ReportInvestGame

How Developers Are Using Generative AI to Create a New Generation of Games

19 pages~15 min full read

The study demonstrates that generative AI is reshaping game development across the United States, South Korea, Norway, Finland, and Sweden. Surveying 615 developers in late June‑early July 2025, it finds that 97 % believe AI is transforming the industry and 90 % already use it in their work. Key impacts include streamlining repetitive tasks, accelerating play‑testing and localization, improving code generation, and enabling dynamic balancing. AI agents are emerging as a new trend; 44 % deploy them for content optimization, 38 % for dynamic gameplay tuning, and another 38 % for in‑game coaching. These agents leverage multimodal inputs to create responsive NPCs, adaptive difficulty, and personalized tutorials, thereby raising player expectations—89 % of respondents report that gamers now demand smarter, more adaptive experiences.

The survey highlights both opportunities and challenges. While 94 % anticipate long‑term cost reductions, 25 % struggle to measure ROI and 24 % cite limited training data. Intellectual‑property concerns dominate, with 63 % worried about data ownership and 32 % uncertain over licensing of AI‑generated content. Despite these risks, developers see AI as a catalyst for new business models and creative horizons, such as emergent gameplay and real‑time world changes. Best practices identified include starting small, aligning AI with creative vision, investing in talent, and establishing clear success metrics. Overall, the findings suggest a rapidly expanding role for generative AI that promises greater efficiency, democratization of development tools, and richer player experiences while underscoring the need for careful governance around IP and data privacy.

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2026

InvestGame · 2025

InvestGame · 2025

InvestGame · 2025

Game Developers Conference · 2025

Google Cloud · 2025

Informa · 2024

Drake Star Partners · 2024

Perforce · 2024

Modern Times Group

Poki · 2026

Sensor Tower · 2026

SocialPeta · 2026

GDC · 2026

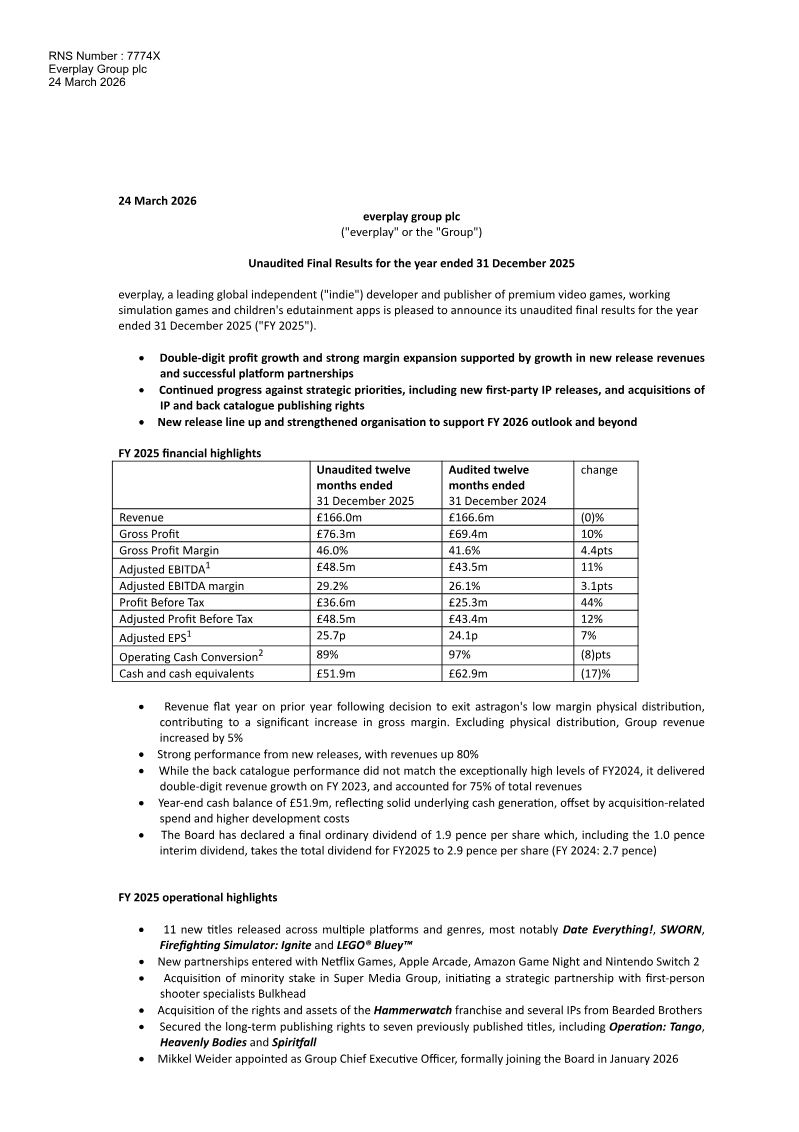

Everplay Group · 2026

BITKRAFT Ventures · 2026