Global

Report

Raport bieżący nr 11/2021Ujawnienie opóźnionej informacji poufnej o zawarciu przez PCF Group S.A. listu intencyjnego dotyczącego przejęcia zespołu deweloperskiego Phosphor Games, LLC

The report discloses that PCF Group S.A., a Warsaw‑based holding, entered into an intention letter on 31 March 2021 to acquire the development team of Phosphor Games, LLC, a Chicago‑based studio. The transaction is subject to an exclusive negotiation period until 30 April 2021 and involves a loan of USD 5 million to the group’s subsidiary People Can Fly U.S., LLC, with LIBOR plus 2 % interest over ten years. The loan is secured by the subsidiary’s intellectual property and is intended to fund the acquisition of Phosphor Games’ team. The report clarifies that signing the intention letter and initiating negotiations does not guarantee completion of the acquisition, noting potential risks to negotiation outcomes. The disclosure was delayed until 23 April 2021 in accordance with Article 17(4) of the EU Market Abuse Regulation (MAR). Management justified the delay by citing legal and commercial considerations: premature disclosure could jeopardise negotiation dynamics, affect transaction terms, or mislead the market. The report outlines that confidentiality was maintained through a controlled list of personnel with access to the information, updated per MAR requirements. Upon publication, PCF Group S.A. will notify the Polish Financial Supervision Authority of the delay and its compliance with MAR provisions. The scope covers a single acquisition transaction involving U.S. entities, with financial terms specified in USD and interest linked to LIBOR. The methodology is a regulatory compliance disclosure, referencing MAR articles and European Securities and Markets Authority guidance on delayed information release.

PCF Group

Report

1st Half Financial Results: FY 2011

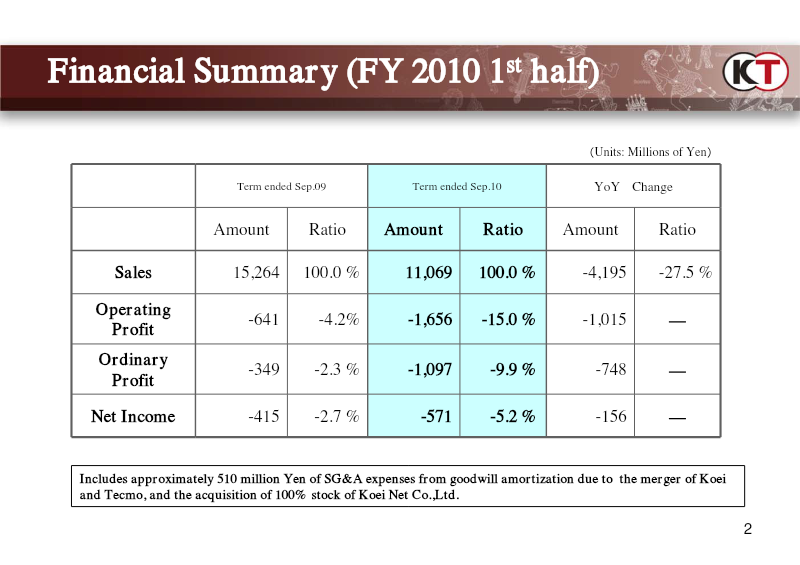

The first‑half financial results for the fiscal year ending March 2011 show a sharp decline in revenue and profitability compared with the same period in 2009. Net sales fell from ¥15,264 million to ¥11,069 million, a 27.5 % drop, while operating loss widened from ¥641 million to ¥1,656 million. Ordinary profit and net income also deteriorated, with ordinary loss increasing from ¥349 million to ¥1,097 million and net loss rising from ¥415 million to ¥571 million. The decline is largely attributed to a one‑time goodwill amortization expense of approximately ¥510 million incurred after the merger with Koei and acquisition of Koei Net Co., Ltd. The company’s operating segments reflected uneven performance: Game sales dropped by 16 % to ¥6,330 million, while Online and Media segments saw modest gains. Regional sales remained concentrated in Japan (85.5 %) with overseas sales accounting for 14.5 % of total revenue. The consolidated plan for FY 2010 projects a modest 0.0 % change in total sales to ¥34,500 million, with operating profit expected to rise from a loss of ¥641 million in FY 2009 to a gain of ¥4,000 million. Ordinary profit and net income are projected to improve by 13.0 % and 7.8 %, respectively, largely driven by a projected operating profit of ¥4,000 million in the Game segment. The plan also outlines significant capital expenditures (¥1,685 million) and a shift in marketing focus toward overseas markets and social gaming. Methodologically, the report relies on consolidated financial statements for the first half of FY 2010 and comparative figures from FY 2009, with adjustments noted for goodwill amortization. The document also includes strategic initiatives such as the launch of social games based on popular IPs, expansion into mobile and PC platforms, and the establishment of a Global Marketing Department to strengthen overseas presence.

Koei Tecmo