Investment

Report

Annual Report 2025: Review of Operations

The annual review outlines Square Enix Group’s fiscal 2025 performance, emphasizing continued efforts to strengthen competitiveness across Digital Entertainment, Amusement, Publication, and Merchandising segments. Net sales fell 8.9 % to ¥324.5 billion, yet operating income rose 24.6 % to ¥40.6 billion, and profit attributable to owners surged 63.7 % to ¥24.4 billion, reflecting improved profitability margins. Digital Entertainment sales declined 16.8 % to ¥206.5 billion, but operating income increased 33 % to ¥33.9 billion. The HD Game sub‑segment saw lower sales from new titles but benefited from reduced amortization and advertising costs, while the MMO sub‑segment grew with the launch of “FINAL FANTASY XIV: Dawntrail.” Games for Smart Devices/PC Browser sales fell due to weaker existing titles. Amusement sales rose 15.7 % to ¥71.2 billion, with operating income up 3.7 %. Publication sales dipped 1.1 % to ¥30.8 billion, with operating income down 8.4 %, partly because of a decline in “The Apothecary Diaries” after its anime adaptation. Merchandising sales increased 0.8 % to ¥19.1 billion, and operating income grew 7.2 % to ¥6.1 billion, driven by strong sales of new IP‑based merchandise. Geographically the report focuses on Japan and global markets, covering a full fiscal year ending March 31 2025. Data derive from consolidated financial statements and segment performance analyses, with no external survey methodology noted. The report highlights strategic shifts toward cost control and IP monetization to offset declining sales in certain sub‑segments.

Square Enix

Report

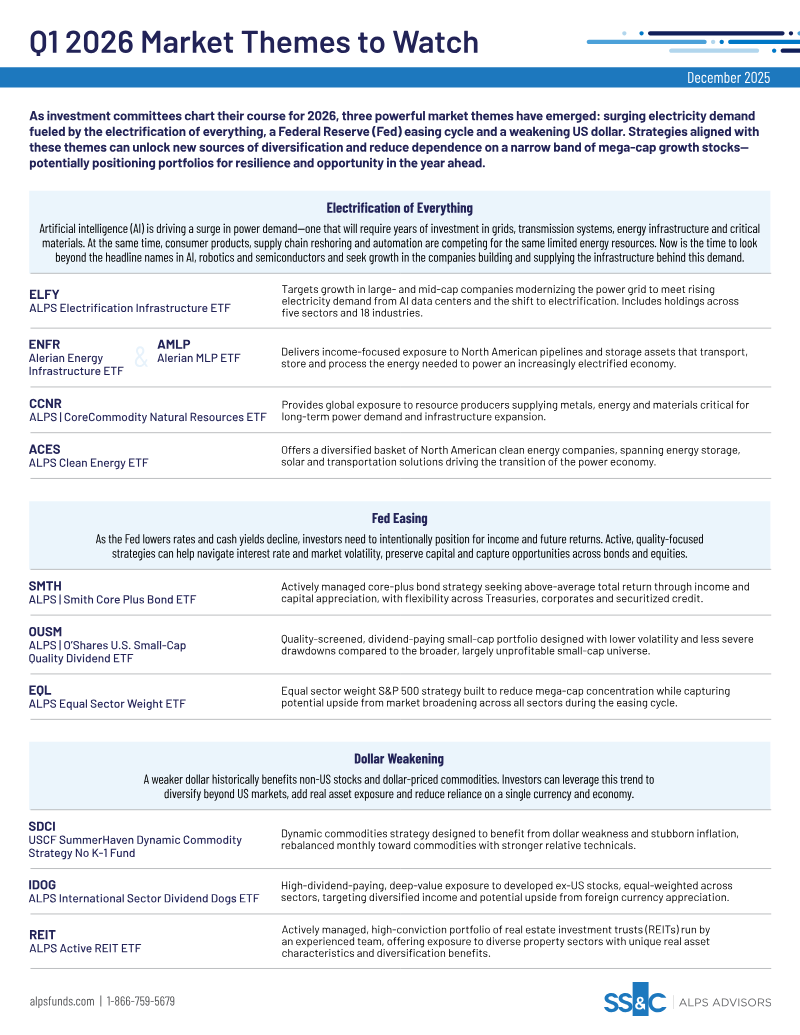

Q1 2026 Market Themes to Watch

Investment committees navigating the 2026 landscape are advised to pivot toward three primary market themes: the widespread electrification of the global economy, the Federal Reserve’s interest rate easing cycle, and the depreciation of the US dollar. These trends offer a strategic framework for diversifying portfolios beyond the narrow concentration of mega-cap growth stocks, potentially enhancing resilience and capturing emerging opportunities across various asset classes. The surge in power demand, driven by artificial intelligence, data center expansion, and industrial automation, necessitates significant capital allocation toward infrastructure. Rather than focusing solely on headline technology firms, investors are encouraged to target the underlying grid modernization, energy transmission, and critical material supply chains. This thematic shift encompasses North American energy pipelines, clean energy solutions, and global natural resource producers, all of which are essential to sustaining an increasingly electrified economy. Simultaneously, the transition toward lower interest rates requires a shift in focus toward quality-oriented income strategies. As cash yields decline, active management in fixed income and the inclusion of quality-screened, dividend-paying small-cap equities can help mitigate volatility and reduce reliance on unprofitable market segments. Furthermore, the anticipated weakening of the US dollar provides a catalyst for diversifying into non-US developed markets and real assets, such as commodities and real estate investment trusts. By rebalancing toward these sectors, investors can hedge against currency risk and inflation while positioning for broader market participation across international and domestic landscapes.

GameVault System