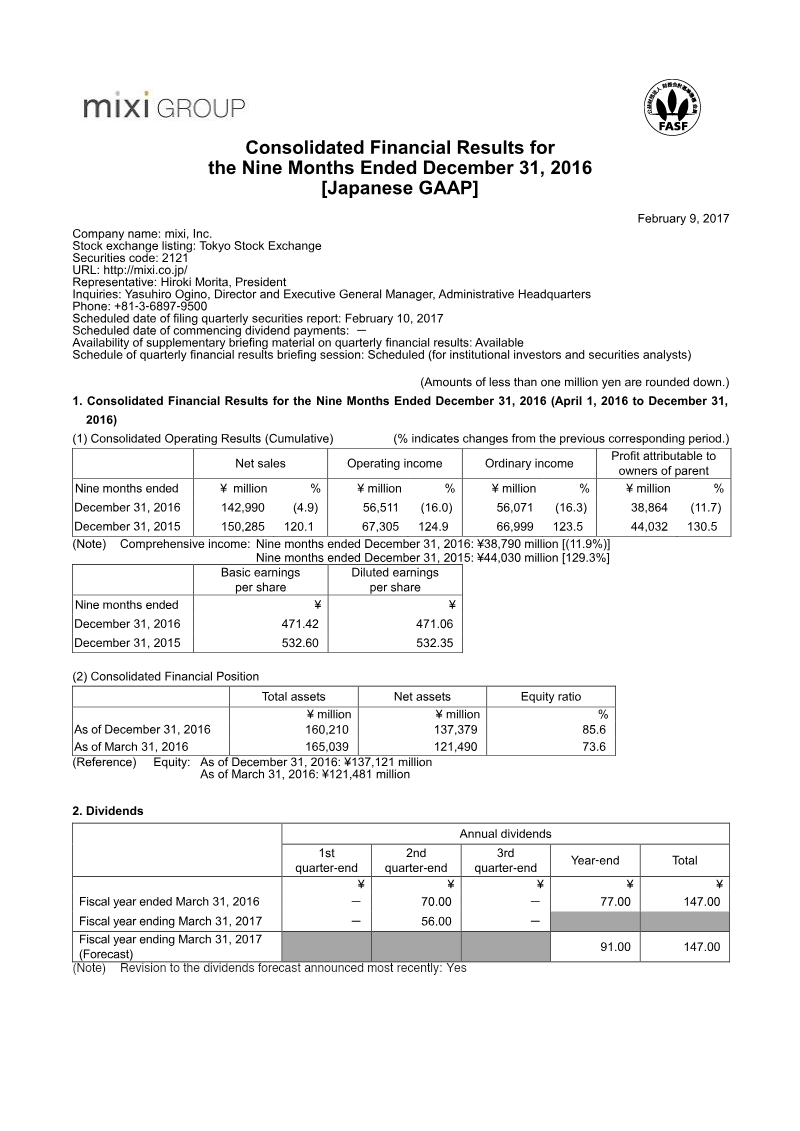

Investment

Report

1Q FY2023 Presentation Material

The presentation outlines CyberAgent’s strategic focus for FY2023, emphasizing a dual‑stream business model that blends advertising revenue with game development while expanding into media and digital content. Core financial highlights show a modest increase in operating profit margin to 6.7 % from 5.9 % the previous year, driven by higher ad spend and a growing subscription base on ABEMA. Operating profit rose to ¥6.4 billion, with revenue growth of 8.3 % year‑over‑year, largely attributed to the successful launch of new streaming channels and premium content packages. Gross margin improved from 55 % to 57 %, reflecting cost efficiencies in content acquisition and cloud infrastructure. Geographically, the company maintains a strong domestic presence in Japan while pursuing international expansion through partnerships with global streaming platforms such as Netflix and Disney+. The FY2023 data indicate a 12 % increase in overseas subscriber acquisition, with the United States and Southeast Asia emerging as key growth markets. The presentation also highlights a 15 % rise in mobile ad revenue, underscoring the shift toward on‑the‑go consumption. Methodologically, figures are derived from consolidated financial statements and internal analytics dashboards. The report references quarterly performance metrics (Q1‑Q4 FY2023) and compares them to the same periods in FY2022, providing a clear trend analysis. Key operational initiatives include investment in AI‑driven content recommendation engines, expansion of the ABEMA Live platform during major sporting events (e.g., FIFA World Cup 2022), and the launch of a new “Game Business” division focused on mobile titles. Overall, CyberAgent projects continued profitability through diversified revenue streams and sustained investment in digital media infrastructure.

CyberAgent

Report

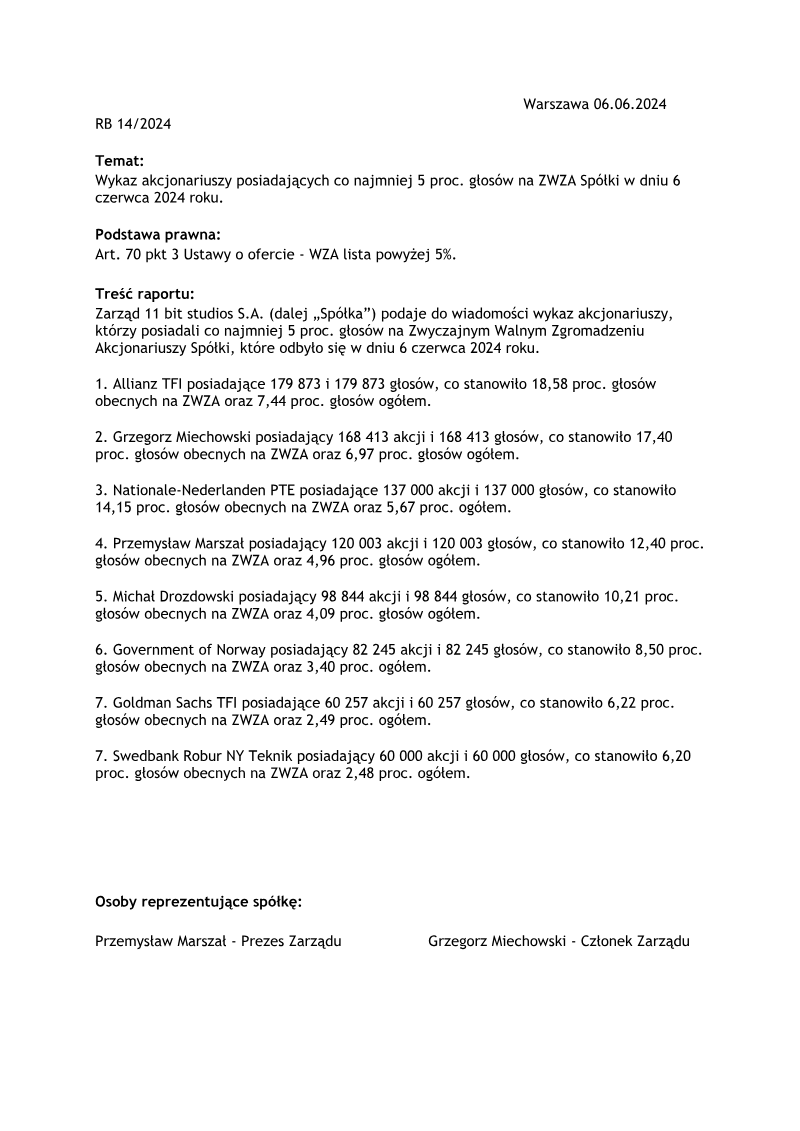

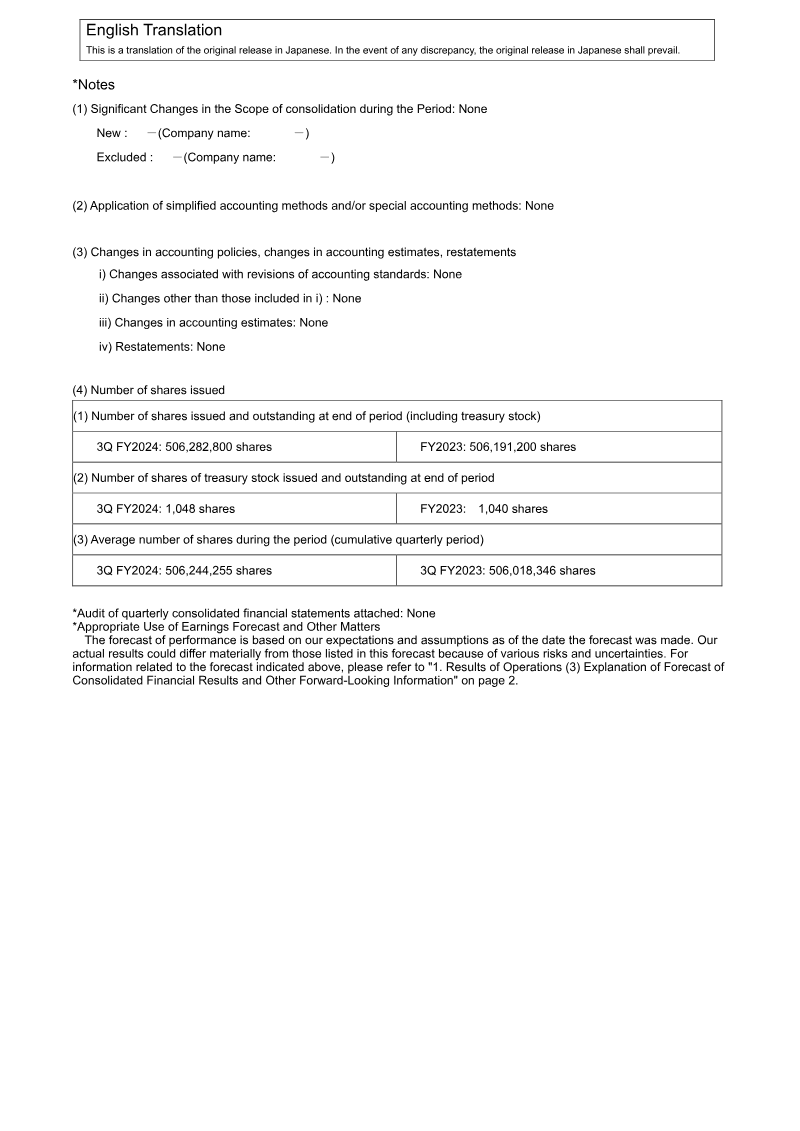

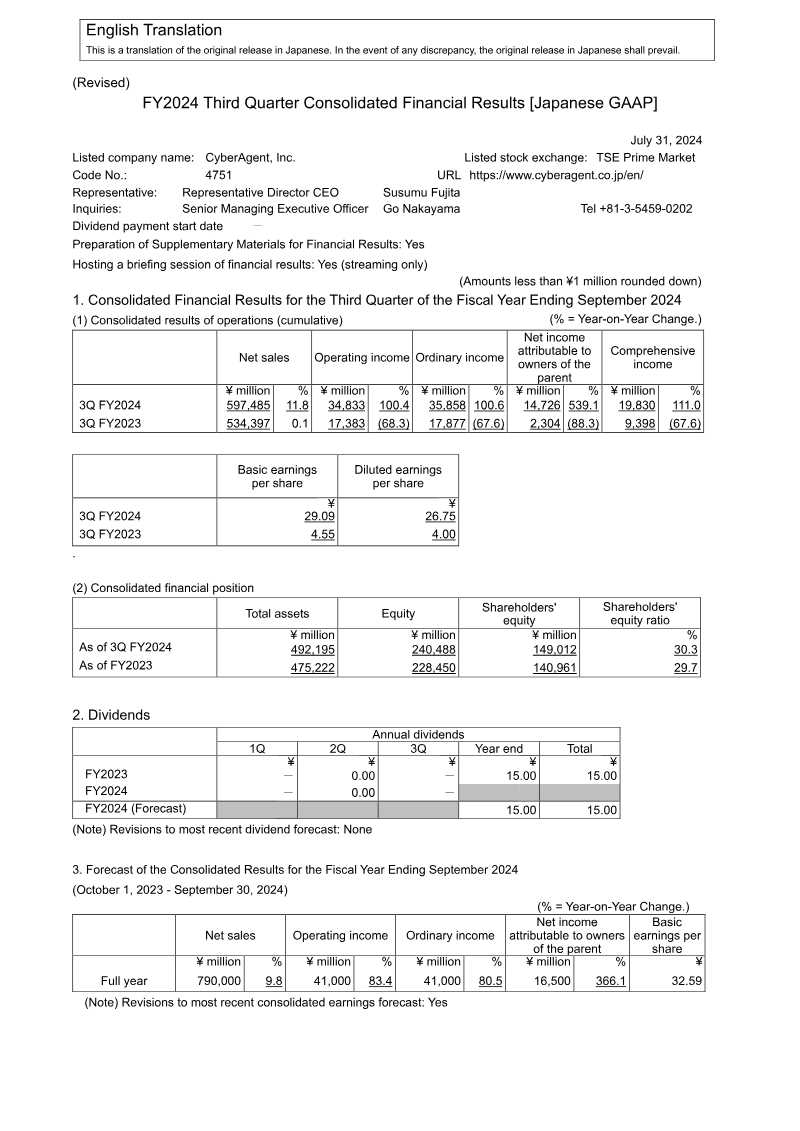

Partial Correction to FY2024 Third Quarter Consolidated Financial Results [Japanese GAAP]

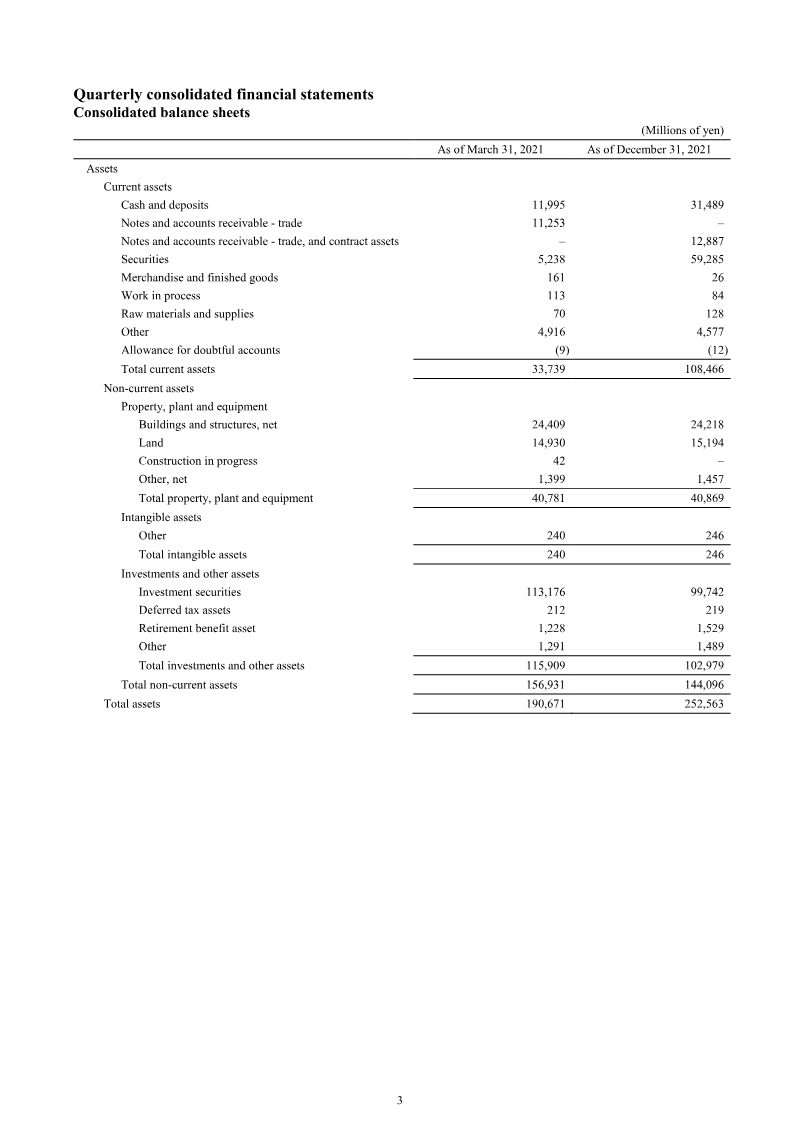

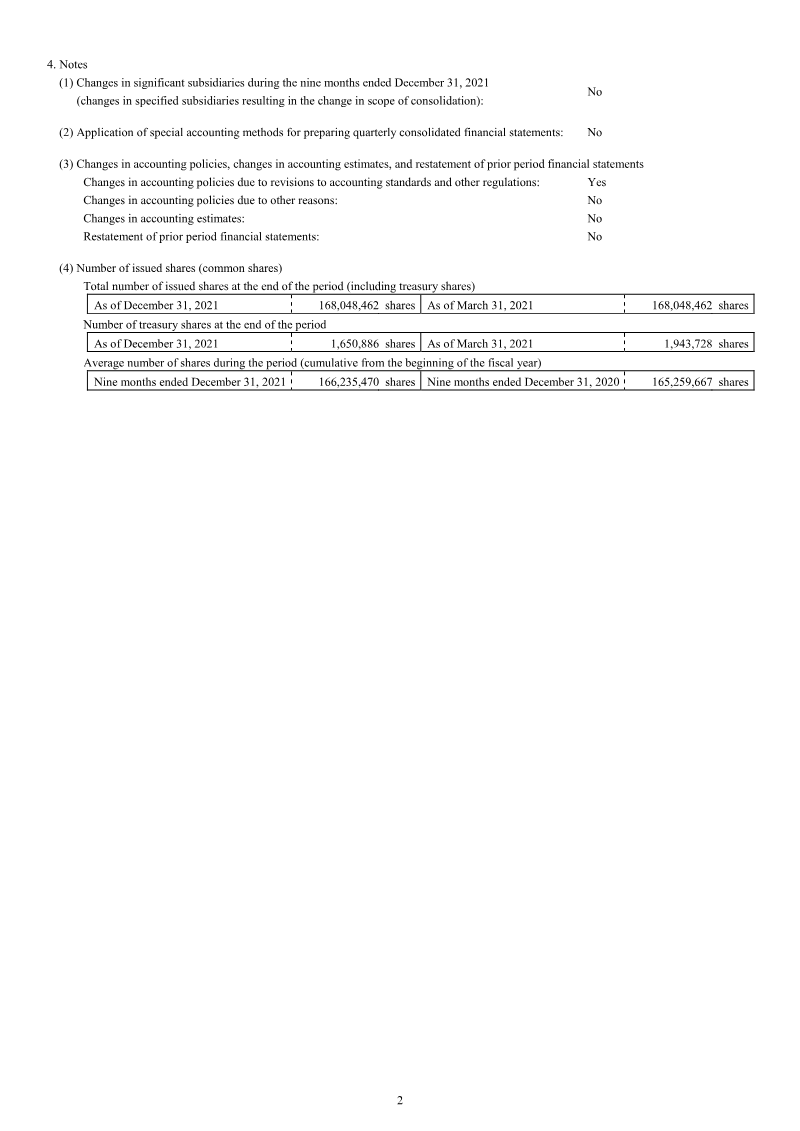

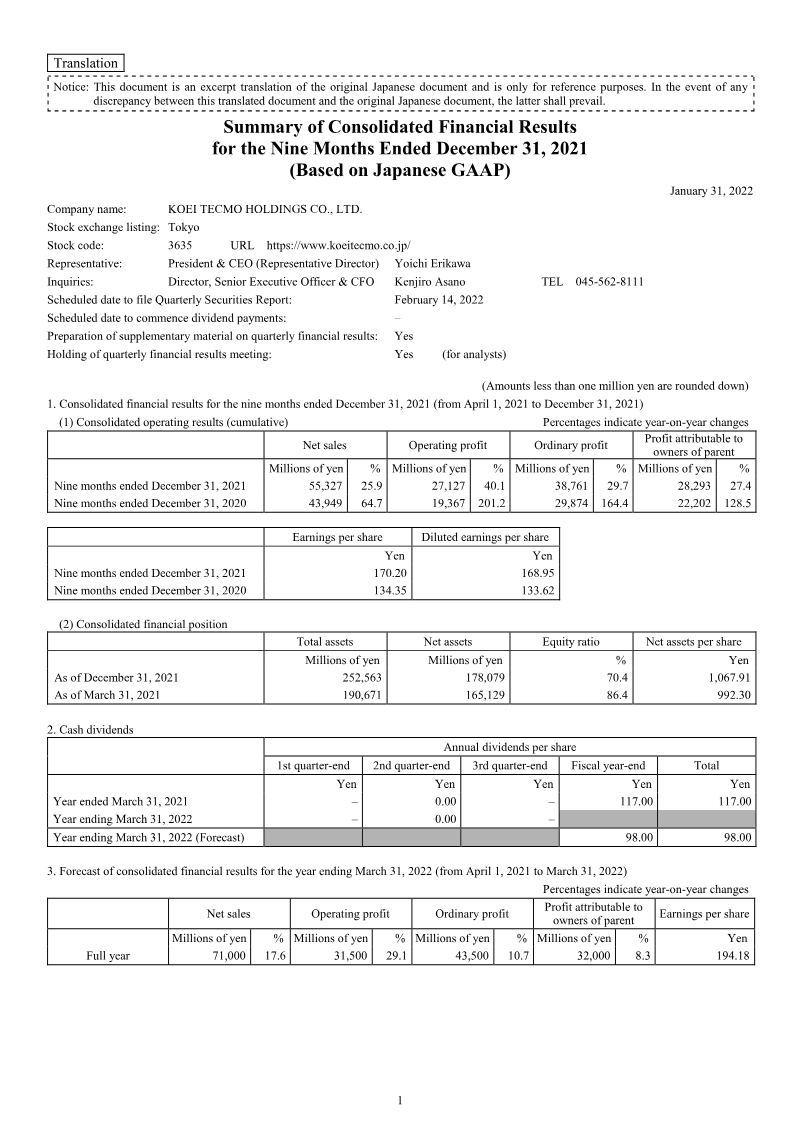

CyberAgent, Inc. issued a partial correction to its FY2024 third‑quarter consolidated financial results under Japanese GAAP, released on May 15 2025. The correction addresses numerical inaccuracies in the previously disclosed July 31 2024 results, with revised figures presented in full. Net sales for the cumulative third quarter rose 11.8 % year‑on‑year to ¥597,485 million, while operating income doubled to ¥34,833 million (100.4 % increase). Ordinary income and net income attributable to owners of the parent surged 100.6 % and 539.1 %, respectively, reaching ¥35,858 million and ¥14,726 million. Basic earnings per share climbed from ¥4.55 to ¥29.09, and diluted EPS rose from ¥4.00 to ¥26.75. Total assets increased by ¥16,972 million to ¥492,195 million, with equity rising 30.3 % to ¥240,488 million; liabilities grew by ¥4,934 million. Cash and deposits expanded to ¥206,055 million, reflecting sales growth. The company maintained a dividend forecast of ¥15.00 million per quarter for FY2024, unchanged from prior guidance. Segment analysis shows the Media Business (ABEMA) generated ¥125,885 million in sales with an operating loss of ¥489 million; Internet Advertisement achieved a record ¥323,740 million in sales and ¥16,454 million operating income; Game Business contributed ¥151,070 million in sales and ¥26,844 million operating income. Investment Development and Other Businesses recorded modest sales with mixed profitability. The correction also notes a business combination: CyberAgent acquired 72.5 % of Nitroplus Co., Ltd. on July 1 2024, a content‑creation firm known for IP such as Touken Ranbu. The acquisition, valued at ¥16,683 million in cash, aims to strengthen CyberAgent’s media‑mix strategy and global IP expansion. No significant changes in accounting policies or consolidation scope were reported, and the company reaffirmed its forward‑looking forecasts for FY2024.

CyberAgent