Console revenue is projected to grow at a 13% CAGR through 2027, significantly outpacing single-digit growth for PC, with major catalysts including the release of GTA VI and the Nintendo Switch 2.

See it on page 14Market dominance is heavily concentrated in established franchises, as new releases captured only 9% of total playtime in 2024, with annual franchises accounting for 67% of new-release hours on consoles.

See it on page 33Title diversity is shrinking, evidenced by a 27% decline in the average number of titles played per user on Steam in the US, with drops as high as 34% in markets like Russia and Brazil.

See it on page 47Player growth remains incremental, with annual increases of 3.5% for console and 2.3% for PC, driven primarily by legacy brands rather than breakthrough innovation.

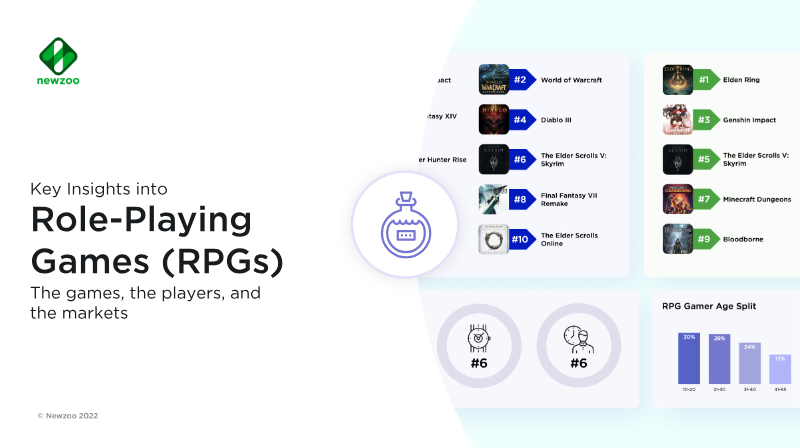

See it on page 16Genre preferences are shifting away from Battle Royale toward Adventure and Role-Playing titles, signaling a market trend toward narrative-rich, long-form gameplay.

See it on page 64Long-term commercial success for new intellectual property requires prioritizing live-service strategies and continuous content updates to compete against the revenue dominance of established annual franchises.

See it on page 91Global PC and console revenues are expected to grow modestly through 2027, with consoles driving the majority of expansion at an estimated +13 % CAGR while PC revenue rises only in single digits. 2024 saw a plateau for PCs, dominated by free‑to‑play and in‑game monetisation, whereas console sales are set to rebound from 2025 thanks to strong releases such as GTA VI and the launch of Nintendo Switch 2. Player growth remains incremental, with PC players increasing at +2.3 % annually and console players at +3.5 %, driven largely by established franchises rather than breakthrough innovation.

Playtime data confirm that 2024 experienced a 6 % YoY increase, with Pay‑to‑Play titles (e.g., Call of Duty) and free‑to‑play hits (Fortnite, Roblox) accounting for most of the lift. New releases captured only about 9 % of total playtime, underscoring that long‑running series dominate the market. Console audiences remain heavily slate‑dependent: 67 % of new‑release hours come from annual franchises, while PC players show a higher share of non‑annual titles. In the US and Western Europe, non‑annual franchise games contribute a smaller slice of console revenue (≈8–22 %) compared to annual franchises, which drive the bulk of earnings.

Engagement patterns reveal a sharp decline in title diversity on PC and Xbox, with the average number of titles played per player falling 27 % on Steam in the US and up to 34 % in Russia and Brazil. PlayStation, by contrast, shows modest growth in title engagement. Genre preferences are shifting away from Battle Royale toward Adventure and Role‑Playing, reflecting a broader industry trend toward narrative‑rich, long‑form gameplay. Nostalgia and free‑to‑play models continue to sustain short‑term spikes, but long‑term retention hinges on continuous content updates and robust live‑service strategies. New IPs must prioritize originality, polished gameplay loops, and community‑first discovery to overcome the legacy brand advantage and achieve lasting commercial success.