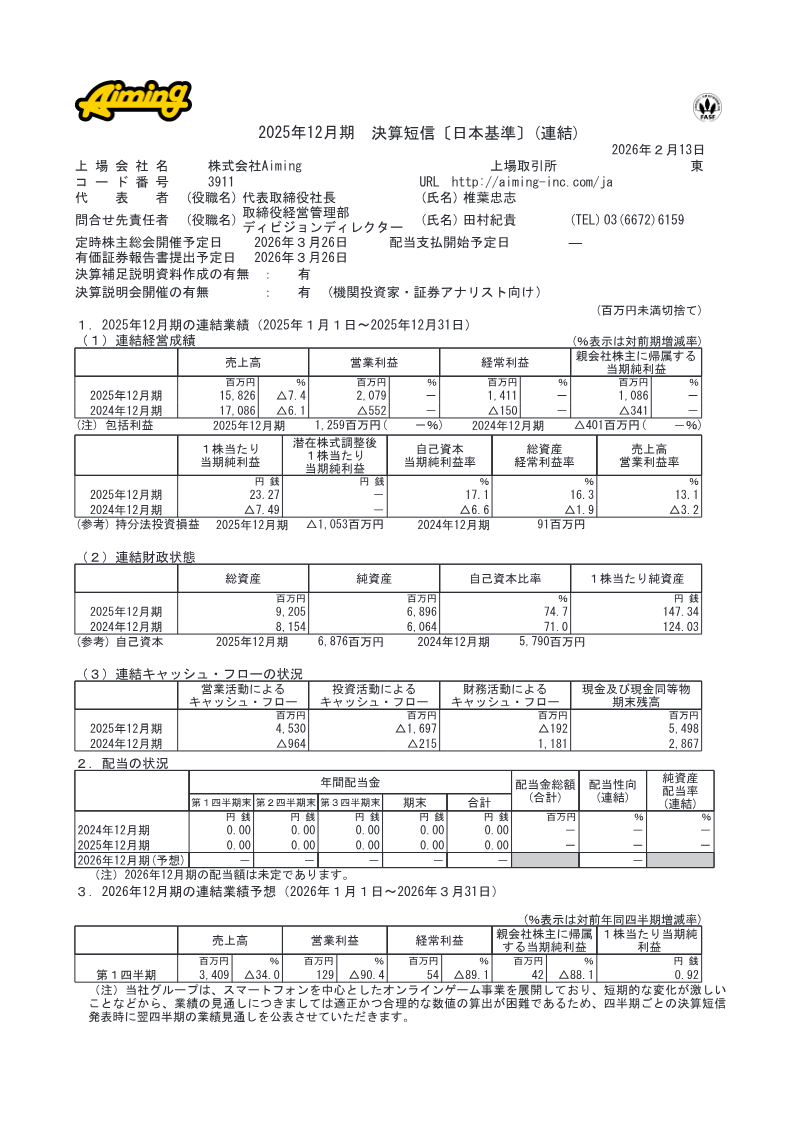

FinancialAiming

Consolidated Financial Results: Fiscal Year Ending December 2025

13 pages~6 min full read

Key insights

7 takeaways · ~3 min read- 01

The company returned to profitability in fiscal year 2025, reporting a net income of ¥1,086 million compared to a ¥341 million loss in 2024.

See it on page 4 - 02

Operating profit reached ¥2,079 million, a significant turnaround from the ¥552 million loss recorded in the previous fiscal year.

See it on page 4 - 03

Total revenue declined by 7% year-over-year, falling from ¥17,086 million in 2024 to ¥15,826 million in 2025.

See it on page 8 - 04

The company maintains a strong balance sheet with an equity ratio of 74.7% and cash and equivalents totaling ¥5,498 million.

See it on page 6 - 05

Mobile online gaming remains the sole operating segment, with performance bolstered by strategic collaborations such as those with Square Enix.

See it on page 4 - 06

Management forecasts a 34% decline in sales and operating profit for the first quarter of fiscal year 2026 due to anticipated market volatility.

See it on page 1 - 07

No dividends were declared for fiscal years 2024 or 2025, and the dividend policy for 2026 remains undetermined.

See it on page 1