Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Newzoo | Game Industry Library

Writers

Newzoo

Back to Writers

Newzoo

Research

93 documents

Documents

Reports

Presentations

Whitepapers

Articles

Financial

Legal

Other

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

94 pages

PC & Console Gaming Report 2025

Console revenue is projected to grow at a 13% CAGR through 2027, significantly outpacing single-digit growth for PC, with major catalysts including the release of GTA VI and the Nintendo Switch 2.

Market dominance is heavily concentrated in established franchises, as new releases captured only 9% of total playtime in 2024, with annual franchises accounting for 67% of new-release hours on consoles.

Title diversity is shrinking, evidenced by a 27% decline in the average number of titles played per user on Steam in the US, with drops as high as 34% in markets like Russia and Brazil.

Market Analysis

Player Demographics

Player Behavior

+1

Newzoo

Jan 2025

Report

26 pages

Newzoo Puzzle Games Report: Mobile Game Genre Insights

The United States is the world's largest mobile puzzle market, followed by Japan and China.

Western puzzle games rely heavily on in-app advertising (IAA) and simple economies, while Eastern titles—especially in Japan—prioritize deep character collection and gacha mechanics to drive higher in-app purchase (IAP) revenue.

Western players demonstrate a higher tolerance for frequent ad breaks, whereas Japanese players prefer longer, uninterrupted sessions and show a greater willingness to pay for aesthetic enhancements and additional functions.

Market Analysis

Player Demographics

Global

+2

Newzoo

Jan 2025

Report

24 pages

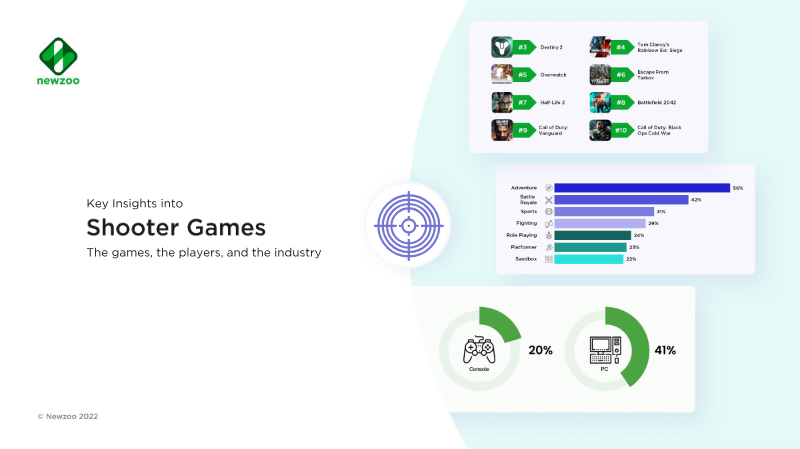

Key Insights into Shooter Games

Shooter games generated approximately $2.24 billion in 2022 across 37 global markets, excluding China and India.

Shooters are a dominant force on PC and console platforms, capturing 68% of monthly active users.

Monetization in the genre is heavily driven by in-app purchases, which are experienced by 97% of shooter players, while advertising remains the least utilized revenue model.

Market Analysis

Global

Shooter

+2

Newzoo

Jan 2025

Report

17 pages

Diversity and Inclusion in Gaming: Newzoo & Intel Report

Nearly 50% of U.S. gamers are more likely to support publishers that take active stances on social justice issues, signaling a shift in consumer expectations toward corporate responsibility.

47% of U.S. gamers actively avoid titles they perceive as not being designed for them, highlighting a significant barrier to market penetration for non-inclusive content.

Black and Hispanic/Latinx gamers are younger and more engaged than white counterparts, with 75% of Black PC players under the age of 35 compared to 50% of white players.

Diversity & Inclusion

Player Demographics

Market Analysis

+1

Newzoo

Jan 2025

Report

67 pages

Global Games Market Report 2025

The global games market is projected to reach $188.8 billion in 2025, a 3.4% year-over-year increase, with mobile platforms accounting for 55% of total revenue at $103 billion.

Mobile gaming remains the primary growth engine with a 4.5% year-over-year expansion, while PC and console segments grow at 3.1% and 2.5% respectively.

Single-player AAA titles launched between February and May outperform those released in the August–November holiday window by an average of 34% due to reduced market cannibalization.

Market Analysis

Monetization

Global

Newzoo

Jan 2025

Report

30 pages

Global Gamer Study 2024: How Consumers Engage with Games Today

Gaming is a primary entertainment pillar, with 80% of the global online population playing games and 85% engaging through play, viewing, or social communities.

Gen Alpha and Gen Z are the most active demographics, with over 90% engagement and Gen Alpha spending 5.2 hours per week on gaming, surpassing their time spent on social media.

A high-value segment of 'new game seekers' makes up 31% of PC and console players; these users are 50% more engaged than average players and 80% of them spend money on games monthly.

Market Analysis

Player Demographics

Player Behavior

+1

Newzoo

Jul 2024

Report

52 pages

Global Games Market Report 2023

The global video game market is projected to reach $183.9 billion in consumer spending across 3.3 billion players in 2023.

The Asia-Pacific region accounts for 46% of global gaming revenue, though it experienced a 0.2% year-over-year decline due to downturns in China, Japan, and South Korea.

Shooter games are the leading PC category, generating $5.5 billion in revenue and achieving 4.9% year-over-year growth.

Market Analysis

Monetization

Global

Newzoo

May 2024

Report

20 pages

The Ultimate Game Hype Tracking Guide

Success in the PC and console market requires tracking the purchase funnel through three core metrics: unaided awareness, aided awareness, and purchase intent conversion rates.

The Game Health Tracker methodology relies on monthly surveys of over 3,000 PC and console players in the United States to benchmark performance against competitors.

Conversion rate, defined as the percentage of aided-aware players who express purchase intent, serves as the primary indicator for measuring marketing effectiveness.

Market Analysis

User Acquisition

Retention

+3

Newzoo

Feb 2024

Report

46 pages

Newzoo PC & Console Gaming Report 2024

The market is highly consolidated, with 28 to 34 publishers capturing 80% of monthly active users and just two titles, Fortnite and Roblox, commanding over 60% of total playtime in 2023.

Engagement is dominated by legacy content, as older titles account for over 60% of total hours played, while new releases capture only 8% of playtime.

Premium transactions remain the primary revenue driver, accounting for 56–57% of total spending and outperforming live-service and subscription models.

Market Analysis

PC

Console

+1

Newzoo

Jan 2024

Report

27 pages

Games Market Trends 2024

The global games market is entering a recovery phase with a projected Compound Annual Growth Rate (CAGR) of +1.3% through 2026.

The live-service market is consolidating, with just 19 titles currently capturing 60% of total player engagement, prompting a strategic shift back toward premium, finite gaming experiences.

Developers are increasingly mitigating financial risk by prioritizing established Intellectual Property and sequels over new, unproven concepts.

Market Analysis

Market Forecast

Monetization

+1

Newzoo

Jan 2024

Report

27 pages

Games Market Trends to Watch in 2024

The global games market is in a period of stabilization and recovery throughout 2024, supported by the growing install base of current-generation consoles like the PlayStation 5 and Xbox Series X|S.

Developers are increasingly pivoting back to premium, finite gaming experiences to counter the oversaturation of the live-service market.

Mobile developers are expanding to PC platforms to mitigate the impact of rising user acquisition costs and stricter privacy regulations.

Market Analysis

Market Forecast

Player Demographics

+1

Newzoo

Jan 2024

Report

46 pages

The PC & Console Market Gaming Report 2024

The PC and console market reached $93.5 billion in 2023, reflecting a 2.6% growth rate despite a 26% decline in average quarterly playtime since 2021.

Market dominance is highly consolidated, with approximately 30 publishers controlling 80% of all monthly active users.

Games six years or older command over 60% of total playtime, while new, non-annual original titles struggle to capture more than 8% of player attention.

Market Analysis

Global

PC

+1

Newzoo

Jan 2024

Previous

1

2

3

…

8

Next