Investment

Report

Gaming Industry Report: Q1 2023

The report presents a comprehensive snapshot of the global gaming industry for Q1 2023, emphasizing market growth, investment dynamics, and strategic shifts across regions. Global revenue reached $201 billion in 2023, up 9% YoY from a $184 billion base in 2022, with public markets showing a 10–20% rise year‑to‑date. Venture capital activity rebounded to pre‑2021 levels, with $761 million invested across 109 North American rounds in Q1 2023; early‑stage deals remain robust while late‑stage activity has slowed. AI investment, though not new to gaming, surged in 2021 and continues to focus on asset generation and conversational AI. Regulatory developments include the finalization of major M&A deals (e.g., Microsoft–Activision Blizzard) and a pending TikTok ban that could impact gaming advertising spend. Key strategic moves feature Epic Games’ launch of self‑publishing tools on its Epic Games Store, offering a 12% fee versus Steam’s 30%, and the integration of user‑generated content into Fortnite with a 40% revenue share for creators. Google’s pivot from Stadia to cloud‑based gaming infrastructure underscores a broader industry shift toward scalable, data‑driven services. Roblox’s demographic expansion has driven a 22% YoY increase in daily active users, reflecting successful monetization of older players. Geographically, Asia dominates venture funding (over $1.8 billion in Q1 2023), followed by North America ($1.9 billion) and Europe ($473 million). Emerging markets such as Africa, South America, and Australia show nascent but growing activity. Public gaming companies hold $48 billion in cash, supporting a healthy M&A environment. The report concludes with a list of major industry events and highlights Konvoy’s investment focus on frontier gaming platforms and technologies.

KonvoyJan 2023

Financial

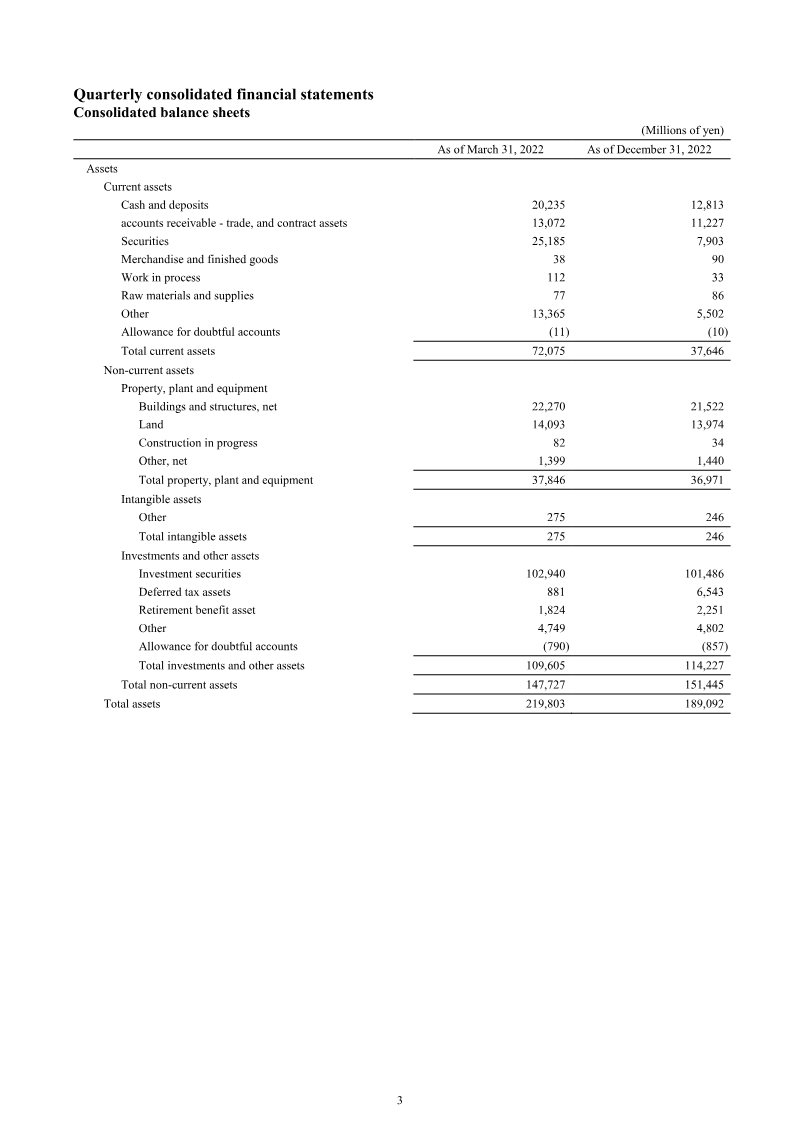

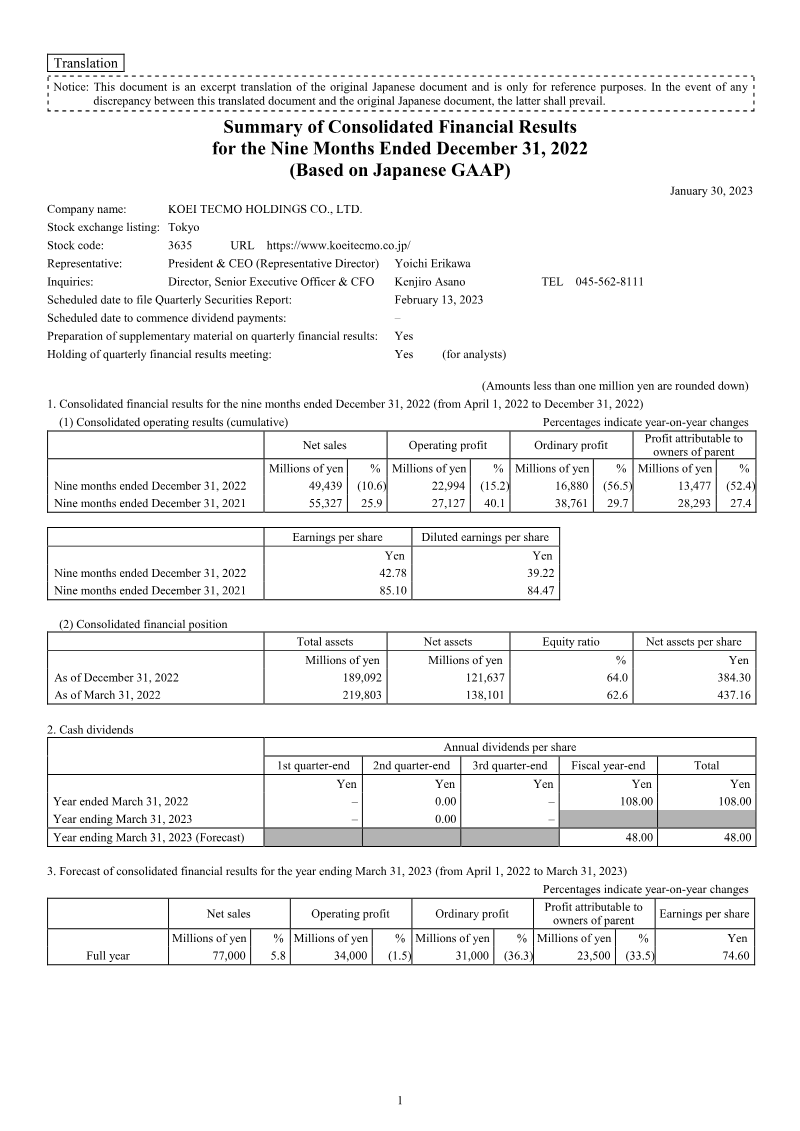

Financial Results for the Third Quarter of the Fiscal Year Ending March 2023

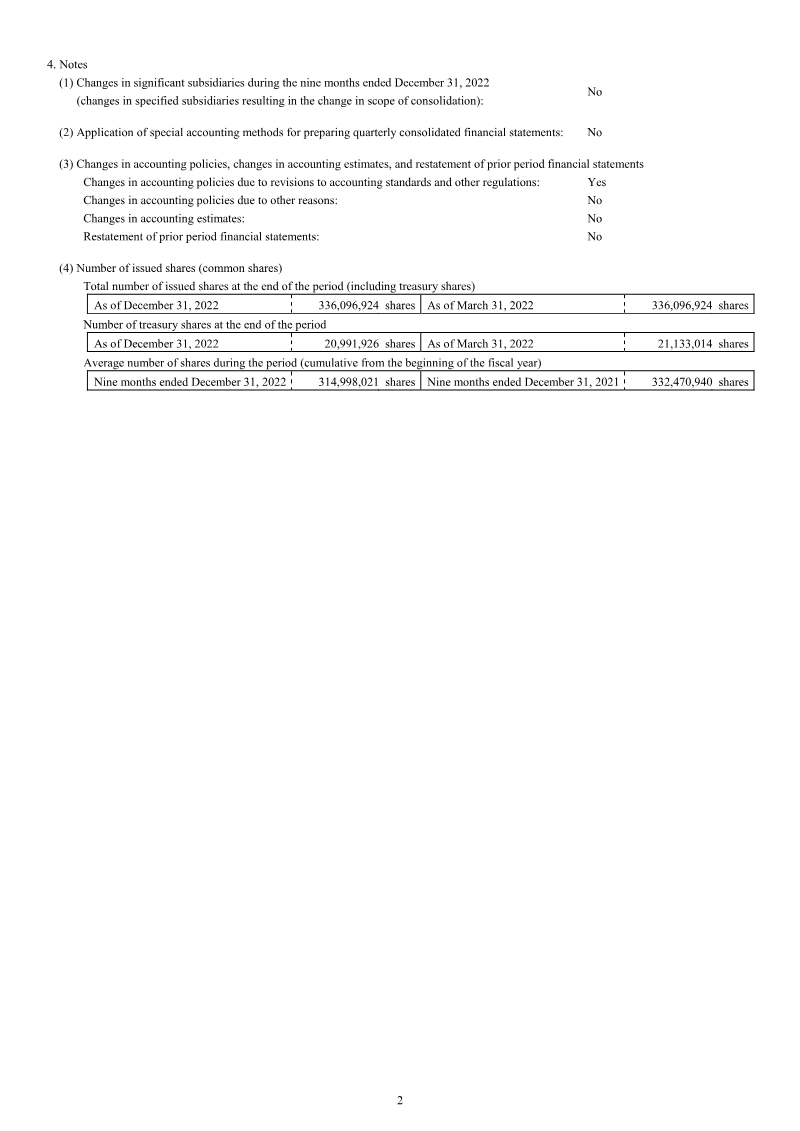

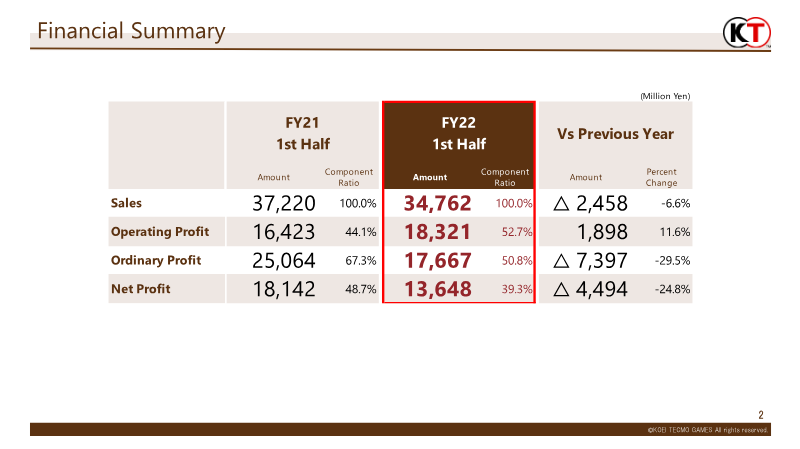

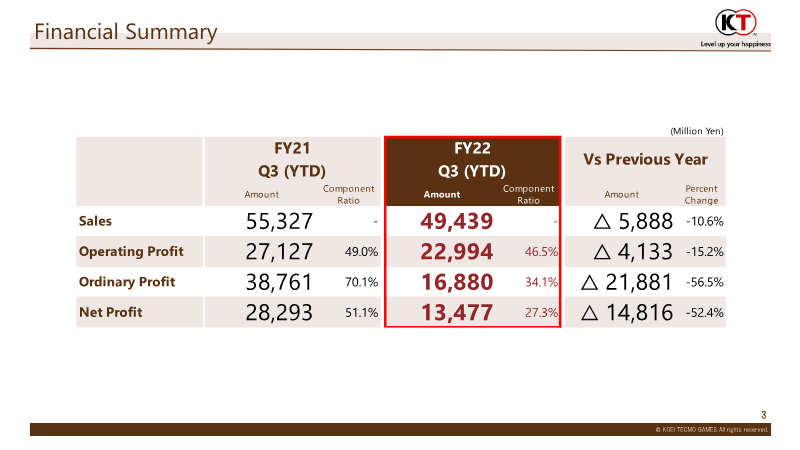

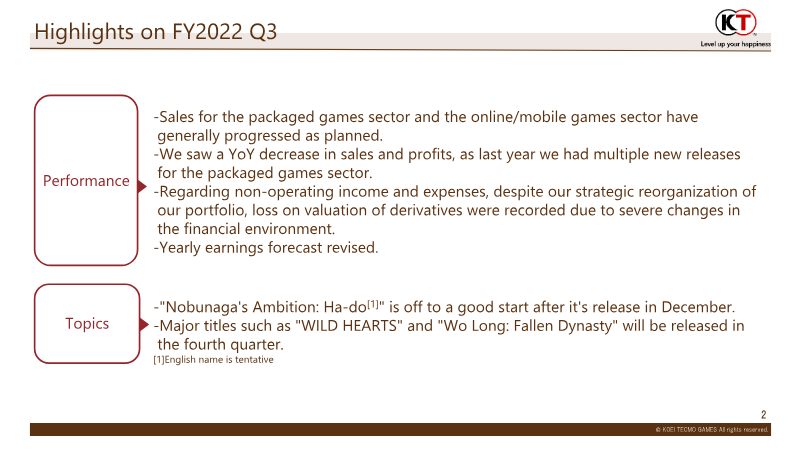

Koei Tecmo Holdings presented its financial results for the third quarter of the fiscal year ending March 2023, revealing a period of transition characterized by a year-over-year decline in sales and profits. Net sales reached 49.4 billion yen, a 10.6% decrease from the previous year, while net profit fell 52.4% to 13.5 billion yen. This downturn is attributed primarily to a high baseline in the prior year driven by major packaged game releases and significant non-operating losses on the valuation of derivatives caused by a volatile financial environment. The entertainment segment remains the primary driver of the business, contributing 46.3 billion yen in sales. While console software sales saw a decline in physical package revenue, digital sales remained resilient, accounting for 78.8% of the entertainment segment's total sales. Geographically, the company maintains a balanced profile, with 51.6% of revenue generated in Japan and 48.4% from overseas markets, particularly in Asia and North America. Despite the dip in revenue, total unit sales actually increased by 4.9% to 5.98 million units, bolstered by strong digital downloads. Looking ahead, the company revised its full-year earnings forecast, raising its operating profit target to 34 billion yen while lowering ordinary and net profit expectations due to the aforementioned non-operating expenses. Growth strategy for the fourth quarter relies on a robust pipeline of global releases, including high-profile titles such as Wild Hearts, Wo Long: Fallen Dynasty, and Atelier Ryza 3. Additionally, the mobile sector showed momentum with the successful launch of Nobunaga’s Ambition: Ha-do and continued regional expansion of existing smartphone IPs. To support this long-term growth, the company increased its total headcount by 15.7% to 2,400 employees.

Koei TecmoJan 2023