The document argues that artificial intelligence has become a strategic asset in mobile game development, transforming every phase of the lifecycle from ideation to live operations. It claims that AI enables teams to prototype, test, and launch content at a fraction of the time previously required, citing examples such as concept‑art generation in days instead of months and single‑person prototype teams that reduce sunk costs. The thesis emphasizes that the combination of trillions of player data points, world‑class creative teams, evergreen intellectual property, and AI as a workflow enabler creates a competitive moat that is difficult to scale for rivals.

Key findings include a 99 % cost reduction in marketing asset creation, an 80 % time saving on influencer spotlights, and a 75 % reduction in analyst turnaround times when querying data through AI agents. The document reports that five new games launched in 2026 adopted an “AI‑first” approach, allowing rapid iteration and simultaneous development of specialized content. It also highlights that AI agents can analyze A/B tests, suggest optimizations, and generate localized UGC‑style assets to lower CPI and improve player engagement.

The scope covers the global mobile gaming market, focusing on mid‑core titles with large player bases. Methodology is implied through internal tooling: 50+ AI platforms (e.g., Claude, Cursor, ComfyUI) and BigQuery‑based agents that process terabytes of data daily. The analysis suggests that AI integration not only accelerates production but also democratizes data insights, freeing analysts to tackle higher‑level strategic questions.

Modern Times Group · 2026

Modern Times Group · 2026

Modern Times Group · 2025

Modern Times Group · 2025

Modern Times Group · 2025

Modern Times Group · 2023

Modern Times Group · 2019

Modern Times Group · 2019

Modern Times Group · 2018

Modern Times Group · 2018

Modern Times Group · 2017

Modern Times Group · 2017

Google Cloud · 2025

Game Developers Conference · 2025

Informa · 2024

Drake Star Partners · 2024

Perforce · 2024

InvestGame

Poki · 2026

Sensor Tower · 2026

SocialPeta · 2026

GDC · 2026

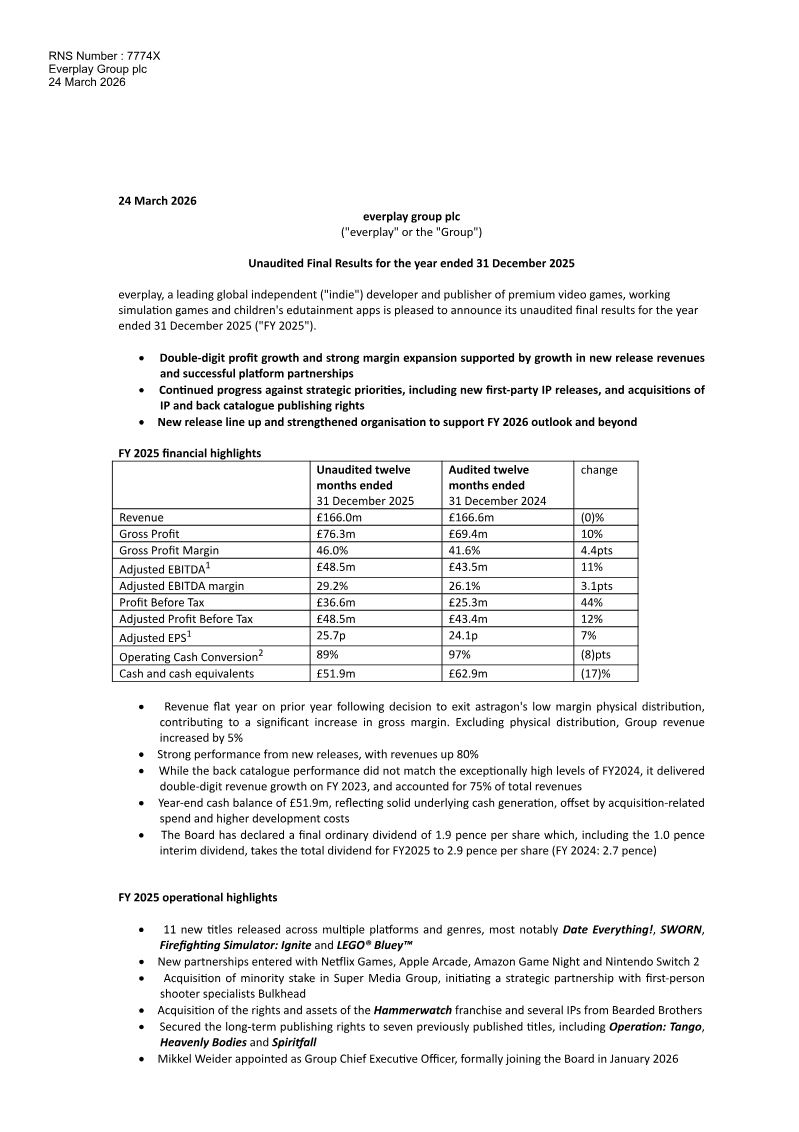

Everplay Group · 2026

BITKRAFT Ventures · 2026