Skip to main content

Game Industry

Library

Library

Search

Ask AI

News

Connect your AI

Browse

The Catch Up

Topics

Collections

Writers

Help

Subscribe

Game Industry

Library

Library

Search

Ask AI

Saved

Library

34 reports matching your filters

All Types

Reports

Articles

Presentations

Whitepapers

Financial

Legal

Other

Search

Salary

Employment

Market Analysis

Global

Diversity & Inclusion

Europe

North America

USA

Game Development

UK

Player Demographics

Investment

Market Forecast

Asia

Japan

Streaming

Finland

Serbia

Clear

Filters

1

Salary

Recently added

Newest first

Oldest first

Title A–Z

Title Z–A

Report

36 pages

State of the Game Development Industry 2023: Workplace Health & HR Culture, Mental Trends

The game industry experienced significant instability in 2023, with 28% of the workforce affected by layoffs and an Employee Net Promoter Score of -19% indicating widespread dissatisfaction.

Economic recalibration and management failures are the primary drivers of industry distress, while AI automation currently accounts for only 3% of total job losses.

Workplace culture is suffering from 'quiet hiring' practices, where 37% of employees are absorbing expanded responsibilities without corresponding increases in compensation.

Employment

Salary

Diversity & Inclusion

+1

80 Level

Jan 2023

Report

61 pages

2023 Games & Interactive Salary & Satisfaction Survey

Salary has overtaken flexible work as the primary driver for career moves, with 31% of UK and Western European respondents citing higher pay as their main reason for leaving a position.

Artist compensation has seen a sharp 35% increase between 2021 and 2023, with mid-level artists now earning approximately £75k.

Project close-out periods are a critical retention risk, as 22% of UK respondents decline new offers to finish current projects and 46% of global staff are actively job hunting.

Salary

Employment

Global

Skillsearch

Jan 2023

Report

3 pages

UK Games Jobs Summary: November 2022

UK games industry recruitment contracted significantly in November 2022, resulting in over 500 fewer open vacancies compared to June 2022.

Mobile studios experienced the highest proportional reduction in job postings, largely driven by the completion or cancellation of roles following corporate mergers.

Despite the broader market decline, the industry added over 600 new job postings during the month, and the total number of tracked studios grew by eight companies.

Employment

Market Analysis

Salary

+1

Games Jobs Live

Nov 2022

Report

3 pages

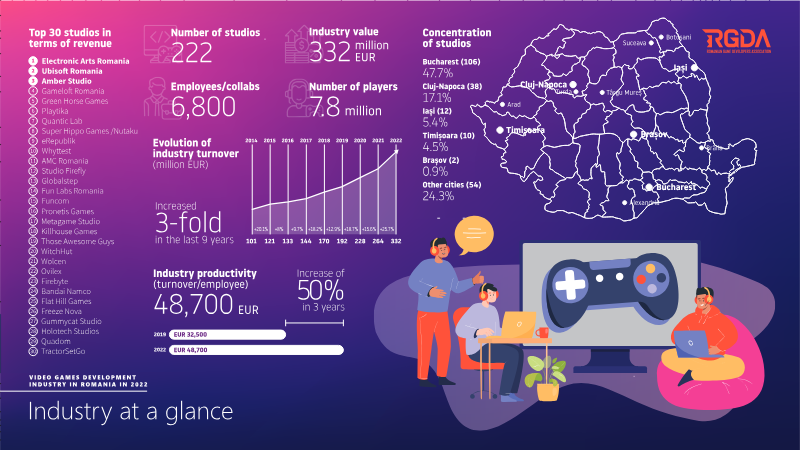

Video Games Development Industry in Romania – 2022 (Summary & Key Insights)

The Romanian video game industry generated between €222 million and €332 million in 2022, driven by a highly export-oriented model where over 70% of revenue comes from foreign markets.

Market concentration is high, with the top three players—Electronic Arts Romania, Ubisoft Romania, and Amber Studio—accounting for approximately 47% of total industry revenue.

Electronic Arts Romania is the largest single entity in the sector, reporting €106 million in revenue, followed by Ubisoft Romania and Amber Studio, which represent significant market shares of 47.7% and 38% respectively.

Market Analysis

Employment

Salary

+1

RGDA – Romanian Game Developers Association

Jan 2022

Report

17 pages

Annual Barometer of the Video Game Industry in France 2021

France is the second most attractive country globally for video game development, supported by a strong reliance on national tax credits and regional funding utilized by 41% of companies.

The industry is highly productive with approximately 1,350 games in development during 2021, 92% of which are original intellectual properties.

Despite high levels of optimism regarding the market, 36.5% of studios reported a financial deficit in 2020, marking the highest rate of insolvency since 2014.

Market Analysis

Salary

Employment

+1

Syndicat National du Jeu Vidéo

Jan 2021

Report

38 pages

Romanian Game Development Industry Report: 2020

The Romanian game development industry generated €218.5 million in revenue in 2020, marking a 19.1% year-on-year growth rate.

The broader IT sector, bolstered by state-aid schemes and tax exemptions, employed over 113,000 people and contributed approximately 6.8% of Romania's GDP in 2020.

Major AAA support studios including EA Romania, Ubisoft, and Gameloft employ roughly 750 developers in the country, contributing to global franchises like FIFA and Assassin’s Creed.

Market Analysis

Employment

Salary

+1

RGDA – Romanian Game Developers Association

Jan 2021

Whitepaper

2 pages

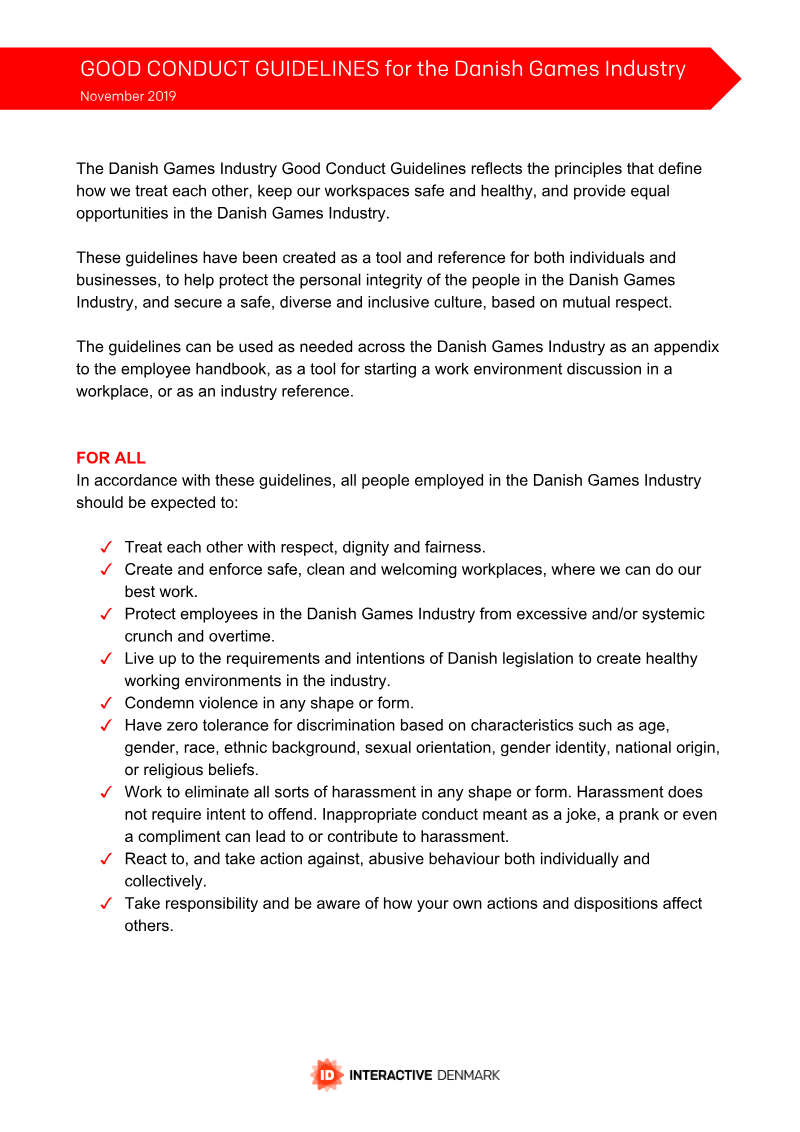

Good Conduct Guidelines for the Danish Games Industry

The Good Conduct Guidelines, published in November 2019, establish a standardized framework for professional behavior and workplace safety across the Danish game development sector.

The policy mandates the elimination of systemic crunch and excessive overtime to ensure a sustainable working environment for all industry staff.

Harassment is defined by its objective impact on the victim rather than the intent of the perpetrator, and the industry maintains a zero-tolerance stance toward all forms of abusive behavior.

Diversity & Inclusion

Employment

Salary

Danish Games Industry

Nov 2019

Report

41 pages

Romanian Game Development Industry Report 2019

The Romanian game development industry generated $188.5 million in 2018, representing a 19.2% year-over-year growth.

The sector employs over 6,000 professionals across approximately 103 active entities, primarily concentrated in Bucharest, Cluj-Napoca, and Timișoara.

77% of industry firms focus exclusively on game development, while the remainder provide ancillary services like quality assurance, testing, and publishing for international clients.

Market Analysis

Europe

Salary

RGDA – Romanian Game Developers Association

Jan 2019

Report

46 pages

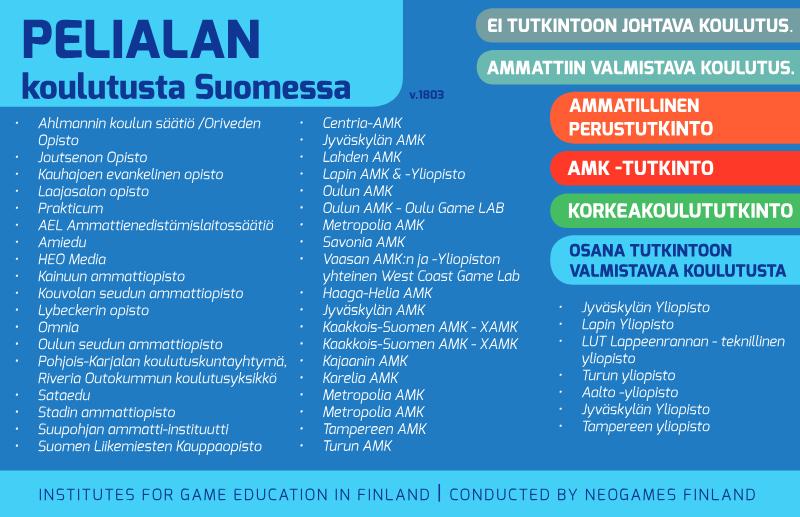

Koulutusta Suomessa

The Finnish educational landscape includes a diverse range of institutions such as Ahlmannin koulun säätiö, Oriveden Opisto, and Joutsenon Opisto.

Vocational and specialized training providers listed include AEL Ammattienedistämislaitossäätiö, Amiedu, and Kouvolan seudun ammattiopisto.

Media-focused education is represented by institutions such as HEO Media and Laajasalon opisto.

Employment

Salary

Finland

+1

Neogames Finland

Jan 2018

Report

51 pages

The Games Monitor 2018

The Games Monitor 2018 provides an updated analysis of the Dutch games industry, following previous research editions published in 2012 and 2015.

Market Analysis

Employment

Europe

+1

Dutch Games Association

Jan 2018

Report

36 pages

Dutch Games Monitor: The Netherlands 2015

The Dutch Games Monitor was first established in 2012 to provide comprehensive industry data through extensive surveys and interviews.

The 2012 edition served as the inaugural research project to offer a broad, structured insight into the state of the Dutch games industry.

Interest in data regarding the games industry has significantly increased in the years following the 2012 report.

Market Analysis

Employment

Europe

+1

Dutch Games Association

Jan 2015

Report

16 pages

Essential Facts 2014: Canada

Canada’s video game sector directly employs 16,500 people, representing 27,000 full-time equivalent jobs.

The industry contributed $2.3 billion to Canada’s GDP and generated $1.6 billion in direct spending, marking a 12.5% increase since 2011.

Employment in the sector grew by 5% between 2011 and 2013, with 40% of firms projecting a 25% staff expansion within two years.

Market Analysis

Player Demographics

Salary

+1

ESAC – Entertainment Software Association of Canada

Jan 2014

Report

60 pages

Canada's Video Game Industry in 2013: Final Report

Canadian video-game firms rate tax credits as highly effective, awarding them an average satisfaction score of 4.4/5.

The tax-credit regime is a primary driver of industry expansion, with 40% of firms projecting revenue growth exceeding 25% in the coming year.

Tax incentives are most effective at creating project opportunities, which received an impact score of 4.0/5, followed by strong benefits for employee retention and industry visibility.

Market Analysis

Employment

Salary

+1

ESAC – Entertainment Software Association of Canada

Jul 2013

Report

19 pages

Faits Essentiels 2011 sur le Secteur Canadien des Jeux Vidéo et Informatiques

Canada’s video game industry generated C$1.7 billion in direct economic impact in 2011, ranking third globally in revenue and first in jobs per capita.

The sector employed approximately 16,000 workers across 350 firms, with an 11% growth rate over the previous two years and a projected 17% increase for the following two.

Quebec serves as the industry hub with 8,236 employees and C$733 million in spending, while Ontario exhibits the fastest growth trajectory at 20–21%.

Market Analysis

Salary

Player Demographics

+1

ESAC – Entertainment Software Association of Canada

Jan 2011

Previous

1

2

Next