Market Analysis

Report

Consolidated Financial Results: Q3 Fiscal Year 2026

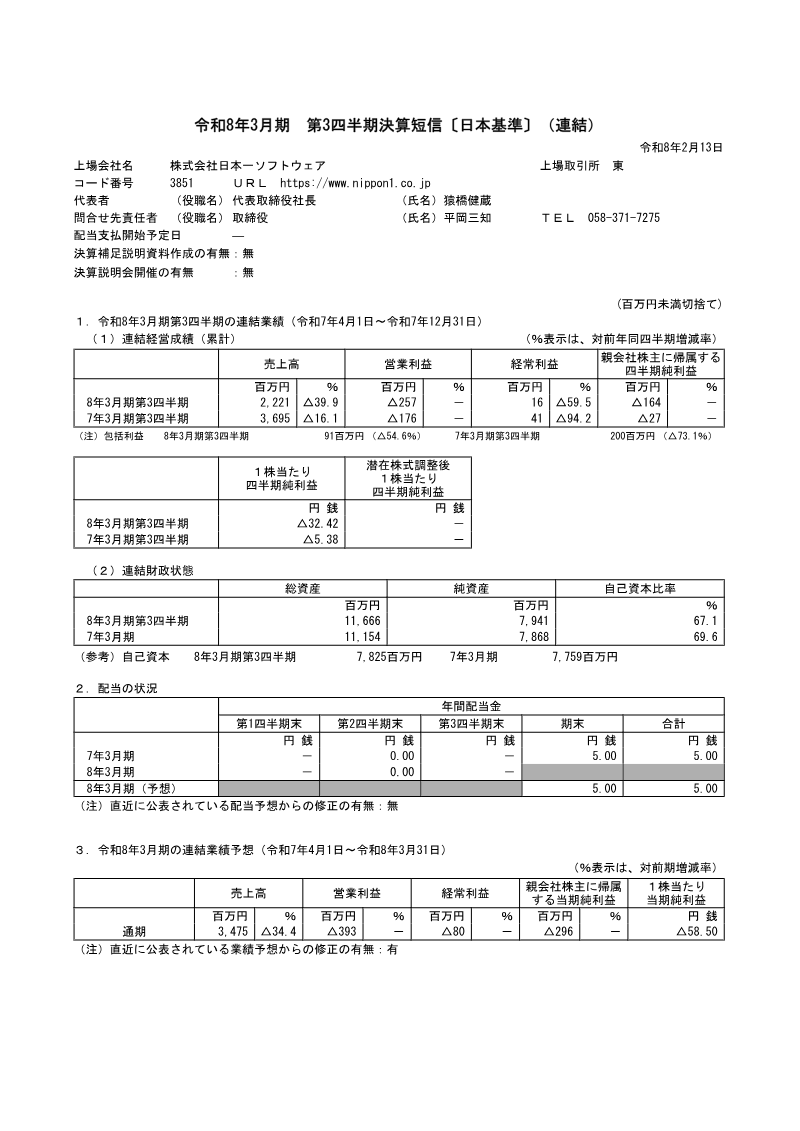

The quarterly consolidated financial results for the period ending March 2026 reveal a sharp contraction in revenue and profitability across the company’s entertainment and student‑housing segments. Total sales fell 39.9 % to ¥2,221 million, while operating loss widened to ¥257 million from a prior‑year loss of ¥176 million. Ordinary profit dropped 59.5 % to ¥16 million, and net loss attributable to parent shareholders rose to ¥164 million from ¥27 million. Segment analysis shows the entertainment business generated ¥2,132 million in sales but incurred a loss of ¥257 million; the student‑housing unit posted higher sales of ¥89 million but a smaller loss of ¥16 million. The company’s total assets increased to ¥11,667 million, driven mainly by cash and inventory gains, while liabilities rose to ¥3,725 million. Shareholders’ equity grew modestly to ¥7,942 million, with a 67.1 % equity ratio. The company forecasts a full‑year decline in sales of 34.4 % to ¥3,475 million and operating loss of ¥393 million, with net loss projected at ¥80 million. Dividend policy remains unchanged, with no interim dividend announced for the quarter and a forecast of ¥5 million per share in the year. No significant accounting policy changes or material adjustments were reported, and the auditor issued a clean review opinion on the interim financial statements. The results reflect broader industry pressures, including inflation‑driven consumer restraint and competitive dynamics in the gaming market.

Nippon Ichi Software

Report

FY2017 Second Quarter Financial Results

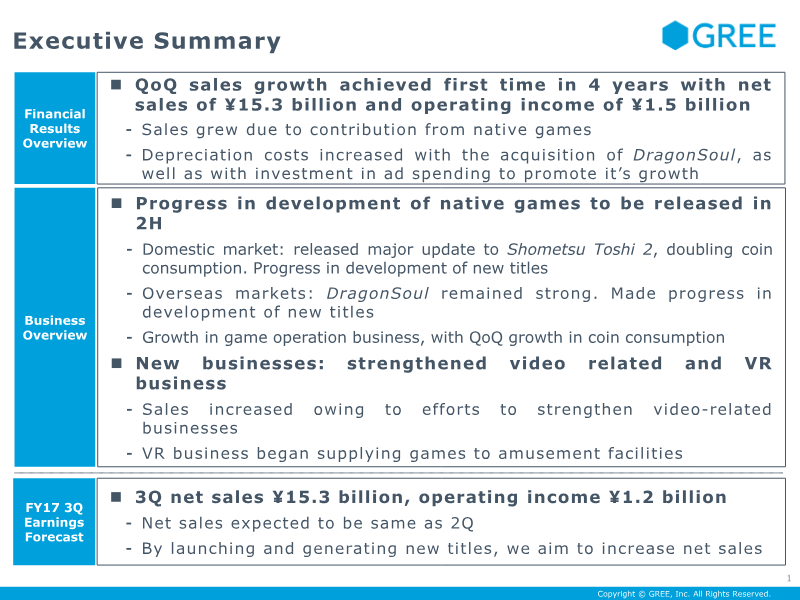

The FY2017 second‑quarter results demonstrate a first quarterly sales growth in four years, with net sales reaching ¥15.3 billion and operating income of ¥1.5 billion. Growth is attributed mainly to native game releases, particularly the major update of *Shometsu Toshi 2* and the launch of *Rara‑MAGI*, which together doubled coin consumption. Overseas performance remained strong through the acquisition of DragonSoul, contributing ¥1.43 billion in ad‑media sales. Operating costs rose by ¥1.5 billion QoQ, driven by increased advertising spend and higher depreciation linked to the DragonSoul acquisition. Variable costs grew modestly, while fixed costs—including labor and outsourcing—expanded as new titles entered development. EBITDA fell to ¥2.07 billion, reflecting the investment push. The company forecasts FY17 third‑quarter net sales to match the second quarter at ¥15.3 billion, but expects operating income to decline to ¥1.2 billion due to higher fixed costs from upcoming 2H releases. Management emphasizes continued investment in native game development, video‑related businesses (notably the 3Minute platform and VR attractions), and overseas expansion to sustain revenue growth. Geographically, domestic Japanese markets drive native game performance, while overseas operations benefit from DragonSoul and other first‑party titles. The period covered is the fiscal year 2017, with a focus on Q2 performance and forward guidance for Q3. The analysis relies on consolidated financial statements, cost breakdowns, and operational updates provided in the quarterly report.

GREE