ReportKoei Tecmo

Financial Highlights: Fiscal Year Ending March 2011

1 pages~1 min full read

Key insights

6 takeaways · ~2 min read- 01

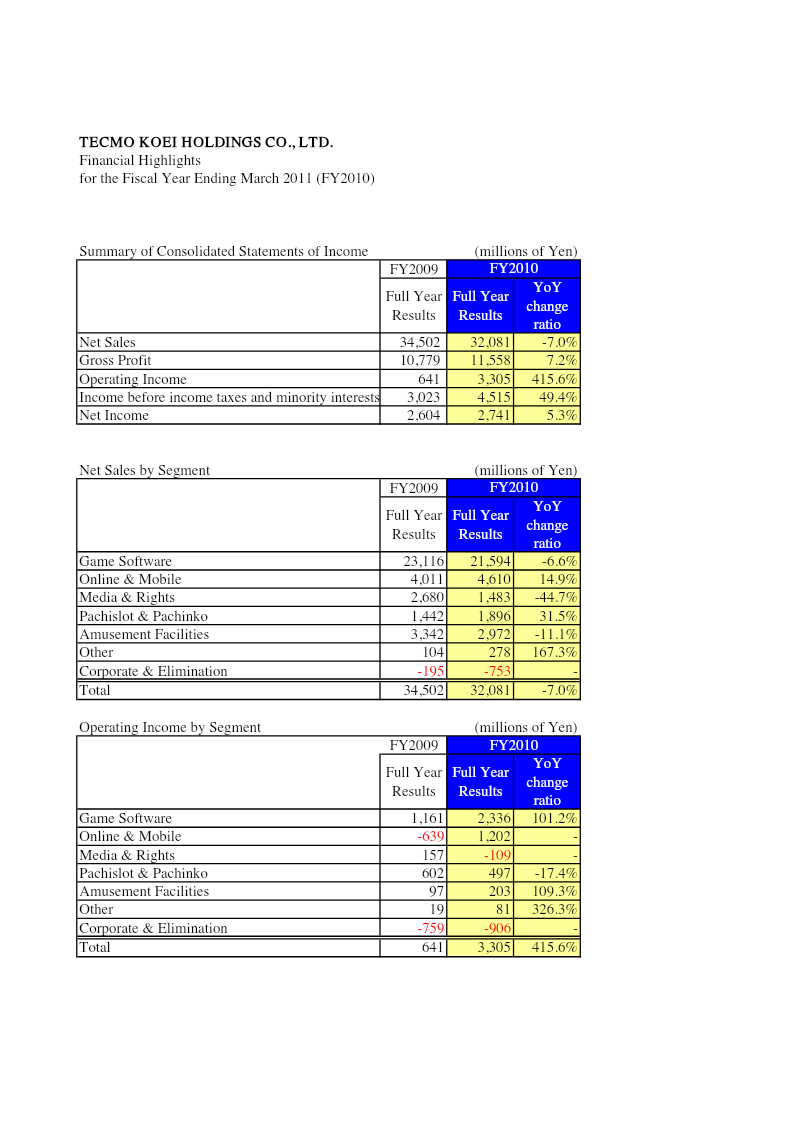

Tecmo Koei Holdings achieved a 415.6% surge in operating income to ¥3,305 million for the fiscal year ending March 2011, despite a 7% decline in net sales to ¥32,081 million.

- 02

Profitability improved significantly through cost efficiencies and high-margin performance, resulting in a 49.4% increase in income before taxes and minority interests to ¥4,515 million.

- 03

The core game software segment saw a 6.6% decline in sales but experienced a 101.2% jump in operating income, indicating a shift toward more profitable operations.

- 04

Revenue diversification efforts showed mixed results, with online & mobile sales growing 14.9% and pachislot & pachinko revenue rising 31.5%, though the latter saw a 17.4% decline in operating income.

- 05

The 'Other' business segment, focused on new initiatives, demonstrated strong growth with a 167.3% increase in sales to ¥278 million and a 326.3% rise in operating income.

- 06

Media & rights revenue performed poorly, dropping 44.7% and contributing negatively to the company's overall operating income for the fiscal year.