Back to Writers

Koei Tecmo

Game Co.

212 documents

Japanese developer/publisher. Dynasty Warriors, Nioh, Dead or Alive, Atelier, Romance of the Three Kingdoms.

Documents

Report

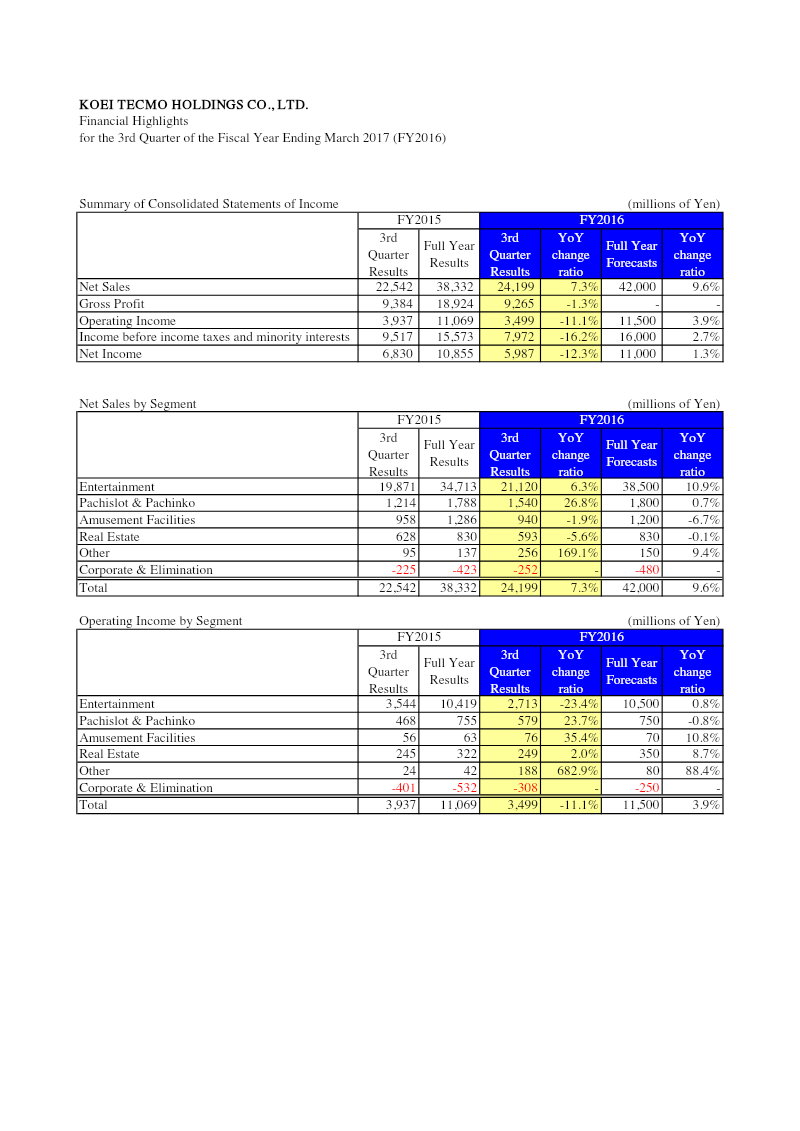

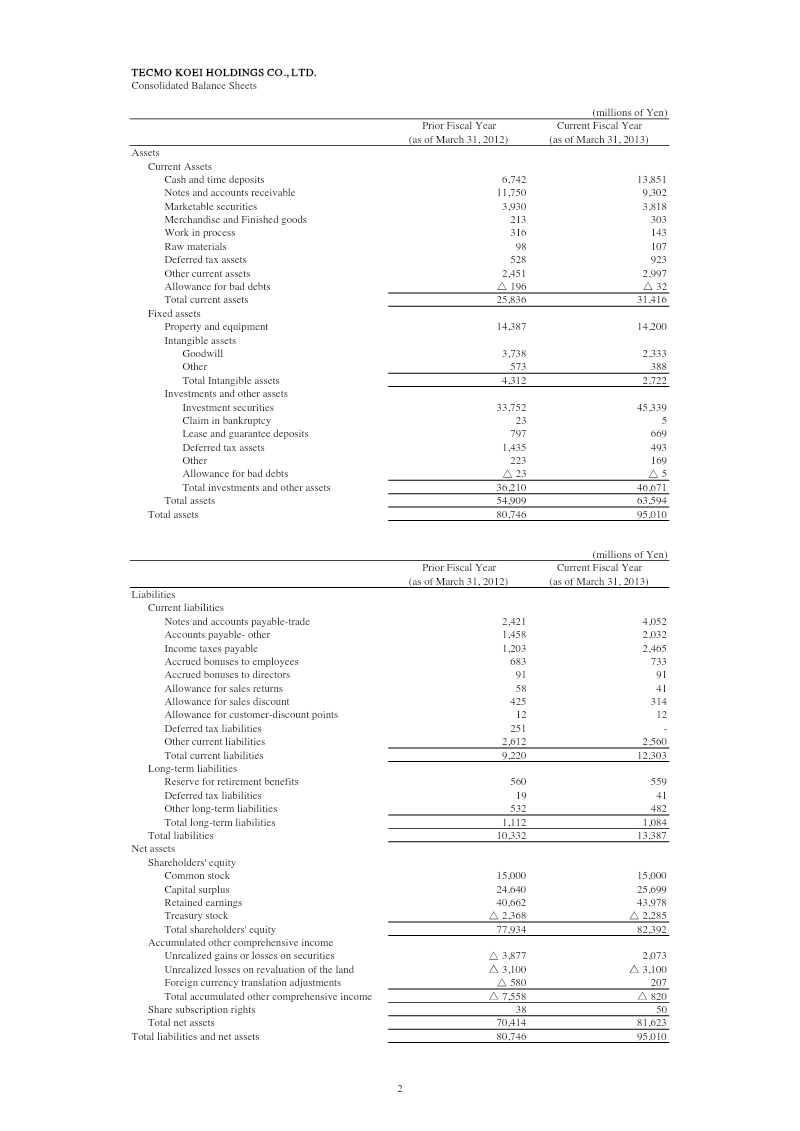

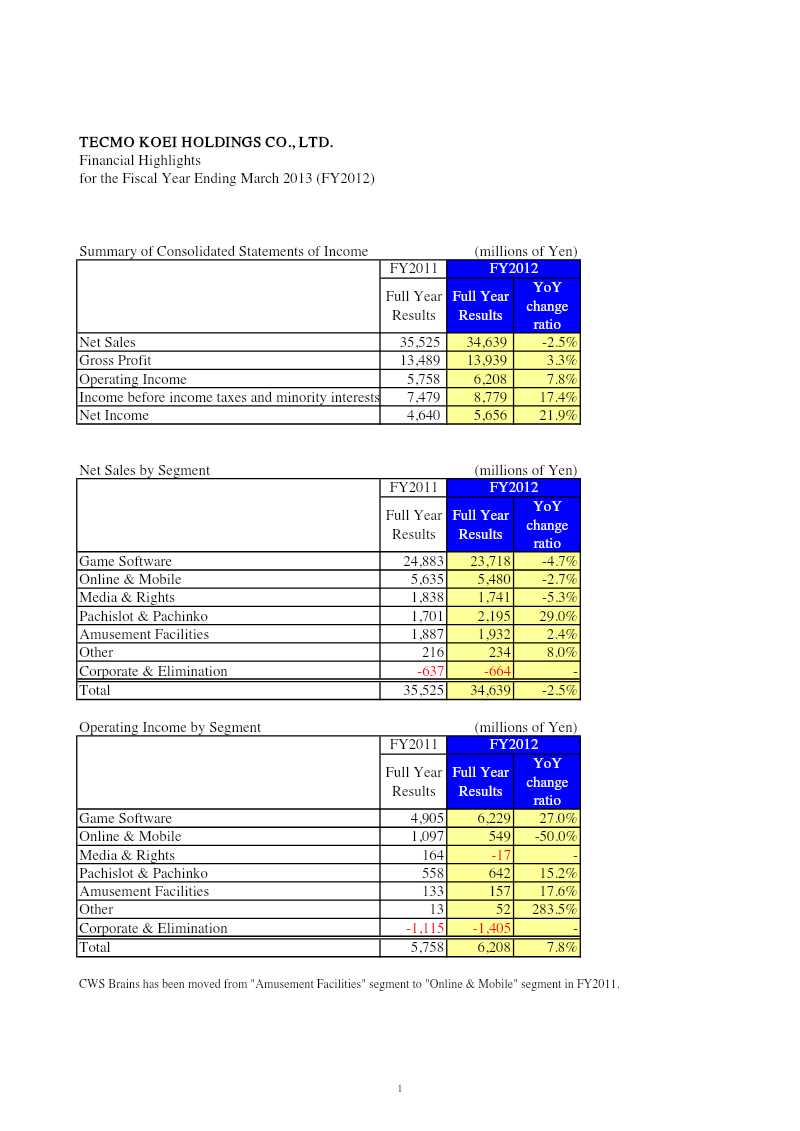

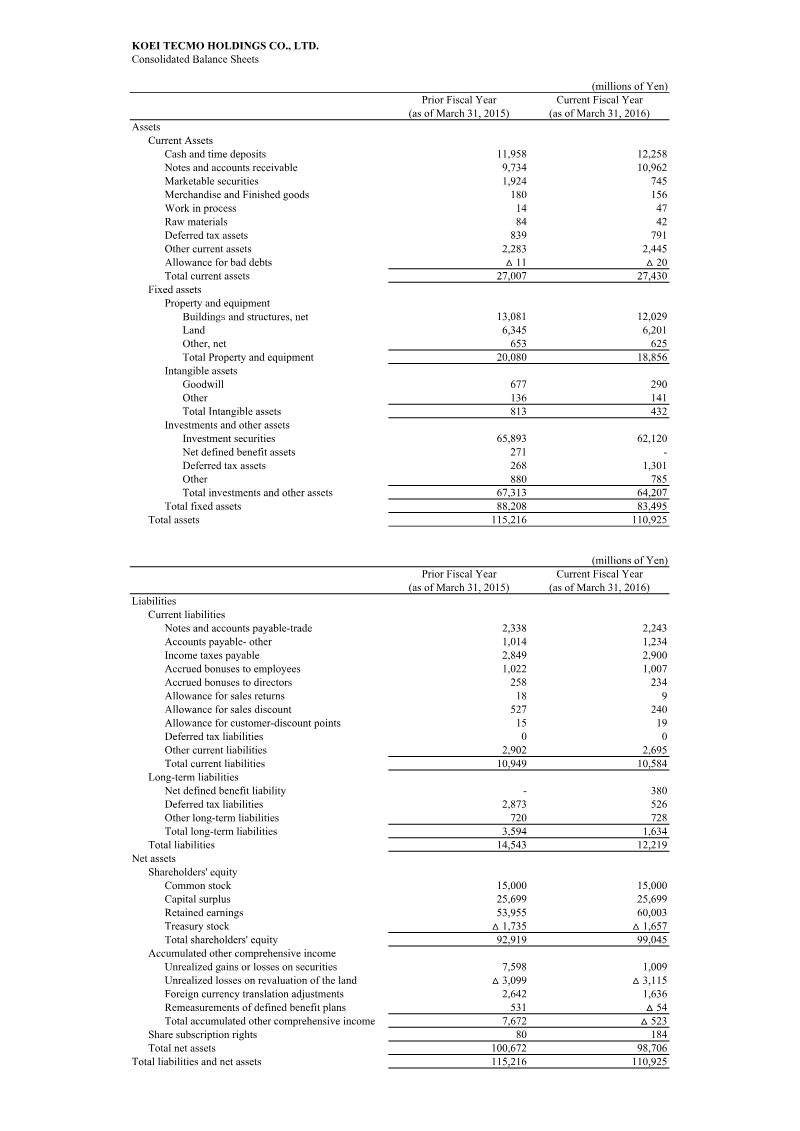

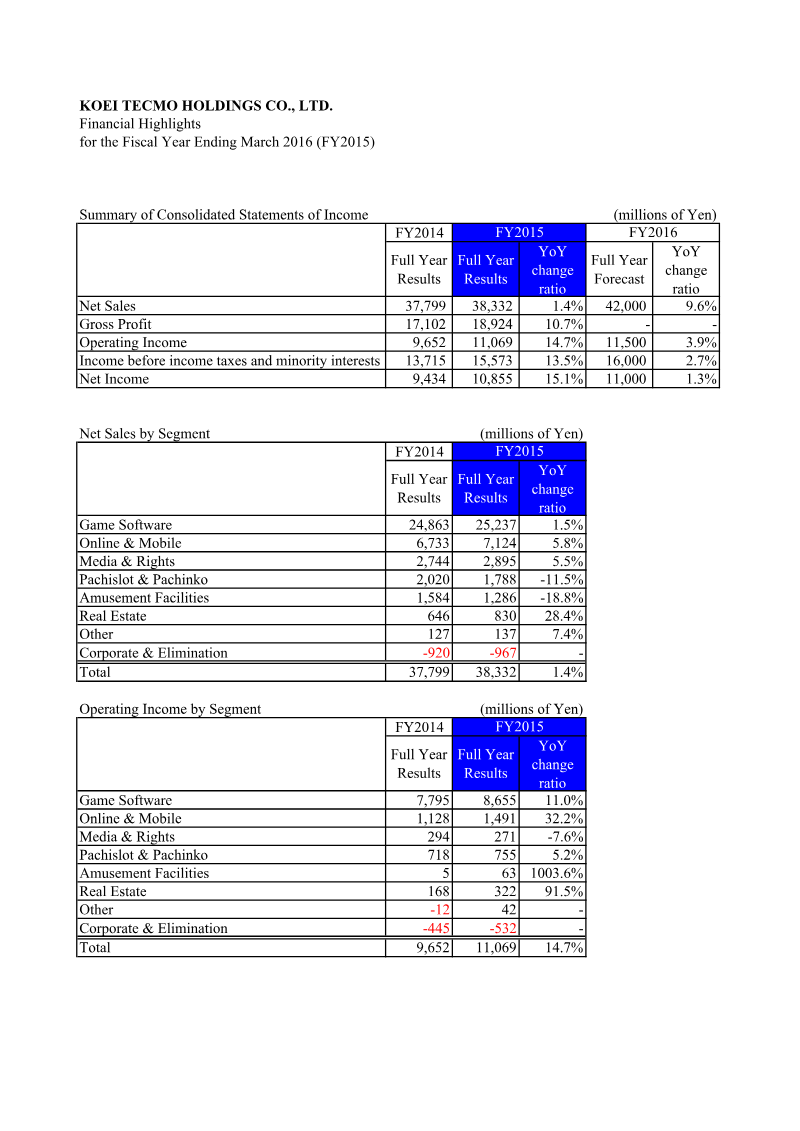

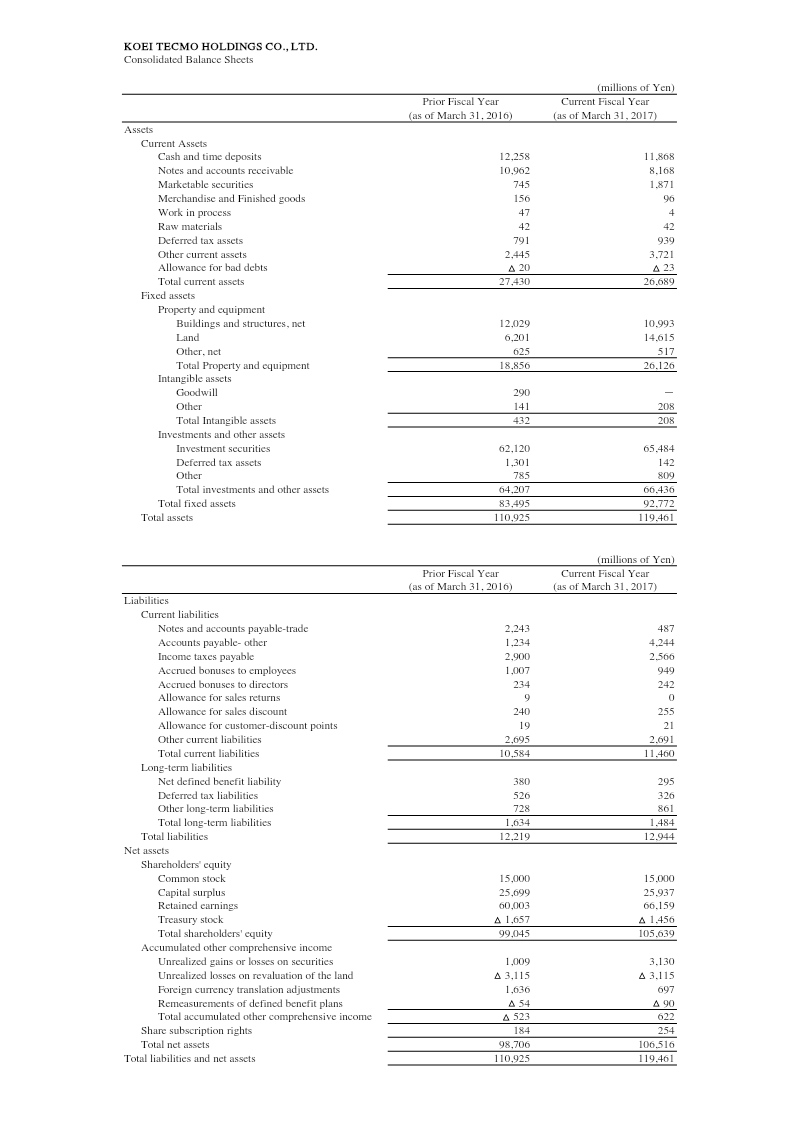

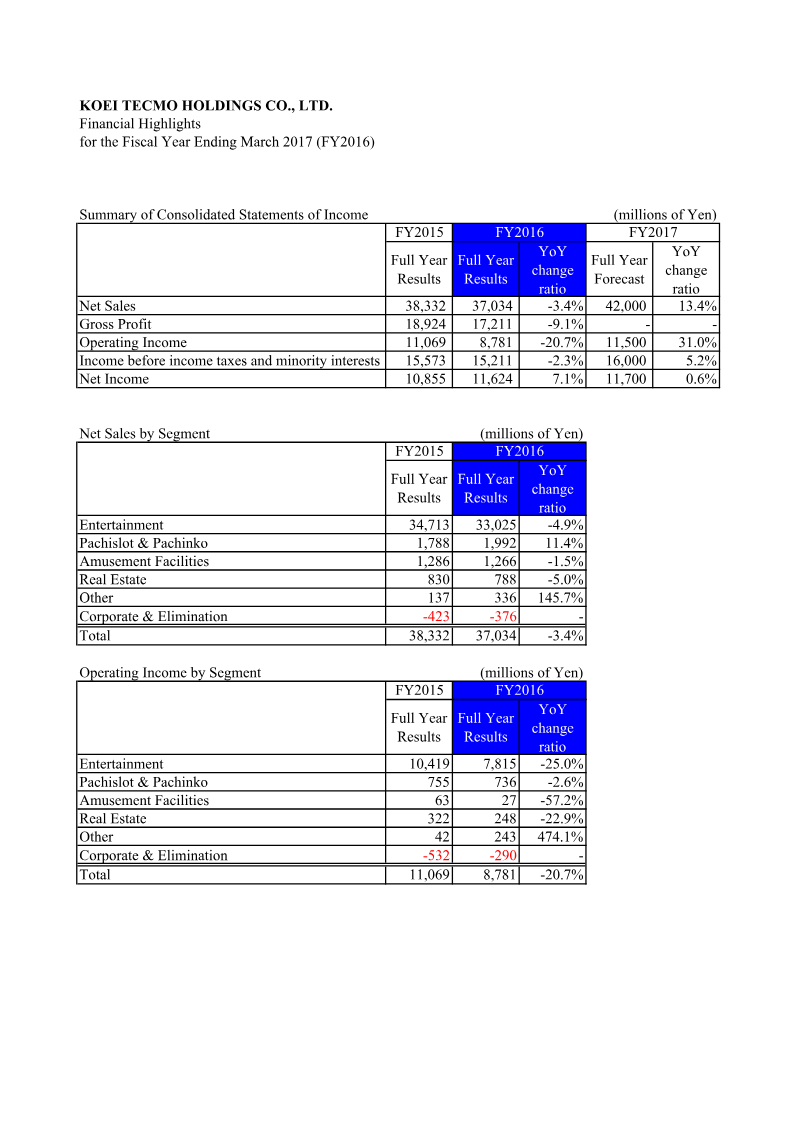

Financial Highlights: Fiscal Year Ending March 2017

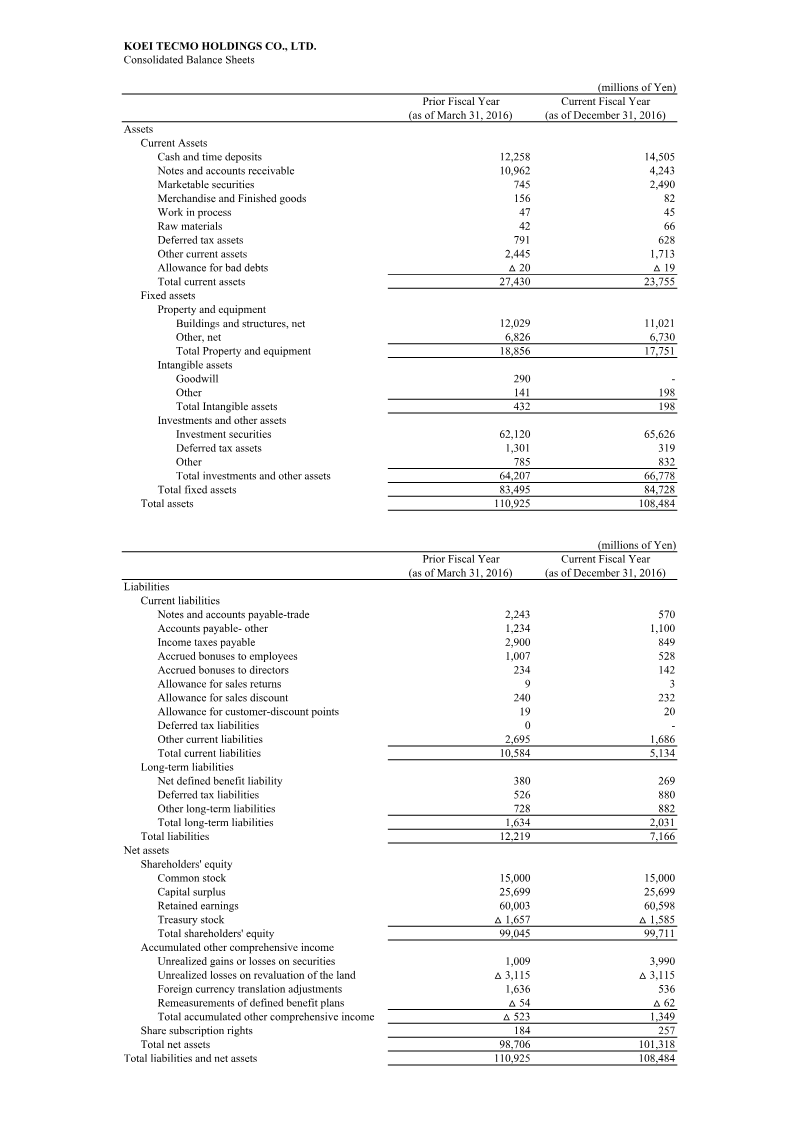

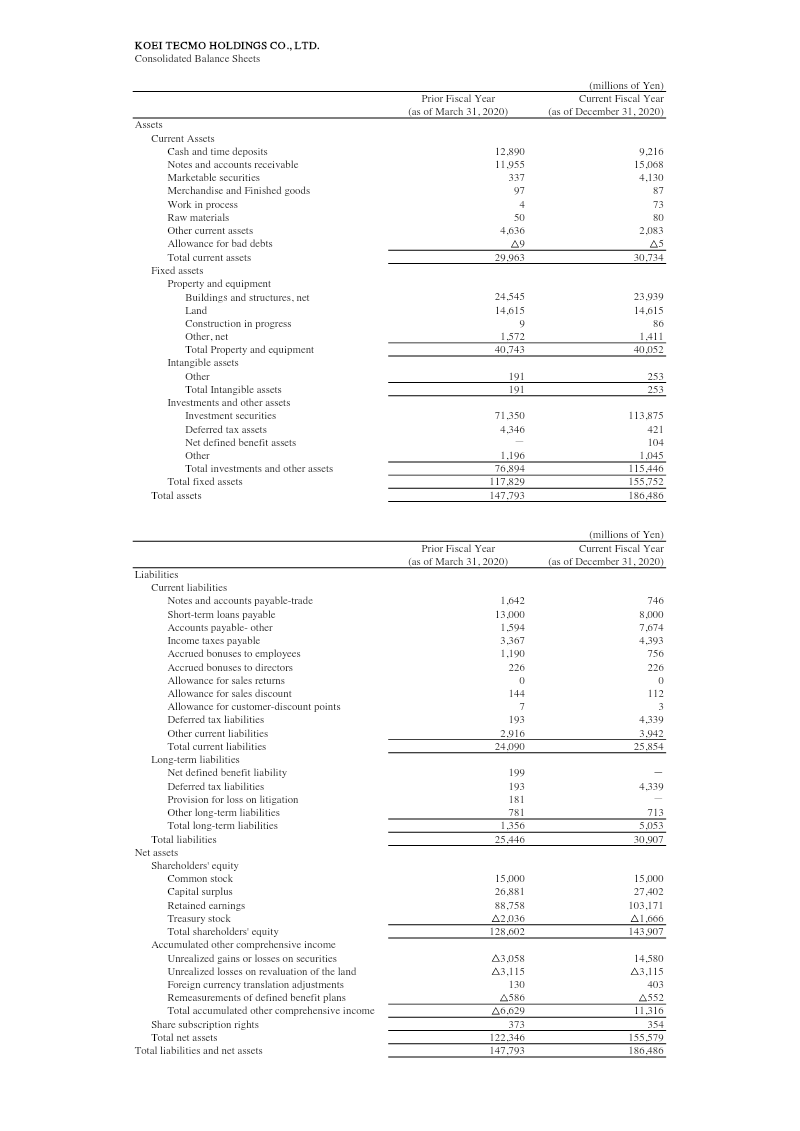

Koei Tecmo Holdings reported a modest improvement in fiscal performance for the year ending March 2017 compared with the prior year. Net sales fell 3.4 % to ¥37,034 million, largely due to a 4.9 % decline in the entertainment segment and a 1.5 % drop in amusement facilities, while pachislot & pachinko sales rose 11.4 %. The “Other” segment, which includes real estate and ancillary activities, grew 145.7 %, offsetting declines in core gaming operations. Operating income contracted 20.7 % to ¥8,781 million, driven by a 25 % reduction in entertainment operating profit and a 57.2 % decline in amusement facilities; the “Other” segment’s operating profit surged 474.1 %. Net income increased 7.1 % to ¥11,624 million, reflecting a 0.6 % rise in the forecasted year and a modest improvement over the previous fiscal period. Balance‑sheet analysis shows total assets rising 7.9 % to ¥119,461 million, mainly due to higher investment securities and land values. Current assets decreased slightly as cash and receivables fell, while fixed assets grew from ¥83,495 million to ¥92,772 million, largely driven by land acquisitions. Total liabilities increased 5.8 % to ¥12,944 million, with current liabilities rising and long‑term liabilities falling. Shareholders’ equity expanded to ¥105,639 million, supported by retained earnings growth and a reduction in treasury stock. The financial highlights cover Japan‑based operations for FY2016, presenting consolidated income statements and balance sheets in millions of yen. Data are derived from audited financial statements, with segment performance broken down by entertainment, pachislot & pachinko, amusement facilities, real estate, and other activities. The report underscores a shift toward diversified revenue streams amid declining core gaming sales.

Koei Tecmo

Report

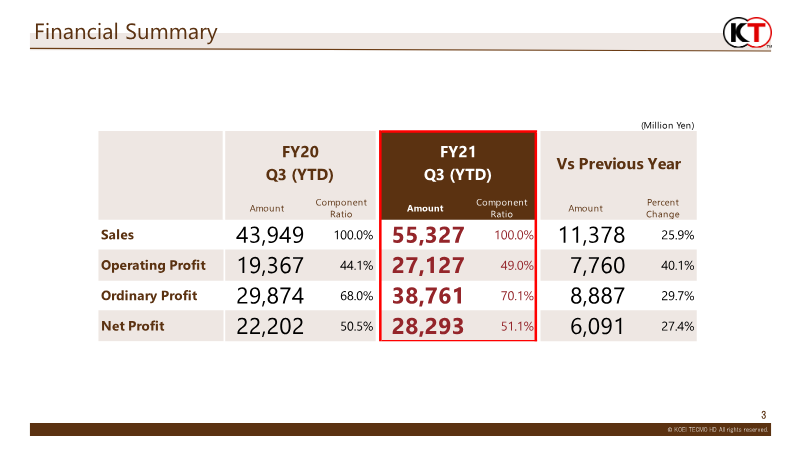

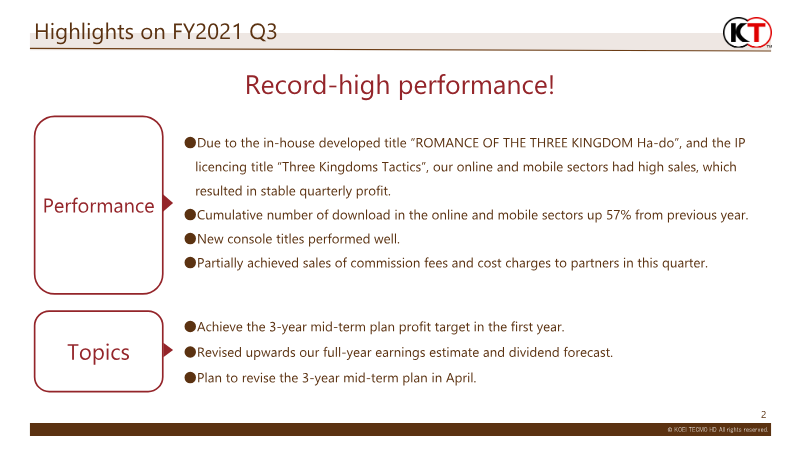

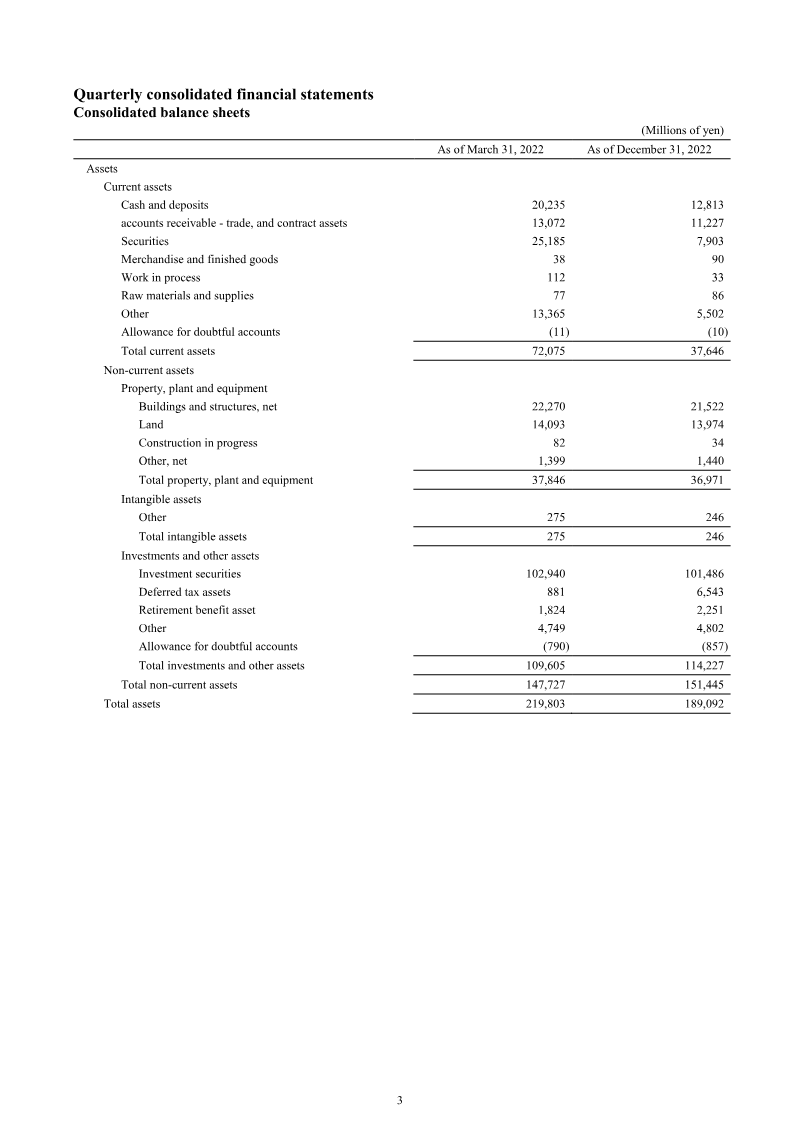

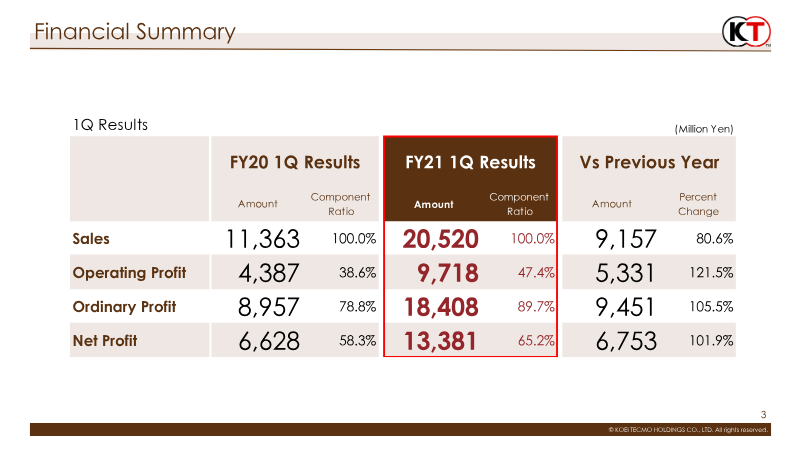

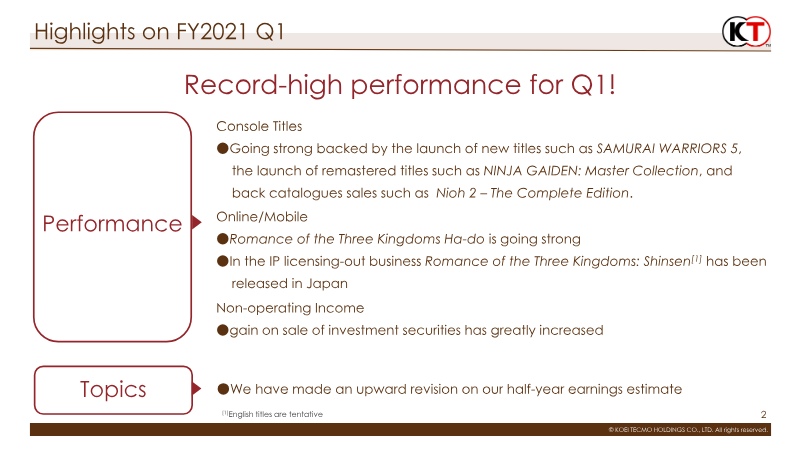

Financial Results for the First Quarter: Fiscal Year Ending March 2022

The financial overview for the first quarter of fiscal 2022 highlights a robust performance driven by new console releases and strong back‑catalogue sales. Total revenue rose 80.6 % from ¥11,363 million to ¥20,520 million, with operating profit more than doubling from ¥4,387 million to ¥9,718 million (121.5 % increase). Ordinary and net profits also surged by 105.5 % and 101.9 %, respectively, reflecting higher margins across the entertainment segment. Revenue composition shifted toward console titles, which accounted for 48.7 % of sales in the overseas market and 38.3 % domestically, supported by launches such as *Samurai Warriors 5* and remastered collections like *Ninja Gaiden: Master Collection*. Online/mobile sales grew 55.8 % in download volume, with the Romance of the Three Kingdoms series expanding into licensing‑out agreements. Non‑operating income benefited from gains on investment securities, prompting an upward revision of the half‑year earnings estimate. Geographically, Japan contributed 38.3 % of sales while overseas markets grew by 51.3 %, with North America and Europe showing mixed results—North America doubled its unit sales, whereas European units fell 26.3 %. Headcount increased by 2.5 % to 2,088 employees, and cost of goods sold rose 22.6 %, largely due to higher production for new titles. Methodologically, the report aggregates quarterly financial statements, sales data by platform and region, and download metrics from the company’s global service portfolio. The analysis underscores a strategic focus on IP licensing, back‑catalogue monetization, and digital distribution to sustain growth in the second half of fiscal 2022.

Koei Tecmo