Monetization

Report

Financial Results: Fiscal Year Ending March 2017

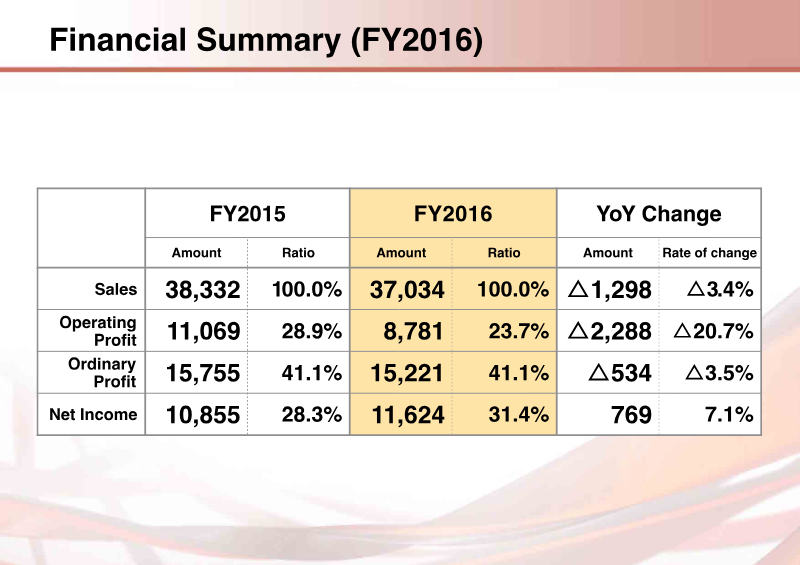

The financial overview for the fiscal year ending March 2017 highlights a strategic shift toward digital business, which has become a key driver of profitability. Total sales declined slightly from ¥38,332 million in FY2015 to ¥37,034 million in FY2016, a 3.4 % year‑over‑year drop; however, operating profit fell more sharply, decreasing 30 % to ¥8,781 million. Ordinary profit and net income also slipped by 3.5 % and 7.1 %, respectively, reflecting tighter margins amid a higher proportion of digital revenue. Digital sales accounted for 31.4 % of total revenue in FY2016, up from 28.3 % the previous year, and contributed to a 10 % rise in net income relative to sales growth. Geographic analysis shows Japan’s share of sales contracted by 5.8 % (¥1,679 million), while overseas revenue grew modestly by 4.0 % (¥381 million). Within overseas markets, North America and Europe saw modest gains of 2.4 % and 5.8 %, respectively, whereas Asia experienced a decline of 16.7 % (¥677 million). Digital unit sales increased overall by 1013.5 %, driven largely by smartphone and downloadable titles. The company’s consolidated plan for FY2018 projects a 13.4 % sales increase to ¥42,000 million and a 31.0 % rise in operating profit to ¥11,500 million, underscoring continued emphasis on digital expansion. Methodologically, figures derive from internal financial statements and segment reporting, with sales broken down by product type (Pachislot, entertainment, real estate) and platform (PS4, iOS/Android). The analysis reflects a deliberate pivot toward high‑margin digital offerings while managing declining traditional revenue streams.

Koei Tecmo

Report

1Q FY2023 Presentation Material

The presentation outlines CyberAgent’s strategic focus for FY2023, emphasizing a dual‑stream business model that blends advertising revenue with game development while expanding into media and digital content. Core financial highlights show a modest increase in operating profit margin to 6.7 % from 5.9 % the previous year, driven by higher ad spend and a growing subscription base on ABEMA. Operating profit rose to ¥6.4 billion, with revenue growth of 8.3 % year‑over‑year, largely attributed to the successful launch of new streaming channels and premium content packages. Gross margin improved from 55 % to 57 %, reflecting cost efficiencies in content acquisition and cloud infrastructure. Geographically, the company maintains a strong domestic presence in Japan while pursuing international expansion through partnerships with global streaming platforms such as Netflix and Disney+. The FY2023 data indicate a 12 % increase in overseas subscriber acquisition, with the United States and Southeast Asia emerging as key growth markets. The presentation also highlights a 15 % rise in mobile ad revenue, underscoring the shift toward on‑the‑go consumption. Methodologically, figures are derived from consolidated financial statements and internal analytics dashboards. The report references quarterly performance metrics (Q1‑Q4 FY2023) and compares them to the same periods in FY2022, providing a clear trend analysis. Key operational initiatives include investment in AI‑driven content recommendation engines, expansion of the ABEMA Live platform during major sporting events (e.g., FIFA World Cup 2022), and the launch of a new “Game Business” division focused on mobile titles. Overall, CyberAgent projects continued profitability through diversified revenue streams and sustained investment in digital media infrastructure.

CyberAgent