Live Ops

Report

FY2019 Fourth Quarter Financial Results Briefing

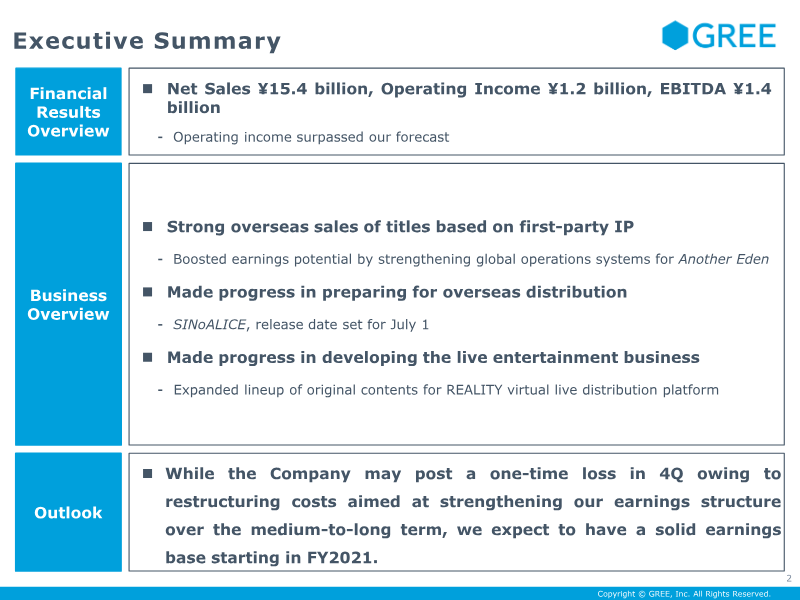

The briefing presents fiscal year 2019 results and outlines strategic priorities for FY20. Net sales reached ¥70.9 billion, operating income stood at ¥5.5 billion and EBITDA was ¥6.4 billion, with the fourth‑quarter figures of ¥17.4 billion in sales and ¥1.3 billion in operating income matching forecasts and remaining flat from the prior quarter. The company attributes performance to robust overseas distribution of existing titles, successful anniversary releases such as SINoALICE and Another Eden, and cost‑efficiency initiatives that lifted organic profit by ¥250 million. Geographically, the firm expanded into key Asian markets—including Hong Kong, Taiwan, and China—while launching titles in North America and Europe. Distribution strategy emphasizes self‑distribution on platforms like Nintendo Switch, LINE, and Facebook Games to enhance profitability. The live entertainment pillar introduced the VTuber platform “REALITY,” adding avatar functions and official programs, while advertising and media efforts focused on vertical media expansion. FY20 plans center on aggressive investment in three pillars: game development (engine, IP, global strategy), live entertainment (REALITY platform enhancements and new VTuber production), and advertising/media (vertical media growth). The company aims to launch two new titles in FY20, with a pipeline of four to six projects for FY21 and beyond. Dividend policy will target a 2 % payout ratio, with a ¥10 dividend proposed for the current year. The overall outlook remains positive, emphasizing stable earnings from existing titles and growth potential from new IPs and overseas markets.

GREE

Report

Summary of Main Questions and Answers at the FY2019 Fourth Quarter GREE Results Briefing

The briefing focused on FY2019 fourth‑quarter performance, highlighting that revenue remained solid largely due to anniversary events for flagship titles. Despite a year‑over‑year drop in coin consumption during the third and fourth quarters, the company noted that 4Q FY2019 anniversary events were more effective than those in 4Q FY2018, aided by the launch of new titles such as *In Love with NEWS* and the North American release of *DanMachi*. Looking ahead to Q1 FY2020, management projected a reactive decline in operating income because of the waning impact of those anniversary events. Forecasted operating income was expected to fall between ¥0.5 billion and just under ¥1.0 billion, with plans to introduce new titles from Q2 onward. The company also emphasized its newly developed simultaneous release system, enabling coordinated launches in Japan and overseas based on each title’s characteristics. Regarding resource allocation, the company confirmed it would continue to develop new titles while maintaining a substantial workforce on existing games, preserving its current balance. The briefing explained that the roughly 40% year‑over‑year decline in operating income was largely attributable to a downturn in browser game revenue, which constitutes over 90% of the company’s overall income. The discussion underscored that while segment‑level details were not disclosed, the decline in browser game earnings was the primary driver behind the overall income contraction.

GREE