Dutch Games Monitor: Main Facts & Figures 2015

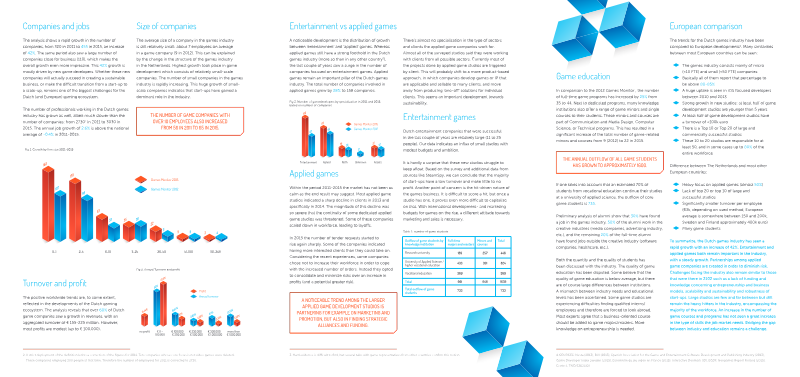

The Dutch games industry experienced significant expansion between 2011 and 2015, characterized by a 42% increase in the number of companies, which grew from 320 to 455. This growth was primarily driven by a surge in new, small-scale game development studios. Despite this rise in firm count, the industry remains dominated by micro-enterprises with an average of seven employees. While the total workforce expanded from 2,730 to 3,030 professionals, the rate of job creation was slower than the rate of company formation, reflecting the challenges start-ups face in scaling operations and achieving long-term sustainability.

The industry is bifurcated into entertainment and applied games, with the latter maintaining a particularly strong foothold in the Netherlands compared to other European nations. Applied game studios, which focus on training, education, and health, faced significant market volatility between 2013 and 2014, though demand for these services rebounded sharply by 2015. To mitigate risks associated with the hit-driven nature of the entertainment market and the project-based cycles of applied games, many studios are shifting toward product-based models and forming strategic alliances for marketing and funding.

Data for this analysis was gathered through a questionnaire sent to over 400 companies, with 130 responses, supplemented by industry roundtable discussions and existing databases. Financial performance remains modest, with most companies reporting annual profits under €100,000. While the number of game-related educational programs has increased by 25%, a persistent skills gap remains, as studios struggle to find employees with the necessary entrepreneurial and business acumen. Ultimately, while the Dutch ecosystem shows robust growth, the industry continues to grapple with the difficulty of transitioning from small start-ups to larger, commercially stable entities.

Dutch Games AssociationJan 2015