FinancialEverplay Group

Unaudited Final Results for the Year Ended 31 December 2025

26 Mar 202623 pages~65 min full read

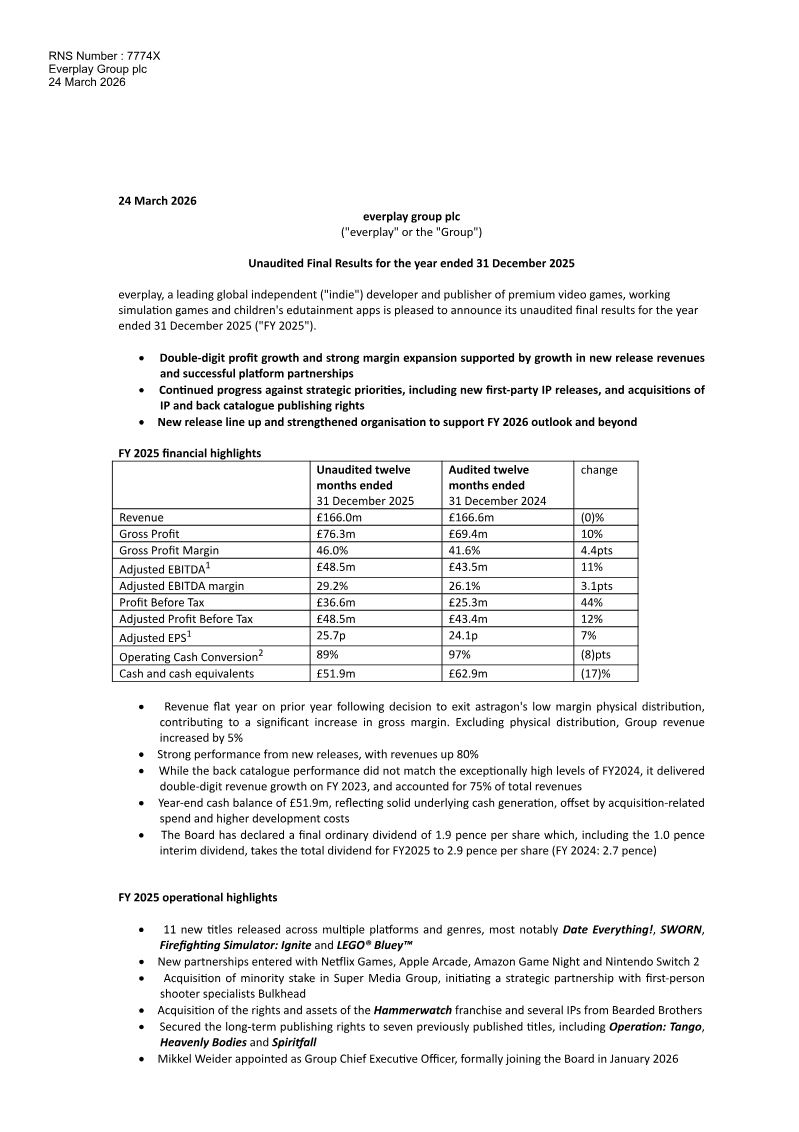

Everplay Group plc delivered unaudited FY 2025 results that demonstrate resilient profitability amid flat headline revenue. Total sales held steady at £166.0 million, a slight decline from the prior year, yet underlying revenue grew 5 % when excluding the impact of Astragon’s exit from physical distribution. Gross profit rose to £76.3 million, achieving a 46.0 % margin, while adjusted EBITDA increased 11 % to £48.5 million (29.2 % margin). Profit before tax surged 44 % to £36.6 million, driven by higher gross margins and reduced royalty expenses.

The Group’s performance was underpinned by robust new‑release activity, with an 80 % revenue increase from fresh titles and a 75 % share of income derived from its back catalogue. Strategic initiatives—such as securing platform partnerships with Netflix Games, Apple Arcade and Amazon Game Night, exiting low‑margin physical distribution, and acquiring additional IP rights—position the company for future growth. Astragon’s revenue fell 33 % to £29.5 million after the distribution exit, yet its first‑party IP share climbed to 83 % of sales; StoryToys expanded revenue by 25 % to £30.4 million, buoyed by high‑profile licenses like LEGO® Bluey and Netflix Games.

Share‑based remuneration expanded, with 317,970 options granted to Executive Directors, 349,805 to other employees and 87,957 to Non‑Executive Directors in FY 2025. The Long‑Term Incentive Plan now covers senior divisional leaders, and an All‑Employee Share Incentive Plan remains active. Outlook for FY 2026 highlights a pipeline of over 15 new games, including five first‑party IP titles, and anticipates H2‑weighted EBITDA growth.

Financially, the Group reports a single aggregated segment comprising Games Label, Simulation and Edutainment. Revenue in 2025 split evenly between first‑party (£56.13 m) and third‑party IP (£109.86 m), with major platforms such as Steam, Microsoft, Sony, Nintendo and Apple each contributing over 10 % of sales. Operating profit benefited from amortisation of development costs (£14.16 m) and publishing rights, while tax expense rose to £9.35 million from £5.13 million in 2024 due to higher current and deferred tax adjustments.

Goodwill impairment testing revealed no shortfalls except for the Astragon Simulation CGU, where recoverable amounts exceed carrying value by £78.5 million (2024: £31.0 million). Sensitivity analysis indicates that a 25 % decline in unreleased title revenues would bring the Astragon CGU to breakeven, but no other reasonable changes trigger impairment. Cash balances remained robust at £51.9 million in 2025, with operating cash flow of £57.7 million slightly below the prior year’s £59.9 million, underscoring solid liquidity and a foundation for continued profitable expansion.

Thunderful · 2025

Koei Tecmo · 2010

InvestGame

Frontier Developments

Frontier Developments

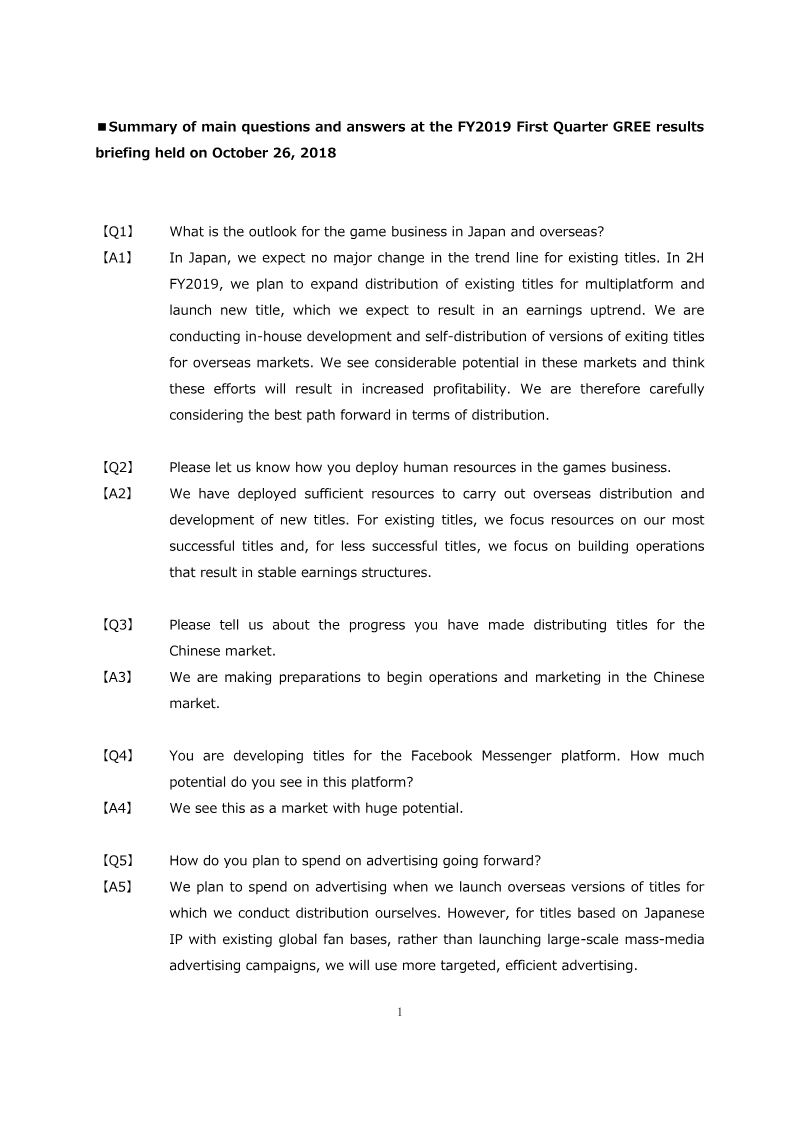

GungHo Online Entertainment

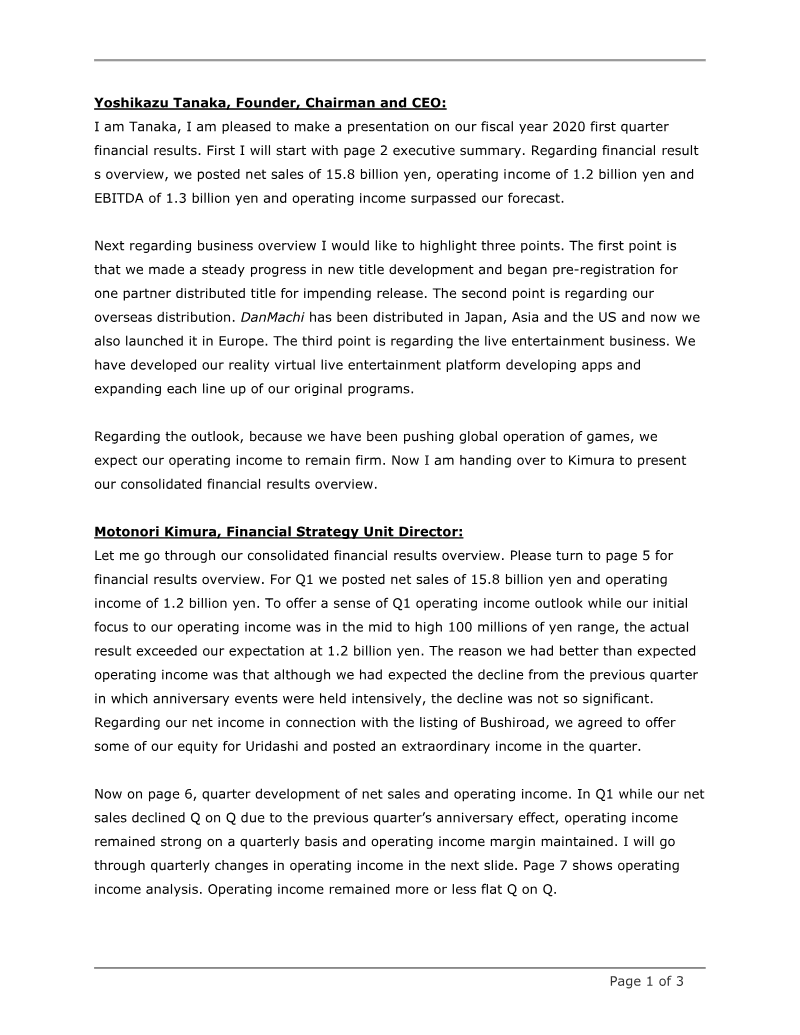

GREE

GREE

InvestGame

Sega Sammy Holdings

Frontier Developments

IGN Entertainment · 2026