Market Analysis

Report

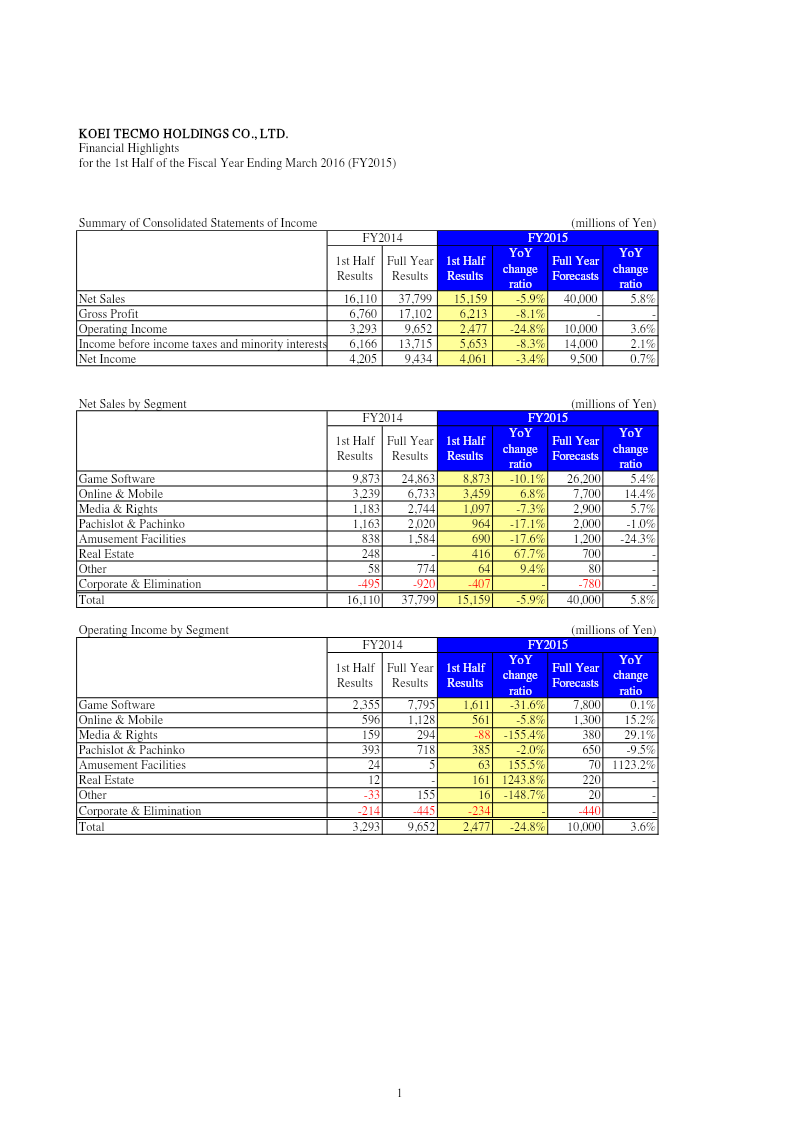

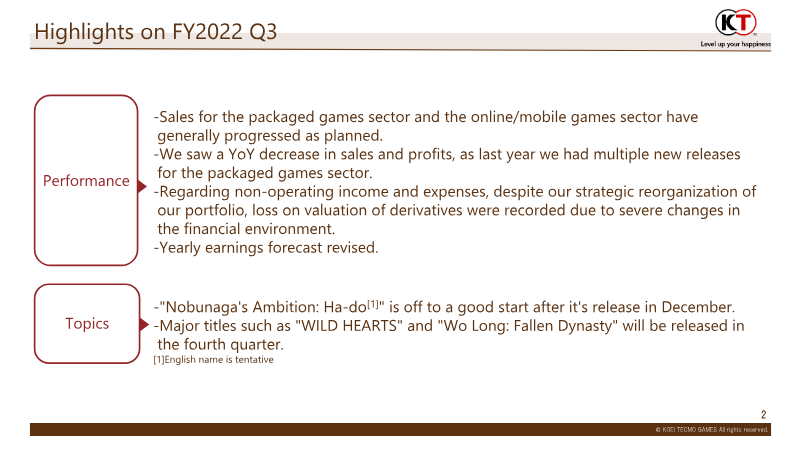

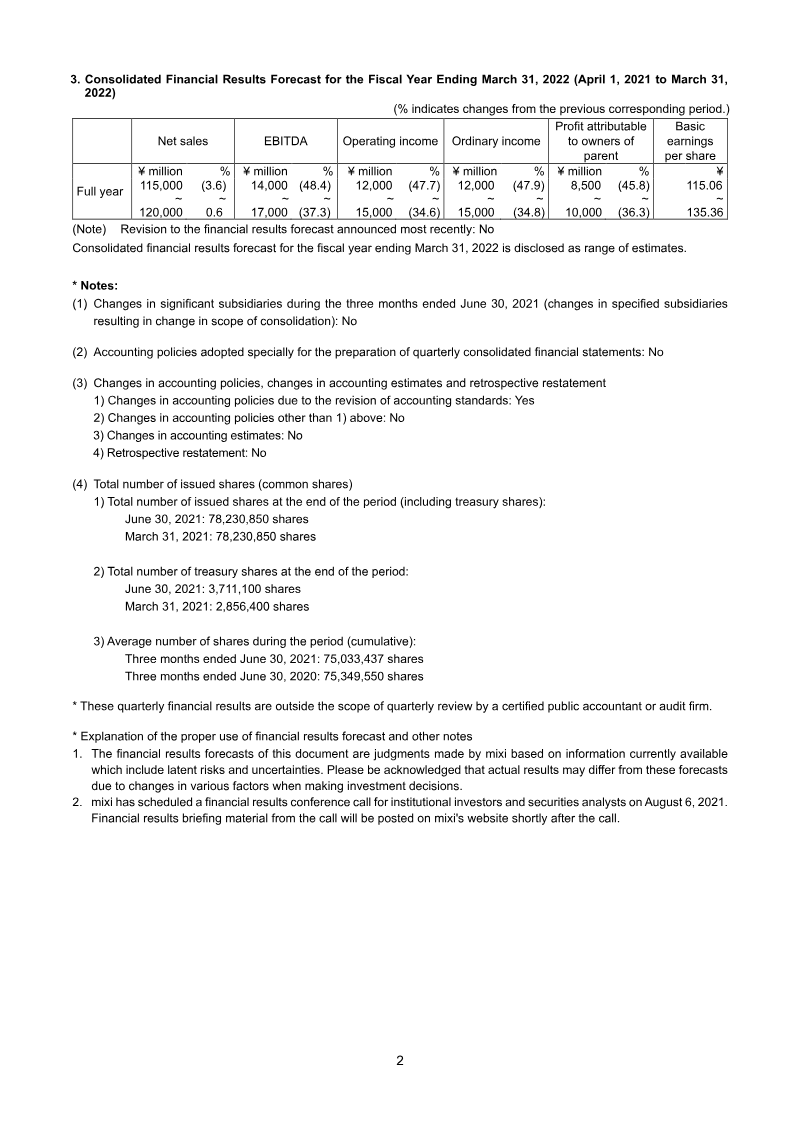

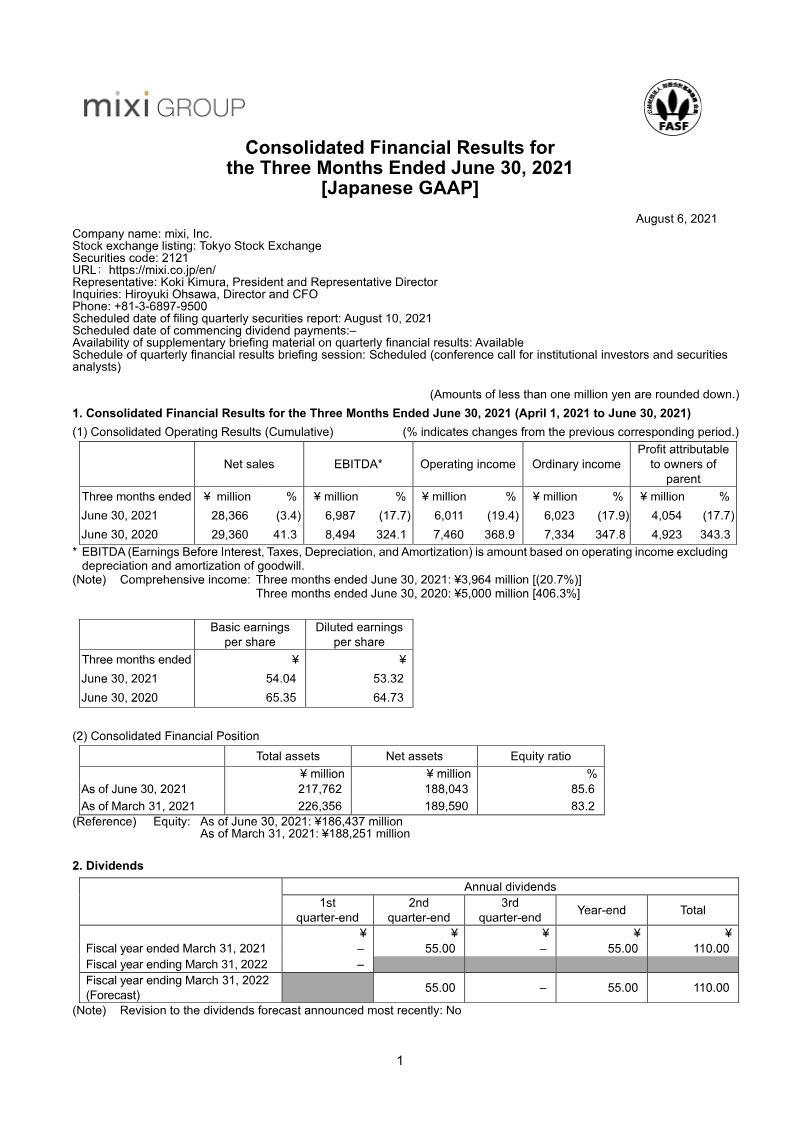

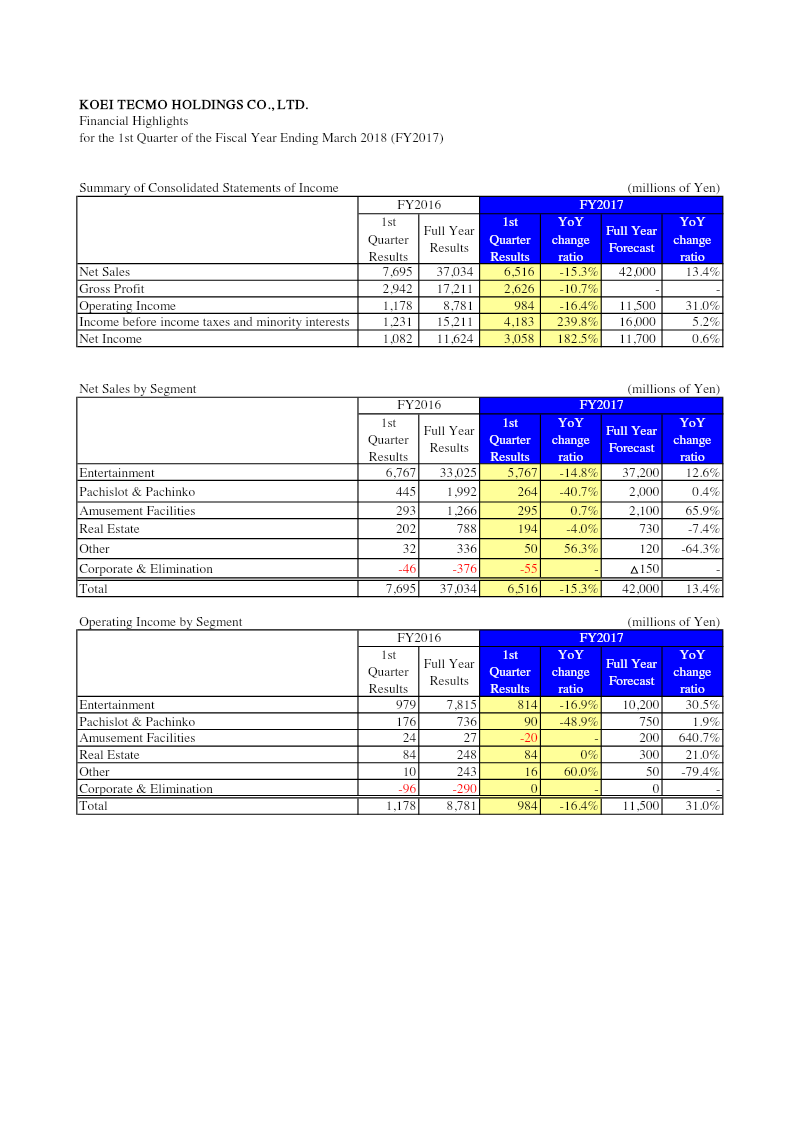

Financial Highlights: 1st Quarter of Fiscal Year Ending March 2018

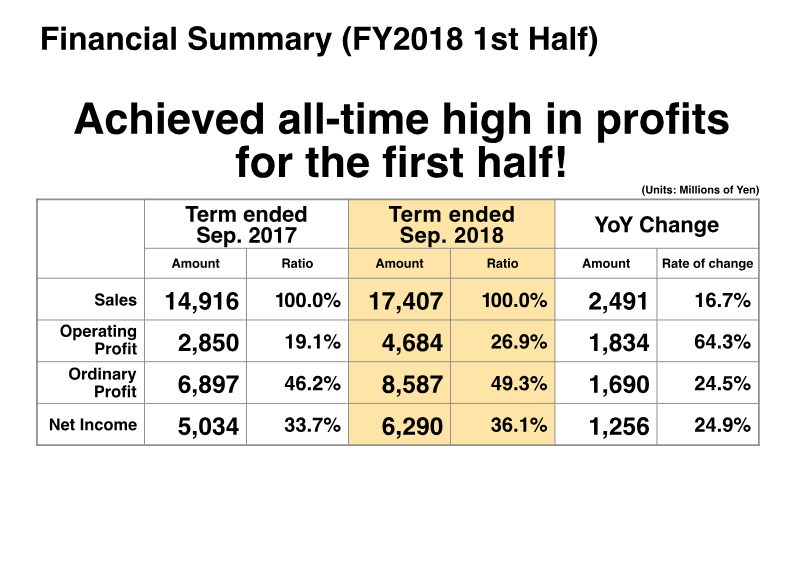

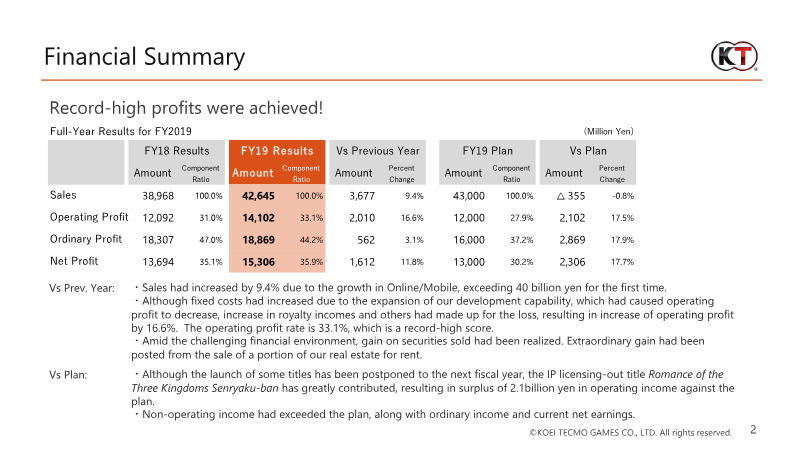

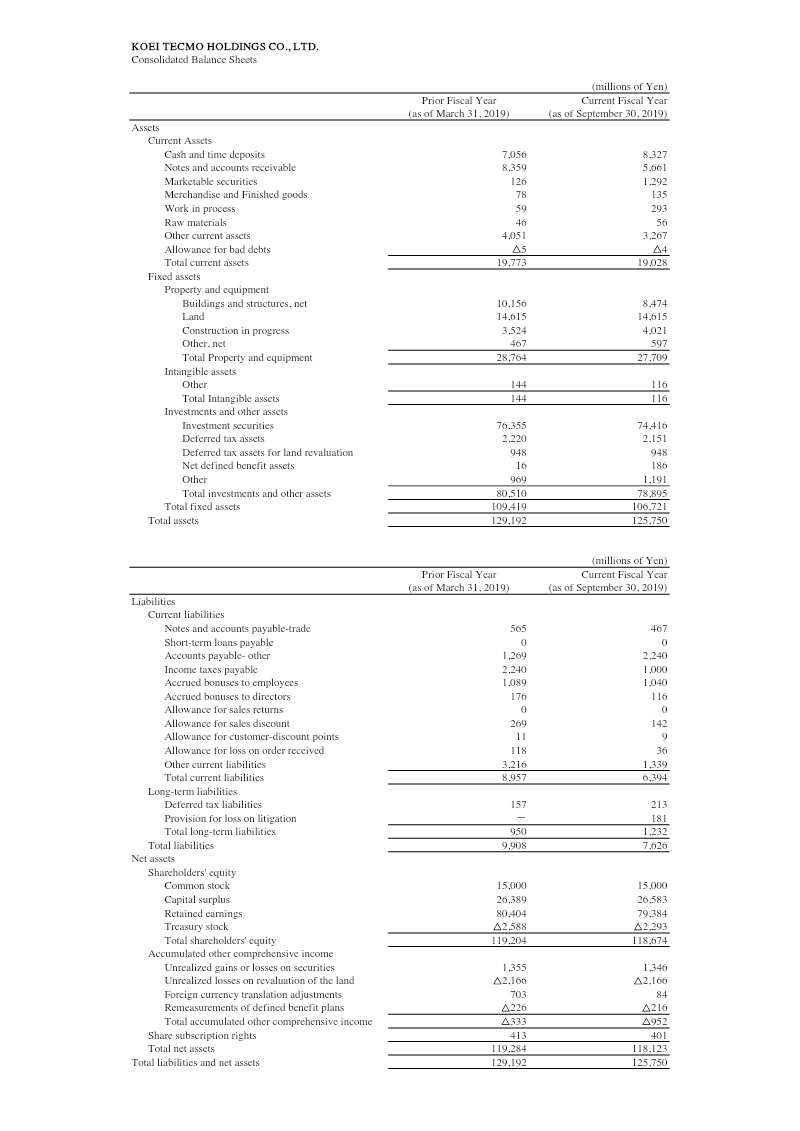

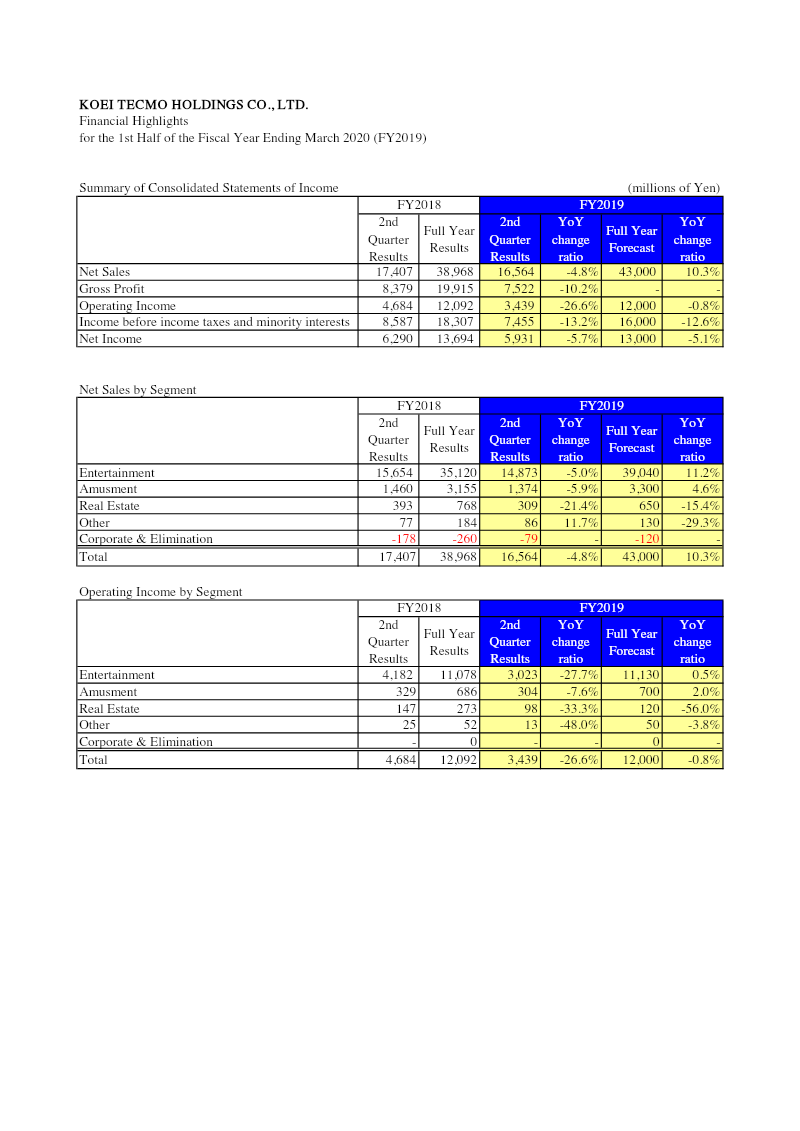

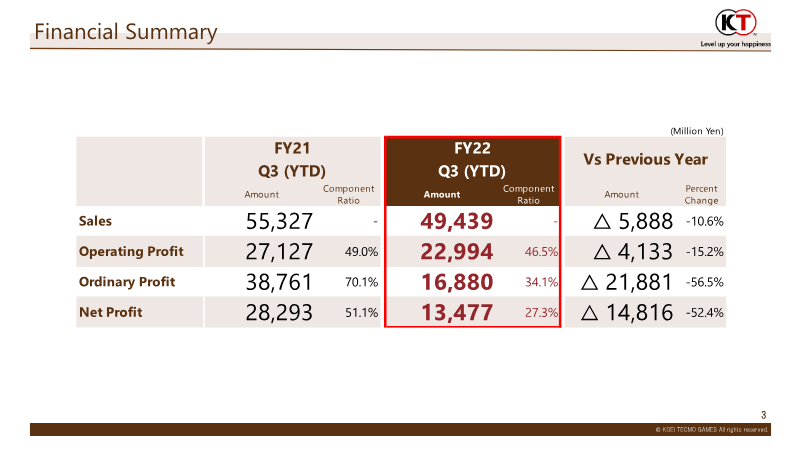

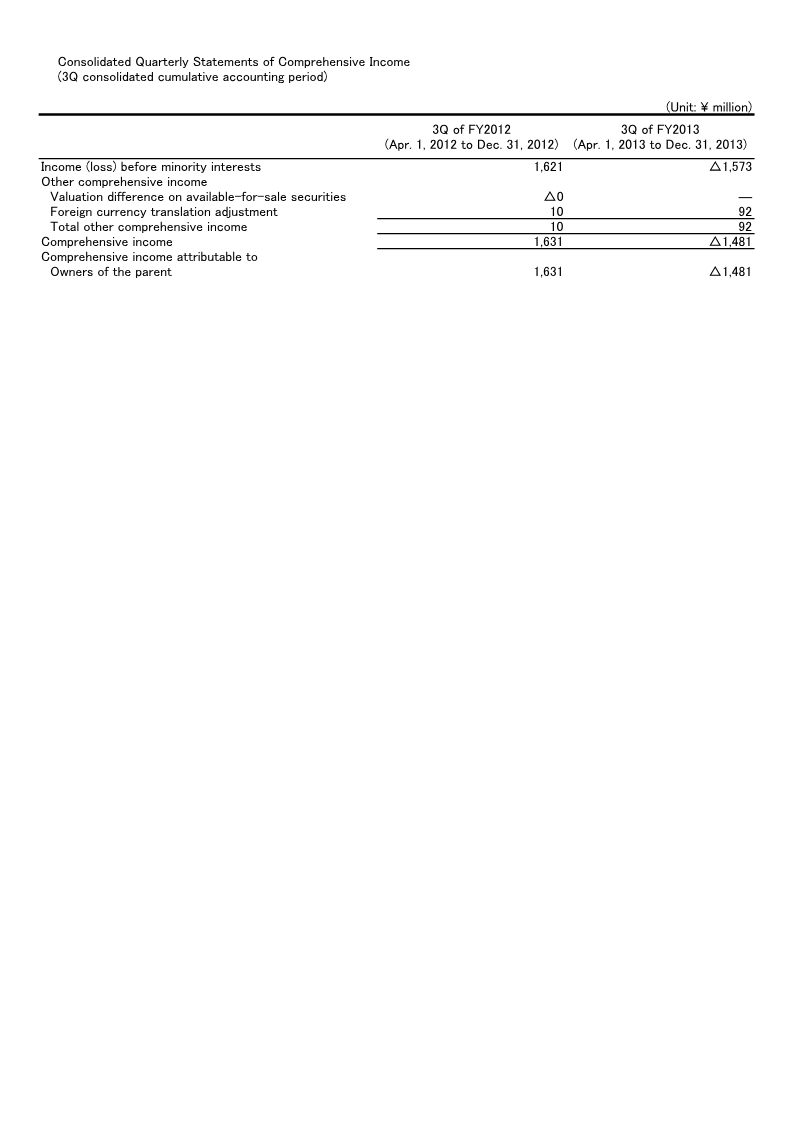

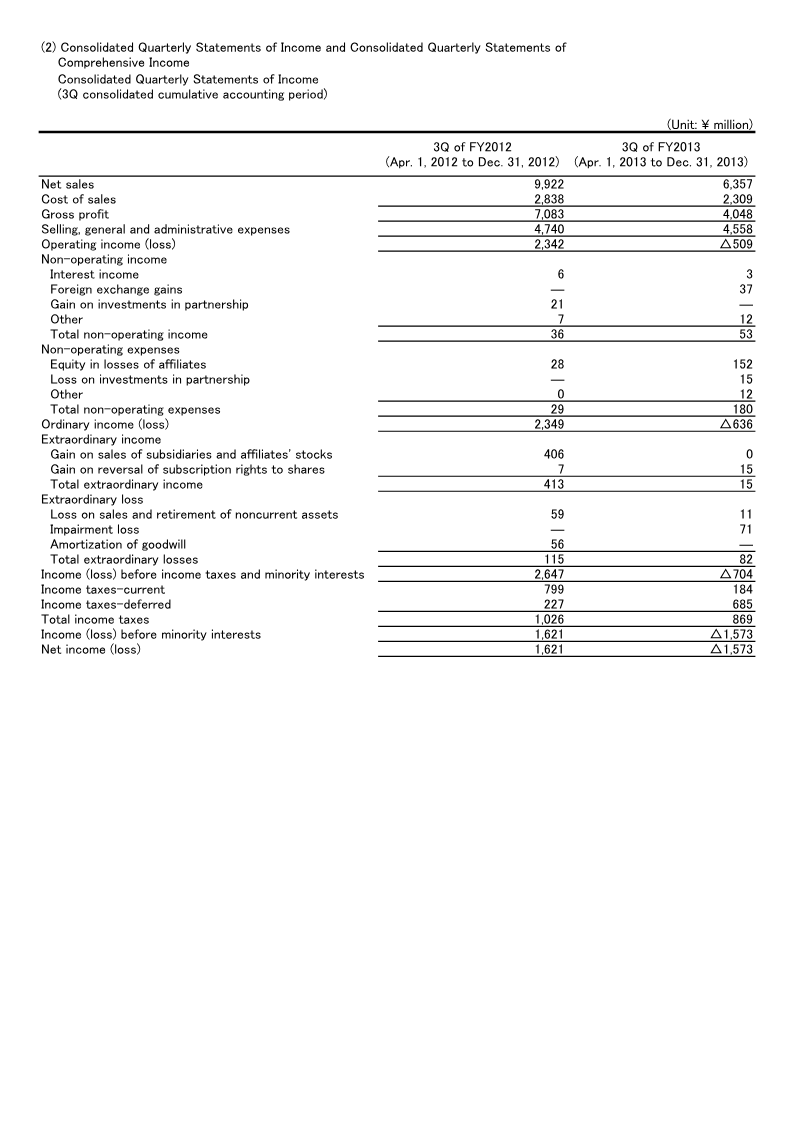

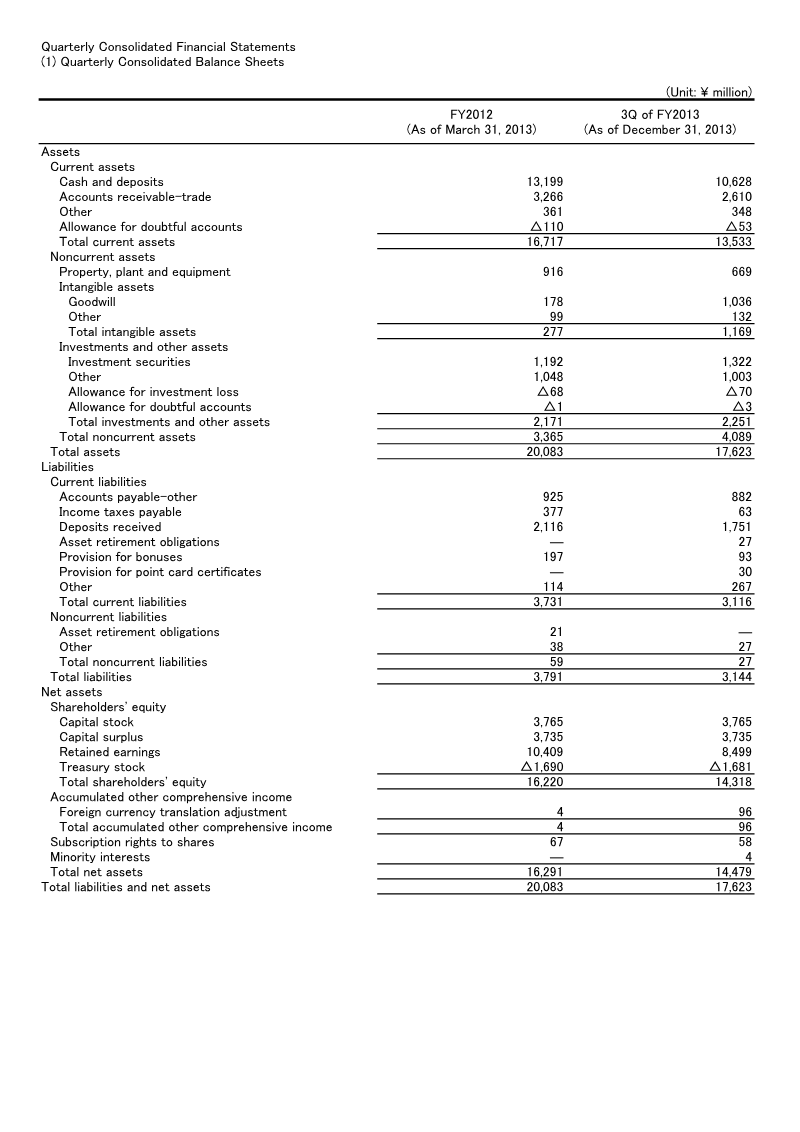

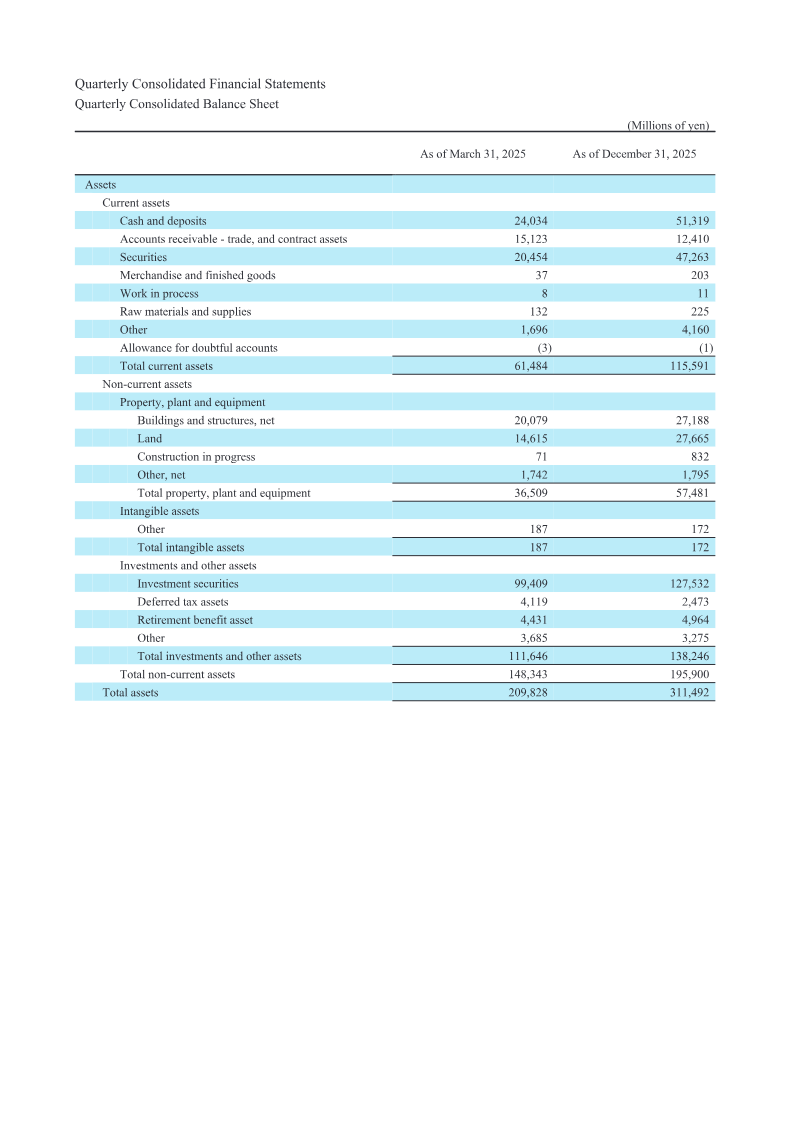

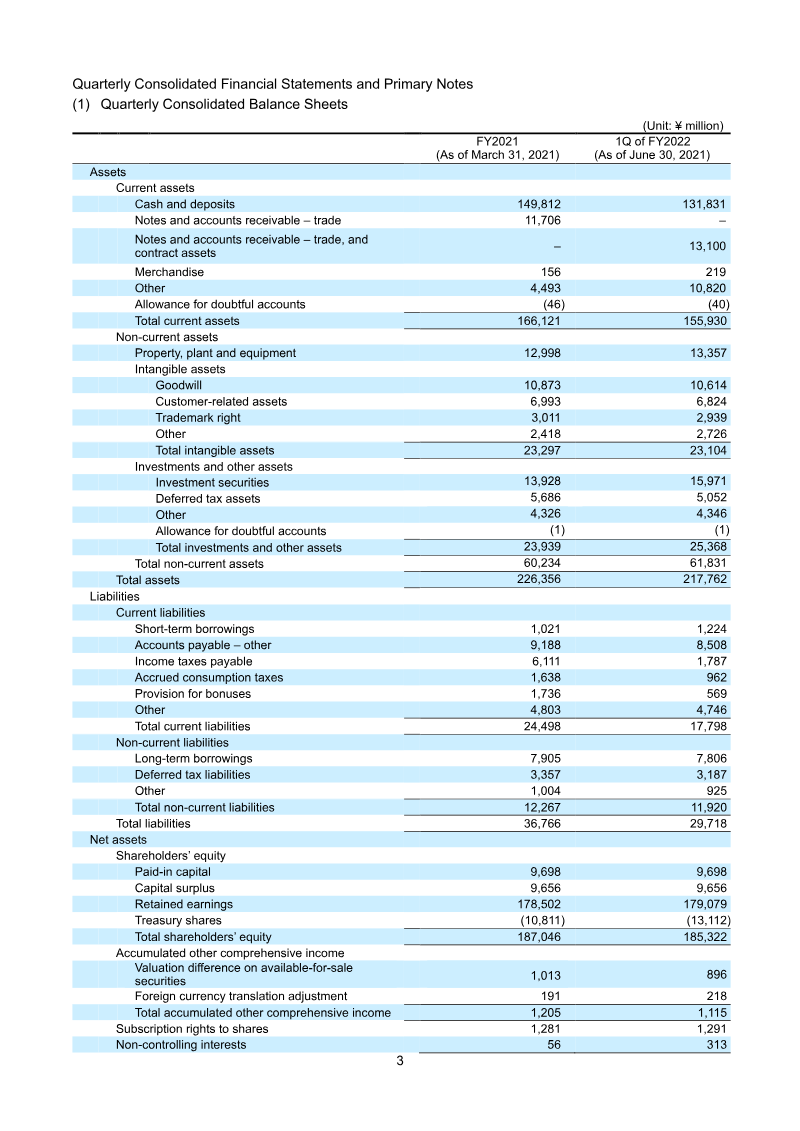

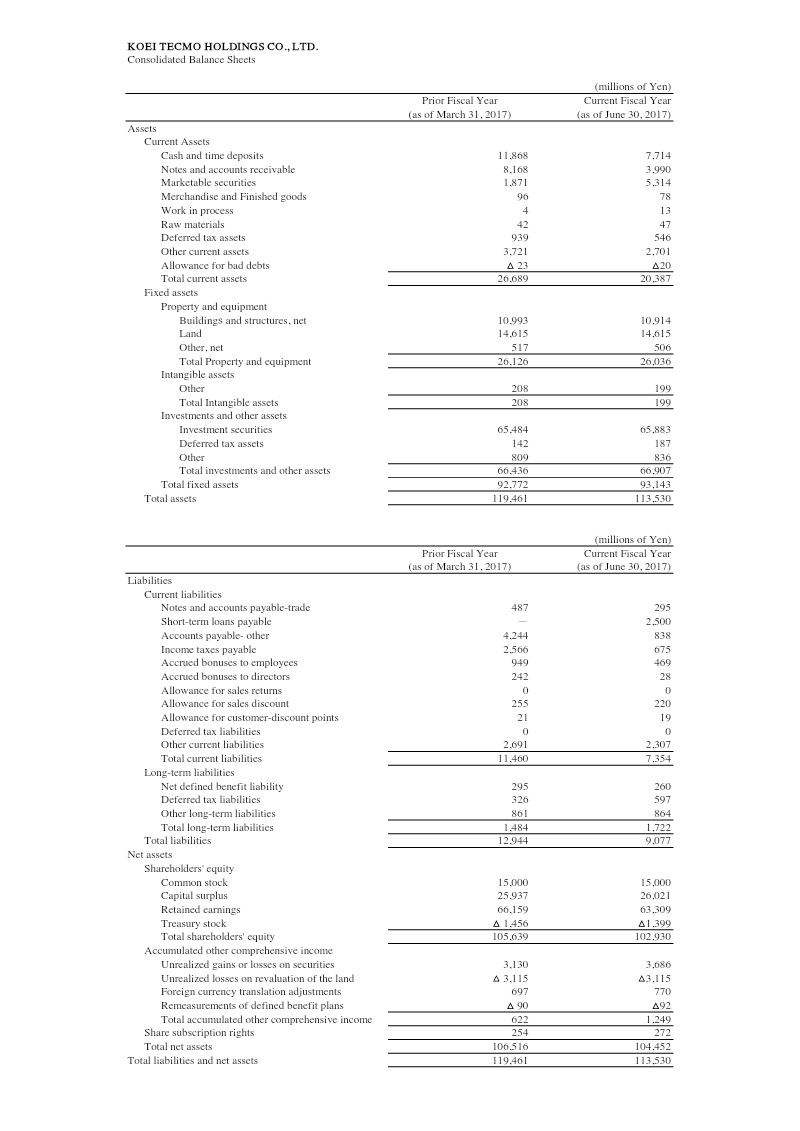

Financial highlights for KOEI TECMO HOLDINGS CO., LTD. cover the first quarter of fiscal year ending March 2018, comparing results to FY2017 and a forecast for the full year. Net sales fell 15.3 % to ¥37,034 million, driven by a 14.8 % decline in the entertainment segment and a 40.7 % drop in pachislot & pachinko revenue, while amusement facilities grew modestly by 0.7 %. Gross profit decreased 10.7 % to ¥17,211 million, and operating income contracted 16.4 % to ¥8,781 million; however, income before taxes surged 239.8 % to ¥15,211 million due largely to a sharp rise in operating income from the entertainment segment. Net income increased 182.5 % to ¥11,624 million, reflecting higher profitability in core gaming operations. Segment‑level operating income mirrored sales trends: entertainment contributed ¥7,815 million (−16.9 % YoY), pachislot & pachinko ¥736 million (−48.9 % YoY), and amusement facilities ¥27 million (−20 %). Forecasts for the full year project net sales of ¥42,000 million (+13.4 % YoY) and operating income of ¥11,500 million (+31.0 % YoY), indicating a recovery trajectory. Balance‑sheet data as of June 30, 2017 show total assets at ¥113,530 million and liabilities at ¥9,077 million, with shareholders’ equity of ¥104,452 million. Current assets declined from ¥26,689 million to ¥20,387 million, largely due to reduced cash and time deposits. Current liabilities fell from ¥11,460 million to ¥7,354 million, driven by lower trade payables and short‑term loans. The company’s liquidity position remains solid, with a current ratio above 2:1 and a debt‑to‑equity ratio below 0.09, supporting continued investment in gaming and entertainment assets across Japan during the fiscal year.

Koei Tecmo

Whitepaper

Evolution of Entertainment Whitepaper

The entertainment landscape is undergoing a significant transformation as consumer engagement shifts toward interactive media, particularly video games, which now compete directly with traditional formats like film and television for leisure time. In the United States, the average consumer aged 2 and older spends approximately 16.5 hours per week on gaming activities, a figure that rivals the time spent on social media and music streaming. This trend is most pronounced among younger demographics, specifically Gen Z and Millennials, who increasingly view gaming not just as a solitary hobby but as a primary social platform for community building and self-expression. Data indicates that 73 percent of the U.S. population plays video games, reflecting a broad market penetration that spans all age groups and socioeconomic backgrounds. While mobile gaming remains the most accessible entry point due to high smartphone ownership, console and PC gaming continue to drive the highest levels of deep engagement and monetization. The rise of subscription services and free-to-play models has further lowered barriers to entry, allowing for a continuous influx of new users while stabilizing revenue through recurring transactions rather than one-time purchases. The convergence of media formats is a defining characteristic of the current era, as intellectual properties increasingly transition between games, streaming series, and live events. This cross-platform synergy extends the lifecycle of content and deepens brand loyalty. As technological infrastructure improves, particularly with the expansion of high-speed internet and cloud gaming capabilities, the distinction between different forms of digital entertainment will continue to blur. Success in this evolving market requires stakeholders to prioritize community-driven experiences and multi-platform accessibility to capture the attention of a fragmented audience.

International Game Developers’ Association