Back to Writers

GREE

Organization

256 documents

Documents

Report

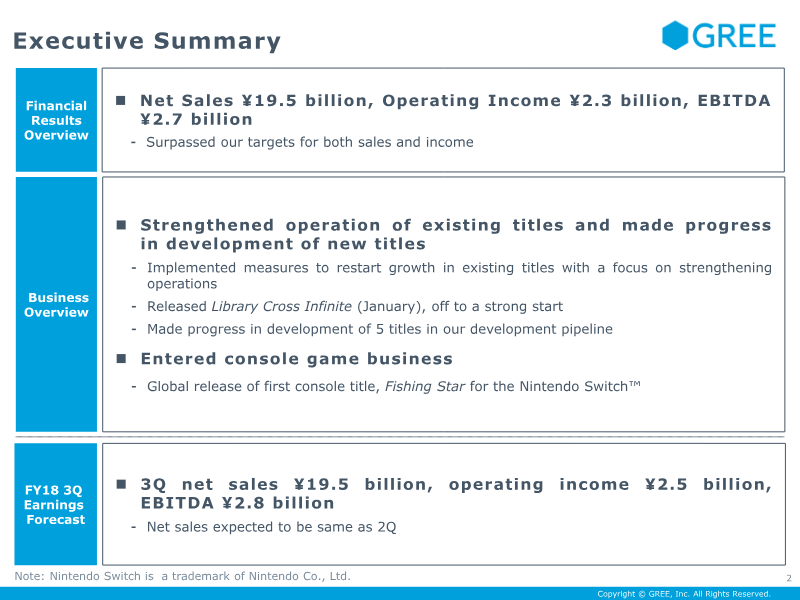

FY2018 Second Quarter Financial Results

The FY2018 second‑quarter results demonstrate a successful rebound in sales and profitability, with net sales reaching ¥19.5 billion and operating income at ¥2.3 billion, slightly below the prior quarter but still surpassing year‑on‑year targets. EBITDA stood at ¥2.7 billion, reflecting a 12.0 % operating margin that narrowed by 0.5 percentage points QoQ. Revenue was dominated by paid‑service sales (¥17.21 billion) and ad‑media sales (¥2.25 billion). Cost control initiatives reduced total costs by ¥1.8 billion QoQ, driven mainly by lower advertising spend and commission fees; variable costs fell ¥1.92 billion while fixed costs remained stable. Strategically, the company expanded its portfolio by launching “Library Cross Infinite” in January and entering the console market with the Nintendo Switch title “Fishing Star.” Development pipelines now include five mobile titles, with two already released and three in advanced stages. Mobile operations benefited from new scenarios and large‑scale collaborations, while the advertising arm reported 1.8× QoQ growth in page views and advertiser numbers across its media brands. Forecasts for the third quarter project net sales of ¥19.5 billion and operating income of ¥2.5 billion, assuming continued cost discipline and steady growth in paid services. The company’s geographic focus remains global, with releases across Japan, Australia, India, South Korea, and Taiwan. Methodologically, figures derive from consolidated financial statements, with headcount totaling 1,407 across game, advertising, and corporate functions.

GREE

Report

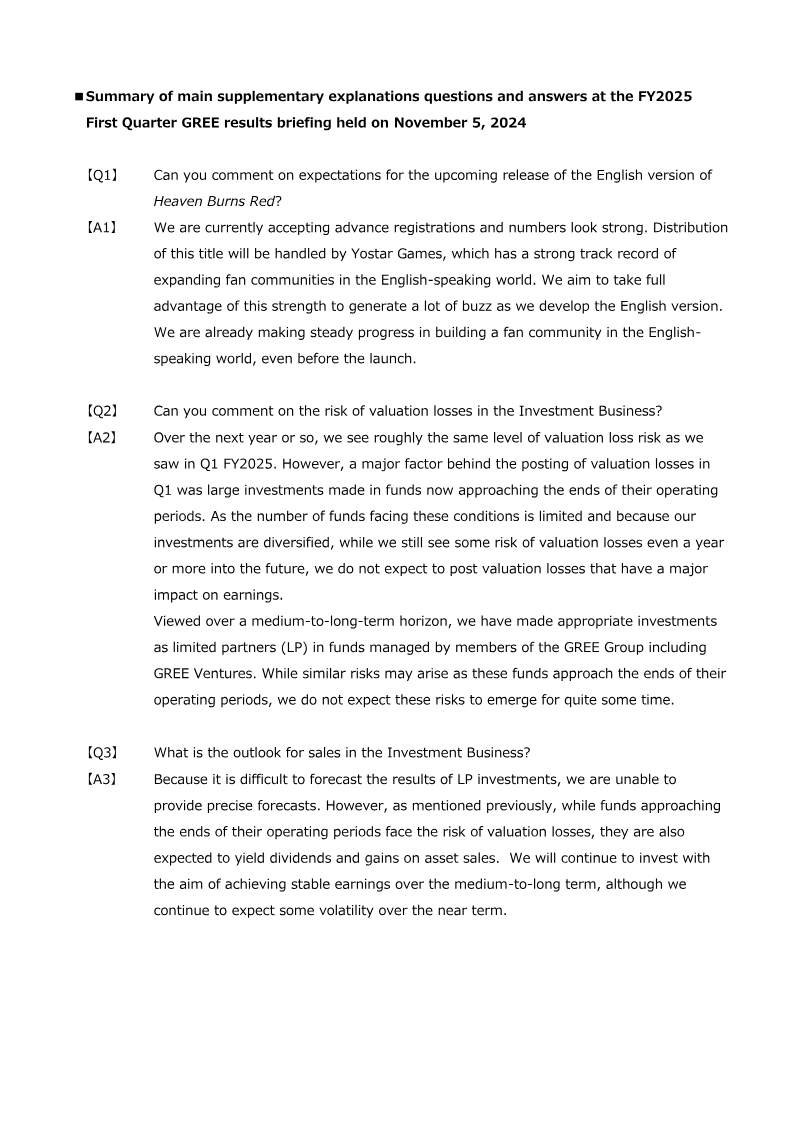

Summary of main supplementary explanations questions and answers at the FY2025 First Quarter GREE results briefing held on November 5, 2024 PDF

The briefing clarified GREE’s strategic focus for FY2025 first‑quarter results, emphasizing both gaming and investment operations. In the gaming segment, the company confirmed that advance registrations for the English version of “Heaven Burns Red” are strong and that distribution will be handled by Yostar Games, whose track record in expanding English‑speaking fan communities is expected to generate significant buzz. GREE highlighted ongoing community building efforts prior to launch, underscoring a proactive marketing approach. Regarding the investment business, management acknowledged that valuation‑loss risk remains comparable to Q1 FY2025 levels. The primary driver of past losses was large investments in funds nearing the end of their operating periods; however, diversification and limited exposure to such funds mitigate long‑term impact. GREE maintains that while short‑term volatility may persist, medium‑to‑long‑term earnings should remain stable as funds mature and yield dividends or asset sales. The company reiterated its commitment to investing in GREE‑Group managed funds, including GREE Ventures, and expects related risks to surface only after several years. Overall, the briefing presented a balanced outlook: aggressive growth in the gaming arm through strategic partnerships and community engagement, coupled with cautious yet steady investment practices aimed at preserving earnings stability amid inherent valuation risks.

GREE