Investment

Financial

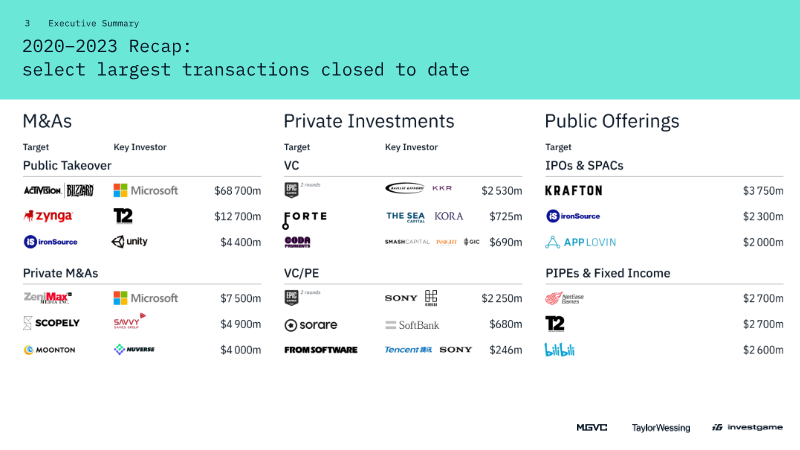

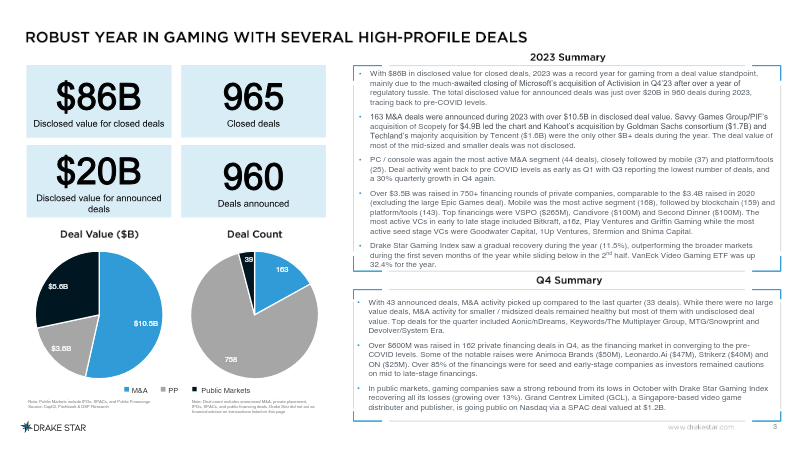

Gaming Report: VC Trends and Emerging Opportunities 2023

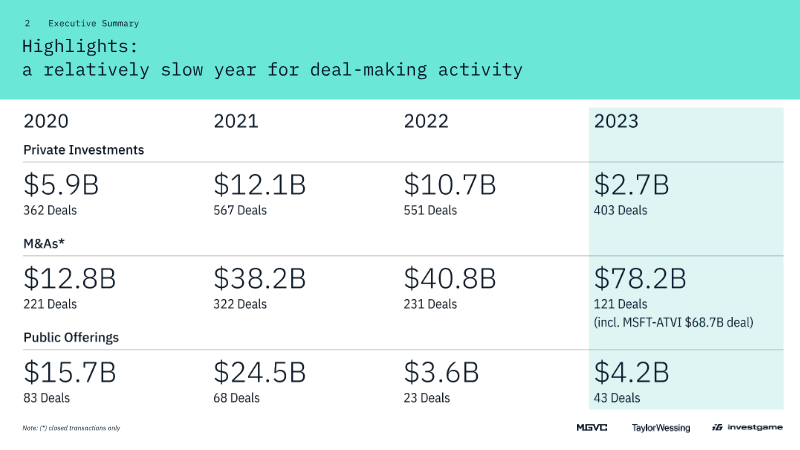

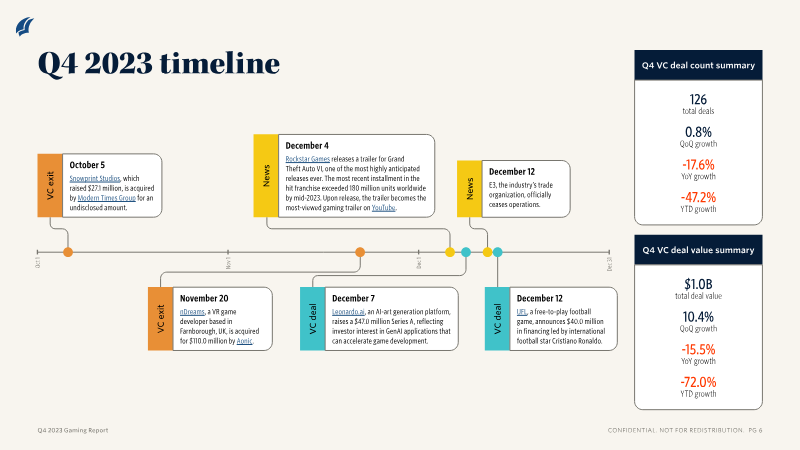

The report examines global gaming venture capital activity in 2023, focusing on Q4 performance and broader industry trends. In the fourth quarter, 126 deals raised $1.0 billion, a modest 0.8 % increase in deal count and 10.4 % rise in value versus the prior quarter, yet both metrics fell sharply year‑over‑year by 17.6 % and 15.5 %. Cumulative 2023 activity reached $4.1 billion, the second‑lowest annual figure since 2017 and only slightly above 2019 levels. The data, sourced from PitchBook, cover all geographic regions and include studios, publishers, developer tools, SaaS platforms, and content segments. Key findings reveal that content‑related startups attracted the largest share of capital in Q4 ($438.4 million across 71 deals), followed by development firms ($288.7 million, 29 deals). Other segments—access, monetization, and gambling—experienced subdued activity. The report notes a shift in investor focus toward more mature business models such as SaaS and developer tools, reflecting the high capital intensity of game development. Methodologically, the analysis aggregates PitchBook’s deal database, reporting both quarterly and cumulative figures. It also highlights notable early‑stage deals (e.g., Stability AI, Leonardo.ai) and strategic acquirers (Unity, Sony Interactive Entertainment). The document concludes that while overall VC enthusiasm has cooled from the Web3 and metaverse peaks of 2020‑22, investment remains concentrated in content creation and developer tooling, suggesting a more realistic, sustainable growth trajectory for the gaming ecosystem.

PitchBookJan 2023

Financial

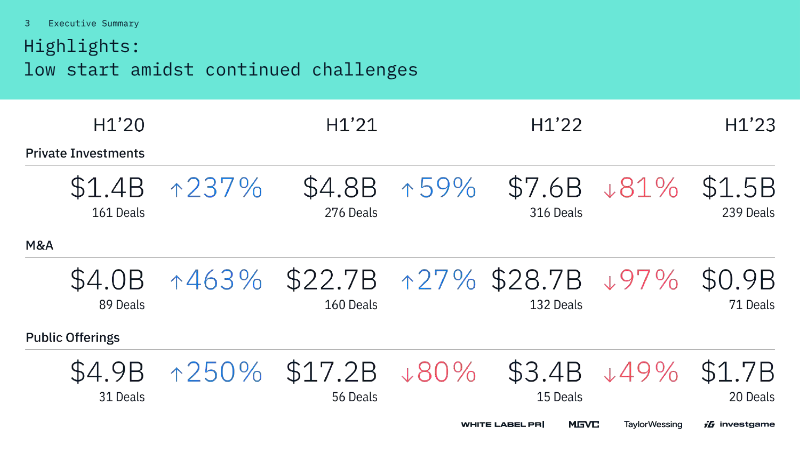

Gaming Deals Report: Navigating Turbulence (H1’23)

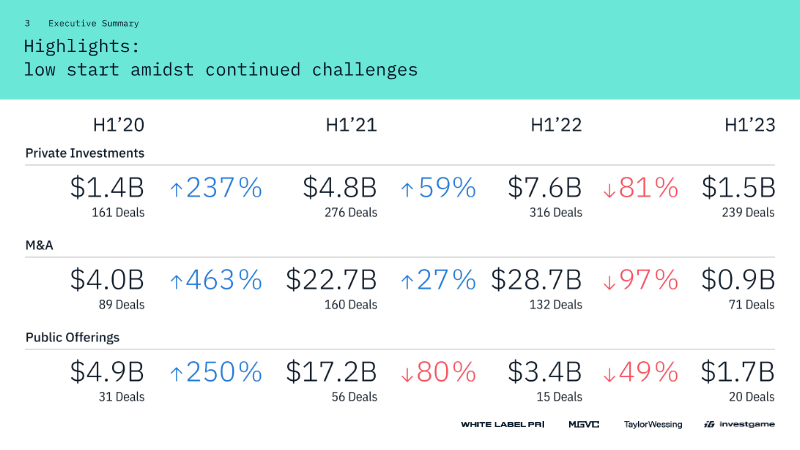

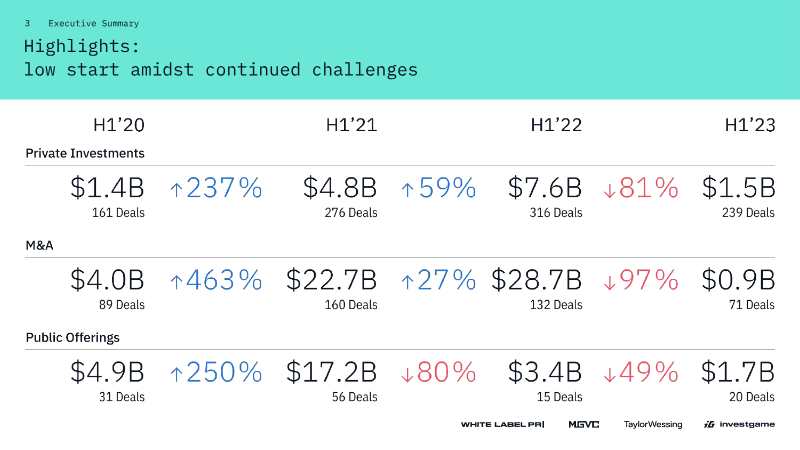

The first half of 2023 marked a significant downturn in gaming industry deal activity, characterized by a sharp contraction in total deal value across private investments, mergers and acquisitions (M&A), and public offerings. Total private investment fell to $1.5 billion across 239 deals, representing a fivefold decline in value compared to the same period in 2022. M&A activity saw an even more dramatic 31x drop in value, falling to $0.9 billion as strategic investors shifted focus toward internal restructuring, layoffs, and cost optimization rather than aggressive expansion. The venture capital landscape remains dominated by early-stage activity, as pre-seed and seed rounds are less susceptible to macroeconomic volatility. While the number of early-stage deals remained relatively stable, the total capital raised shrank by more than half to $269 million. Late-stage investments have largely paused due to a closed IPO window and a lack of viable exit opportunities, leading to a disconnect between investor expectations and startup valuations. Geographically, North America led early-stage VC activity with 24 deals, followed by Western Europe and the MENA region. Public markets remained muted, with companies increasingly choosing to postpone listings or engage in share buybacks. Despite the general market cooling, artificial intelligence has emerged as a resilient niche; investments in AI-related gaming companies rose to $214.1 million across 19 deals in the first half of 2023. Analysts anticipate a potential recovery in the latter half of the year, driven by the closing of major pending deals, such as the Savvy Games Group acquisition of Scopely and Microsoft’s pursuit of Activision Blizzard, alongside a significant amount of unallocated venture capital waiting to be deployed.

InvestGameJan 2023