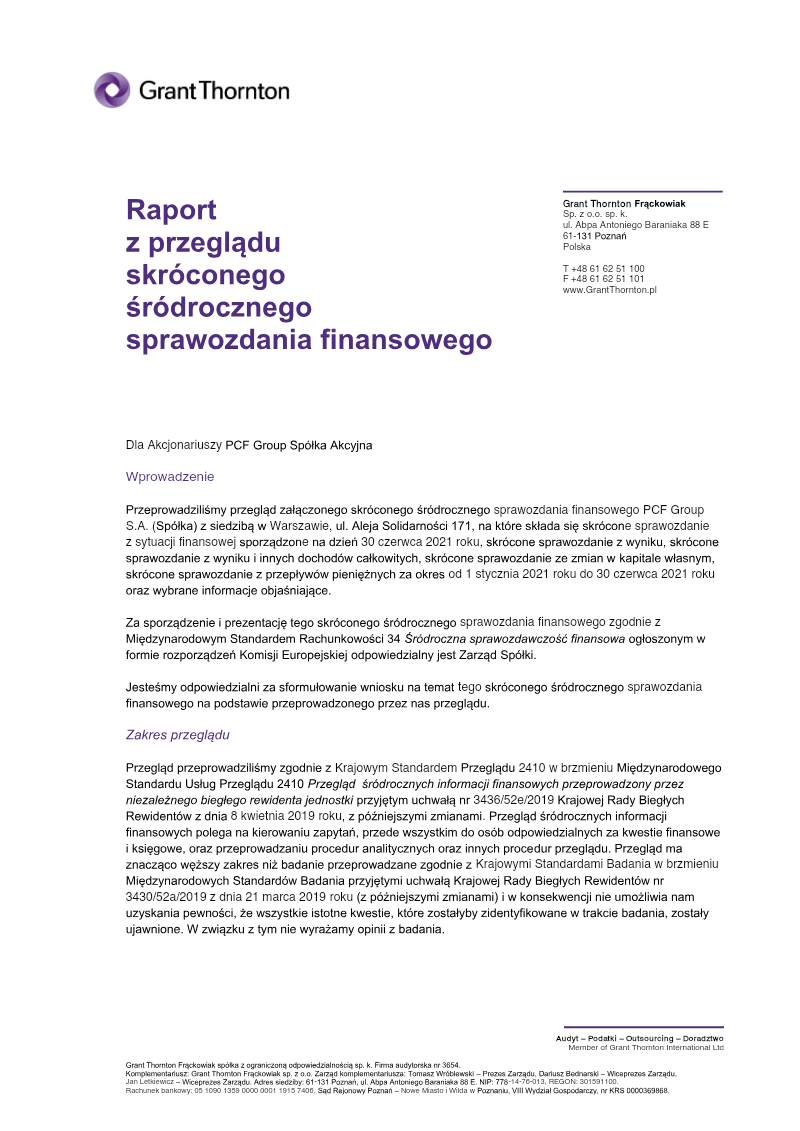

ReportPCF Group

Raport z przeglądu skróconego śródrocznego sprawozdania finansowego: H1 2021

2 pages~3 min full read

Grant Thornton Frąckowiak issued a clean review conclusion for PCF Group S.A.’s condensed half-year financial statements for the period ending 30 June 2021.

See it on page 1The review confirmed that the financial statements were prepared in all material respects in accordance with International Accounting Standard 34 (IAS 34) for interim financial reporting.

See it on page 2The engagement was conducted under the Polish National Standard for Review of Interim Financial Information 2410, which is equivalent to the International Standard on Review Engagements.

See it on page 1The scope of the review was limited to inquiry and analytical procedures, meaning no formal audit opinion was expressed by the reviewers.

See it on page 1The review covered the full suite of financial documents, including the statement of financial position, profit or loss, comprehensive income, changes in equity, and cash-flow statements for H1 2021.

See it on page 1No material irregularities or discrepancies were identified during the review process that would contradict the company's financial reporting compliance.

See it on page 1The report presents the conclusion of an independent review conducted by Grant Thornton Frąckowiak on PCF Group S.A.’s condensed half‑year financial statements for the period from 1 January to 30 June 2021. The review covered the condensed statement of financial position, the condensed statements of profit or loss and other comprehensive income, changes in equity, cash‑flow statement, and selected explanatory notes. The statements were prepared in accordance with International Accounting Standard 34 on interim financial reporting, as adopted by European Union regulations.

The engagement was performed under the Polish National Standard for Review of Interim Financial Information (Standard 2410), equivalent to International Standard on Review Engagements. The review involved inquiry procedures directed at the company’s finance and accounting personnel, analytical procedures, and other review activities. The scope is narrower than a full audit; therefore, the reviewers do not express an audit opinion but provide a review conclusion.

The key finding is that nothing was identified that would lead the reviewers to believe the condensed interim financial statements were not prepared in all material respects in accordance with IAS 34. The conclusion is supported by the procedures performed and the information obtained during the review.

The report covers PCF Group S.A., a Warsaw‑based joint‑stock company, and pertains to the first half of 2021. No specific financial figures or ratios are disclosed in the summary, as the focus is on the review methodology and overall compliance with IAS 34.