses for each target region were validated by current sales trends, confirming that the user profiles initially targeted align with actual players. In addressing future profitability, GREE disclosed a planned divestiture of unprofitable titles. The company estimates that this will reduce third‑quarter sales by several hundred million yen but will have a negligible impact on operating income, as overseas gains from “Another Eden” are expected to offset declines in existing titles. Concurrently, investment in new game development will increase, particularly during later production phases when outsourced labor and content creation intensify. Advertising spend is projected to remain flat domestically while allocating several hundred million yen for overseas promotion of “Another Eden.” A one‑time accounting adjustment in the first quarter, where variable costs were misclassified as overseas rather than domestic, was corrected in the second quarter. GREE clarified that this revision is isolated and will not recur. Overall, the briefing outlined a strategy of leveraging overseas market penetration to drive profitability while managing development and marketing expenditures in alignment with projected sales trajectories.

GREE