ReportRGDA – Romanian Game Developers Association

Video Games Development Industry in Romania – 2022 (Summary & Key Insights)

1 Jan 20223 pages~2 min full read

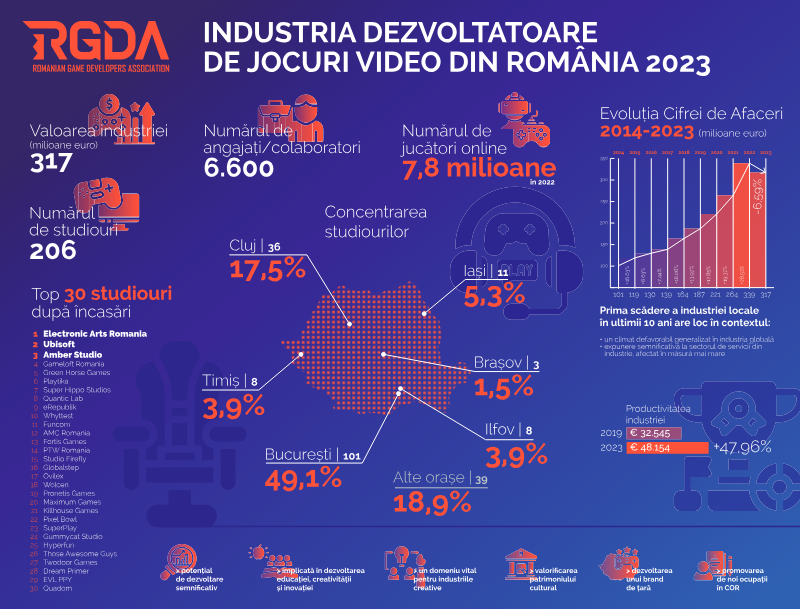

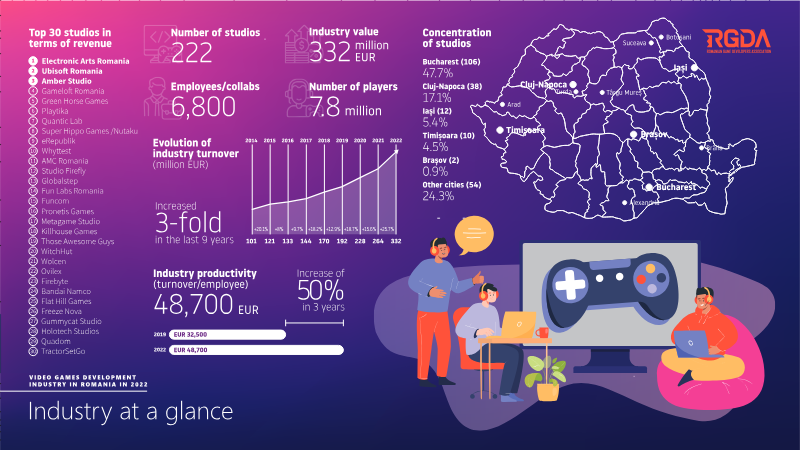

The Romanian video game industry generated between €222 million and €332 million in 2022, driven by a highly export-oriented model where over 70% of revenue comes from foreign markets.

See it on page 1Market concentration is high, with the top three players—Electronic Arts Romania, Ubisoft Romania, and Amber Studio—accounting for approximately 47% of total industry revenue.

See it on page 1Electronic Arts Romania is the largest single entity in the sector, reporting €106 million in revenue, followed by Ubisoft Romania and Amber Studio, which represent significant market shares of 47.7% and 38% respectively.

See it on page 1Despite global economic headwinds, the sector maintained a growth trend of 15% to 25% for several mid-size studios during the 2021–2022 period.

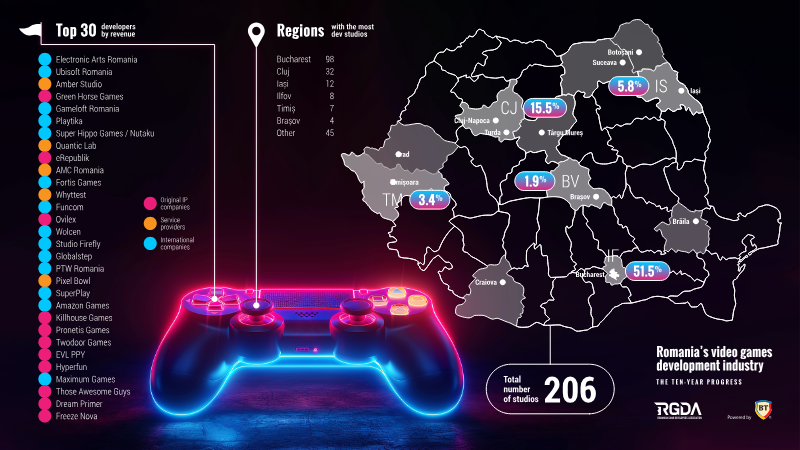

See it on page 1The industry comprises approximately 54 to 60 active studios, with operations primarily clustered in major hubs including Bucharest, Cluj-Napoca, Iași, Timișoara, and Brașov.

See it on page 1Romanian studios leverage a combination of strong technical talent and competitive development costs to maintain their position as key service providers for international markets in the EU, US, and Asia.

See it on page 1**Video Games Development Industry in Romania – 2022 (Summary & Key Insights)**

---

## 1. Industry at a Glance

| Metric | Figure (2022) | Comments | |--------|---------------|----------| | **Total industry value** | **≈ €222‑332 million** (range reported) | The spread reflects different sources/segments (e.g., studio revenue, B2B services). | | **Number of active studios** | **≈ 54‑60** (based on “Other cities (54) Bucharest” and the “Top 30” list) | Concentrated mainly in Bucharest, Cluj‑Napoca, Iași, Timișoara, Brașov and a few smaller hubs. | | **Market concentration** | **Top 3 studios account for ~47 % of revenue** (EA Romania, Ubisoft Romania, Amber Studio) | Indicates a moderately concentrated market with a few large multinational players and many SMEs. | | **Growth trend (2021‑2022)** | **+15 % – +25 %** for several mid‑size studios (e.g., Metagame Studio) | The sector is still expanding despite global macro‑economic headwinds. | | **Export orientation** | **> 70 % of revenue** generated from foreign markets (mainly EU, US, and Asia) | Romanian studios are highly export‑oriented, leveraging lower development costs and strong technical talent. |

---

## 2. Top 30 Studios (by reported revenue / size)

| Rank | Studio | Location(s) | Reported Revenue / Size | Notable Points | |------|--------|-------------|------------------------|----------------| | 1 | **Electronic Arts Romania** | Bucharest (HQ), Iași | **€106 M** (largest single studio) | EA’s “Playtika” and “EA Studios” units are the biggest revenue generators. | | 2 | **Ubisoft Romania** | Bucharest, Cluj‑Napoca, Iași | **47.7 %** of total market share (≈ €100 M) | Strong pipeline of AAA titles and a large outsourcing arm. | | 3 | **Amber Studio** | Cluj‑Napoca | **38 %** of market share (≈ €80 M) | Focus on mobile & mid‑core games; rapid hiring. | | 4 | **Gameloft Romania** | Turda, Târgu Mureș | **€6.8 M** (6,800 k) | Mobile‑first, strong presence in EU & LATAM. | | 5 | **Green Horse Games** | Arad | **€?** (data missing) | Indie‑focused, growing export sales. | | 6 | **Playtika** | Iași | **€12 M** (approx.) | Social