Back to Writers

GREE

Organization

256 documents

Documents

Report

Financial Results for the First Quarter: Fiscal Year Ended June 30, 2011

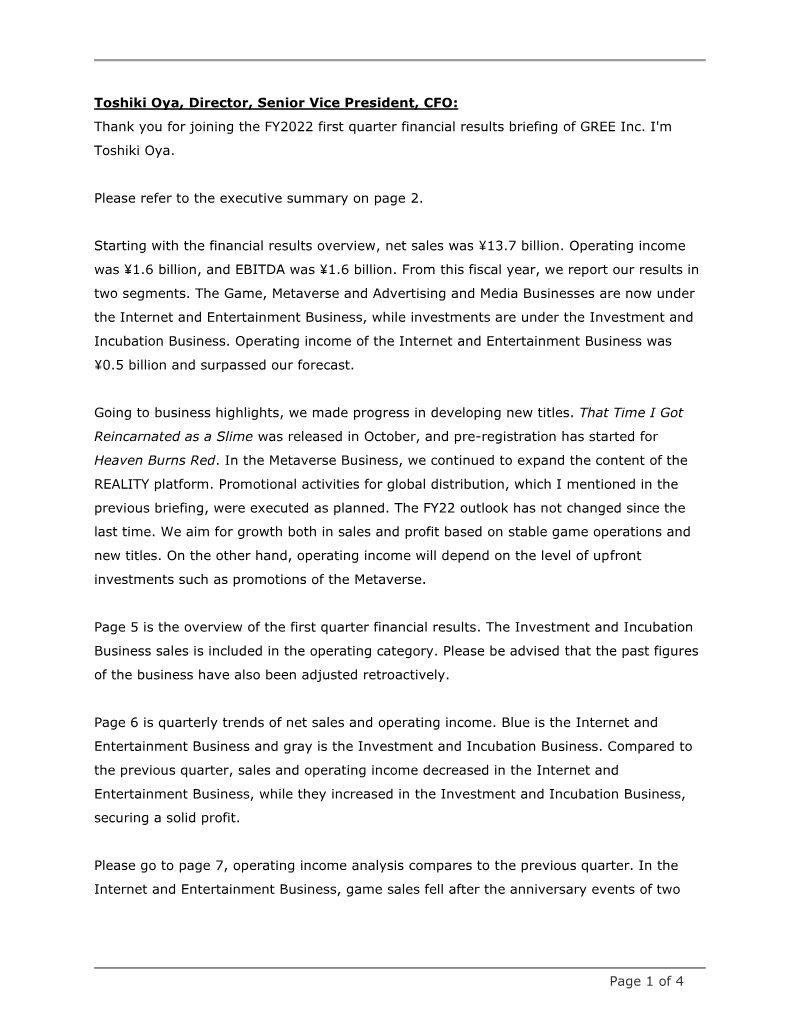

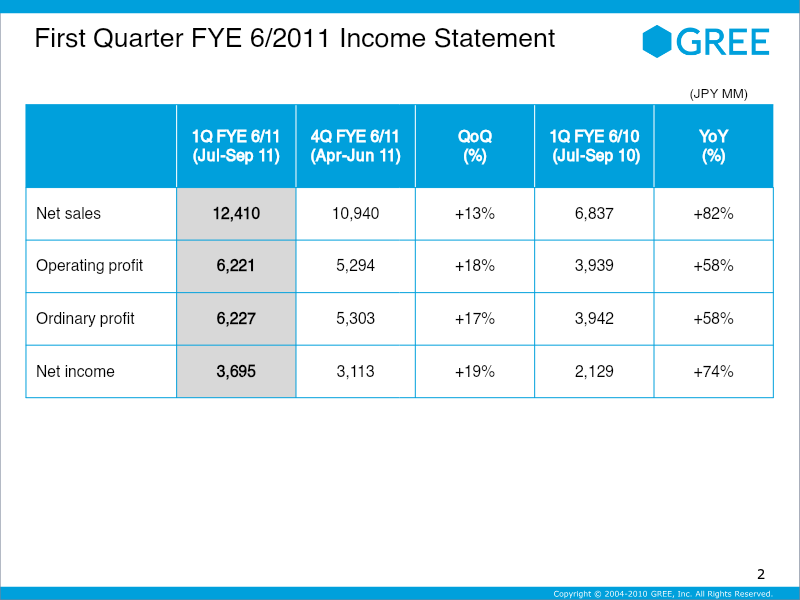

GREE, Inc. reported first‑quarter financial results for the fiscal year ending June 30 2011, showing a 13 % rise in net sales to ¥12.41 billion versus the prior quarter and an 18 % increase in operating profit to ¥6.22 billion. Net income climbed 19 % to ¥3.70 billion, driven by higher paid‑service and advertisement revenues linked to new first‑party titles such as “Pirate Kingdom Columbus” and the launch of a monthly fee plan for “Hacöniwa.” The company’s user base reached 22.46 million members by September 2010, with 46 % aged over 30, and mobile traffic accounted for a growing share of page views. Operating expenses rose modestly; cost of sales increased by 25 % mainly due to higher rental charges, while advertising spend grew 22 %. Labor costs and SG&A expenses also rose, reflecting continued investment in development and marketing. Cash flow from operations turned negative for the quarter, offset by a significant inflow of ¥8.78 billion from investment activities and a reduction in financing cash outflows. GREE expanded its platform by opening the “GREE Platform” to third‑party developers, partnering with hosting and customer‑support firms, and launching a mobile service on smartphones. Geographic outreach plans include opening offices in Asia and North America and partnering with Project Goth, Inc. to tap emerging‑market mobile SNSs. The company maintained a robust safety framework through its GREE Patrol system and age‑restriction policies, reinforcing user protection amid rapid growth.

GREE

Report

FY2025 Second Quarter Financial Results Briefing

The briefing presents FY2025 second‑quarter financial results for GREE Holdings, emphasizing a revised disclosure structure that separates the Investment Business from the other three operating segments—Game and Anime, Metaverse, and DX. Consolidated net sales reached ¥15.6 billion with operating profit of ¥2.2 billion, both up QoQ and YoY, driven by foreign‑exchange gains and strong dividend income from investment funds. On a three‑segment basis, net sales were ¥13.7 billion and operating profit ¥1.2 billion, surpassing prior forecasts. Segment performance highlights include a record‑high ¥2.1 billion in Metaverse sales, driven by avatar and live‑streaming revenue; Game and Anime sales rose QoQ thanks to anniversary events for flagship titles, though YoY growth slowed; DX Business maintained forecasted sales of ¥1.8 billion, with a shift toward recurring SaaS and consulting services. The Investment Business posted significant gains from fund dividends, offsetting a prior quarter loss; portfolio valuation climbed to ¥36.3 billion with IRR outperforming VC benchmarks. Management reiterated medium‑term targets: FY2027 sales of ¥17.9 billion and operating profit of ¥3.3 billion, with continued investment in Metaverse, DX recurring models, and diversified fund sourcing. The briefing covered 2025 full‑year forecasts—sales of ¥8.7 billion and operating profit of ¥500 million for Metaverse, ¥7.3 billion and ¥800 million for DX—reflecting modest sales adjustments but confidence in margin improvement. Overall, the presentation underscores robust quarterly growth across core segments and a strategic pivot toward higher‑margin recurring revenue streams.

GREE