Japan

Report

FY2016 First Quarter Financial Results

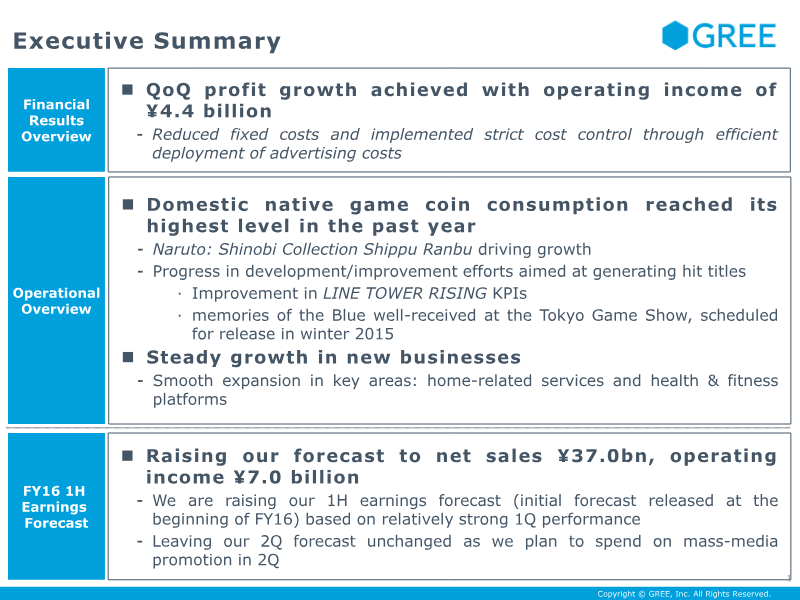

The FY2016 first‑quarter results demonstrate a modest improvement in profitability driven primarily by cost discipline and strong native game performance. Net sales fell 1.6 % QoQ to ¥19.3 billion, while operating income rose 0.17 billion to ¥4.4 billion, marking a 2.6‑percentage‑point increase in operating margin to 22.7 %. EBITDA mirrored this trend, declining slightly QoQ but remaining above the previous year’s level. The decline in total costs of ¥1.8 billion—largely from reduced advertising spend (from 8.3 % to 6.3 % of sales) and lower commission fees—offset modest revenue contraction. Key drivers include the domestic native game “Naruto: Shinobi Collection Shippu Ranbu,” which achieved record coin consumption and contributed to a 60 billion‑coin spike, while “Shometsu Toshi” and “SAMURAI Kingdom” maintained steady sales. The company’s native game pipeline expanded to 16 titles, with two new releases in Q2 and several first‑party projects slated for later in the year. Web game operations improved efficiency by cutting server numbers and shifting offshore work to Vietnam, preserving profitability despite a 26 % YoY cost reduction. Geographically, the company operates in Japan and overseas markets, with a growing European version of “Knights & Dragons” and next‑gen releases in development. The 1H forecast was raised to ¥37 billion in sales and ¥7 billion operating income, reflecting confidence in the Q1 momentum while maintaining a conservative outlook for new IP and advertising spend. The report relies on consolidated financial statements, cost‑structure analysis, and internal KPI tracking to support its projections.

GREE

Report

Summary of Financial Results for First Quarter: Fiscal Year Ending December 31, 2015

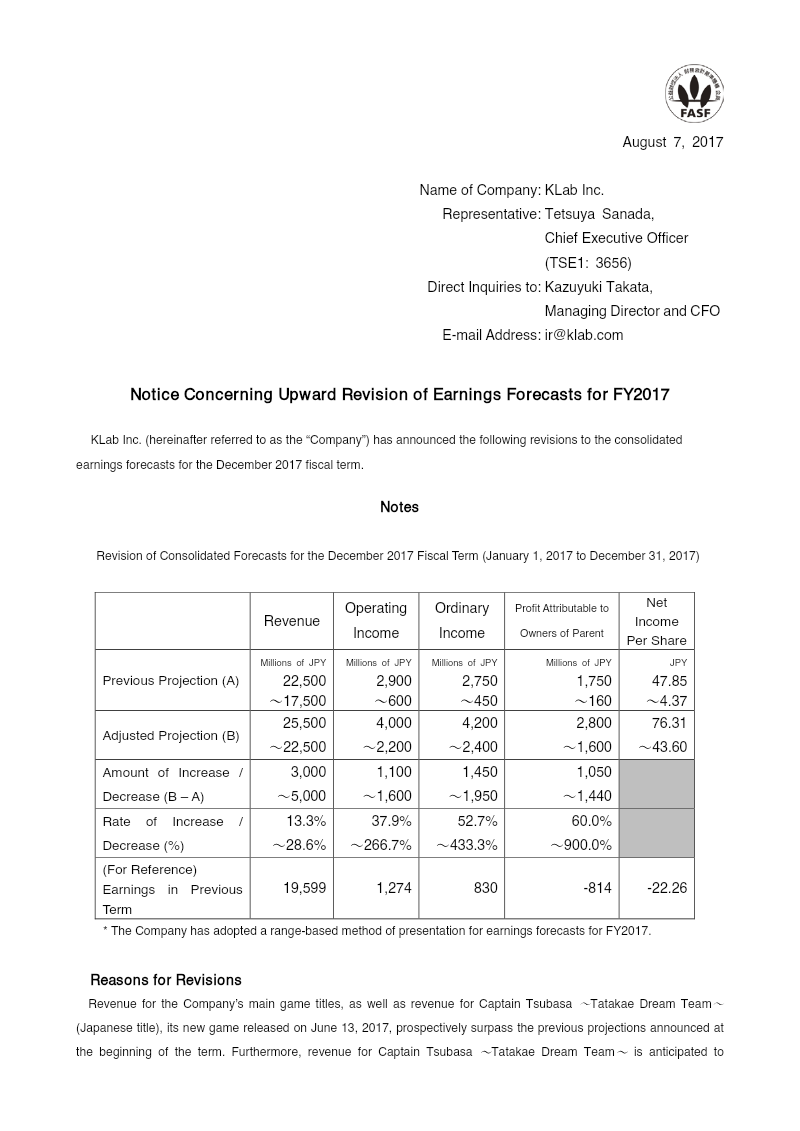

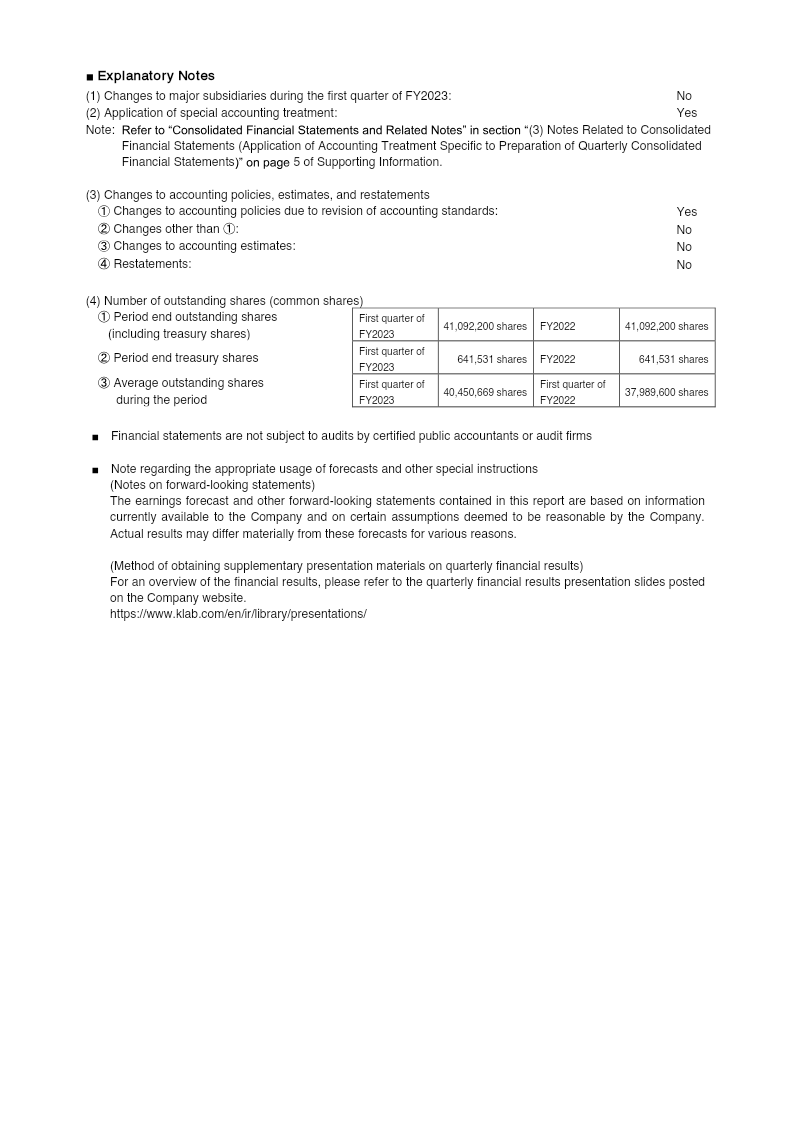

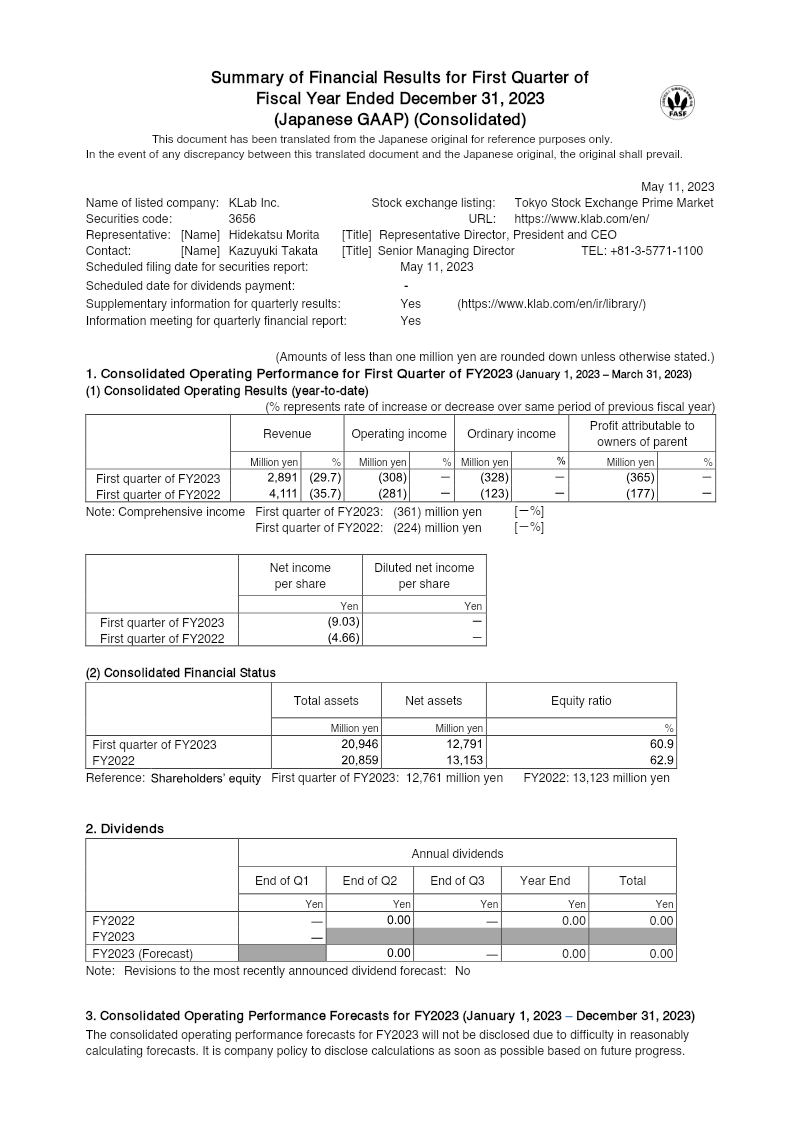

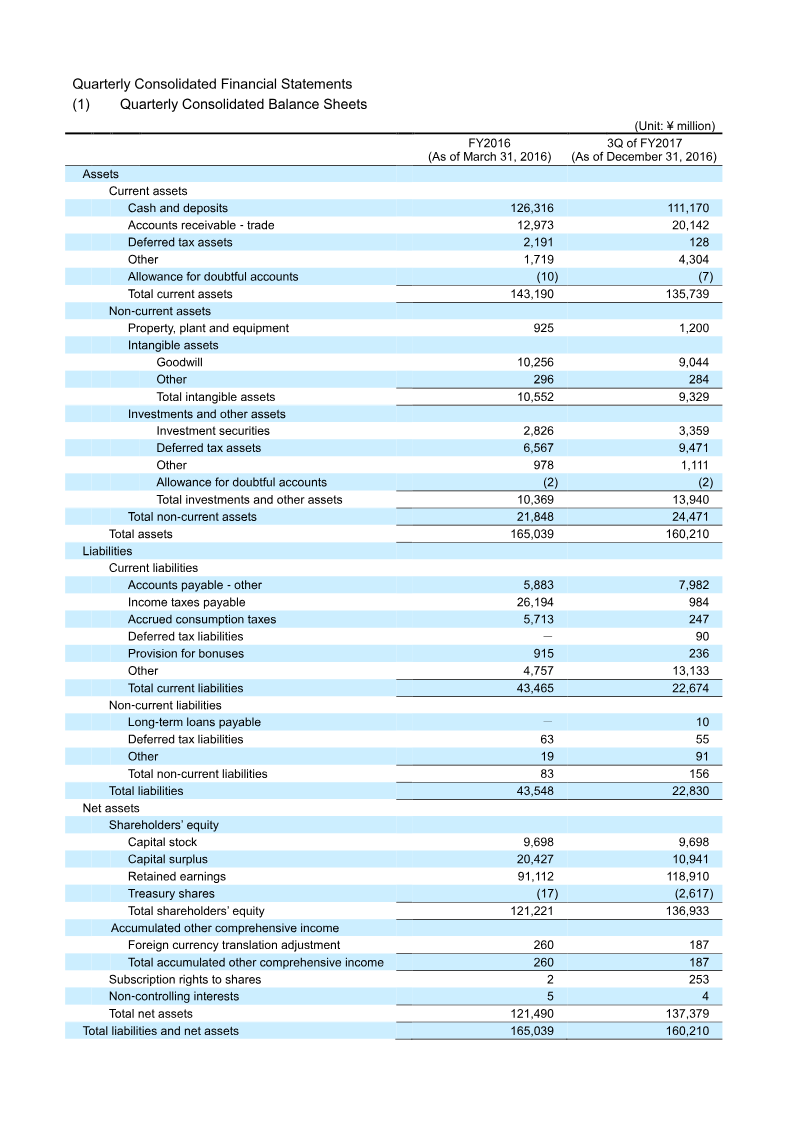

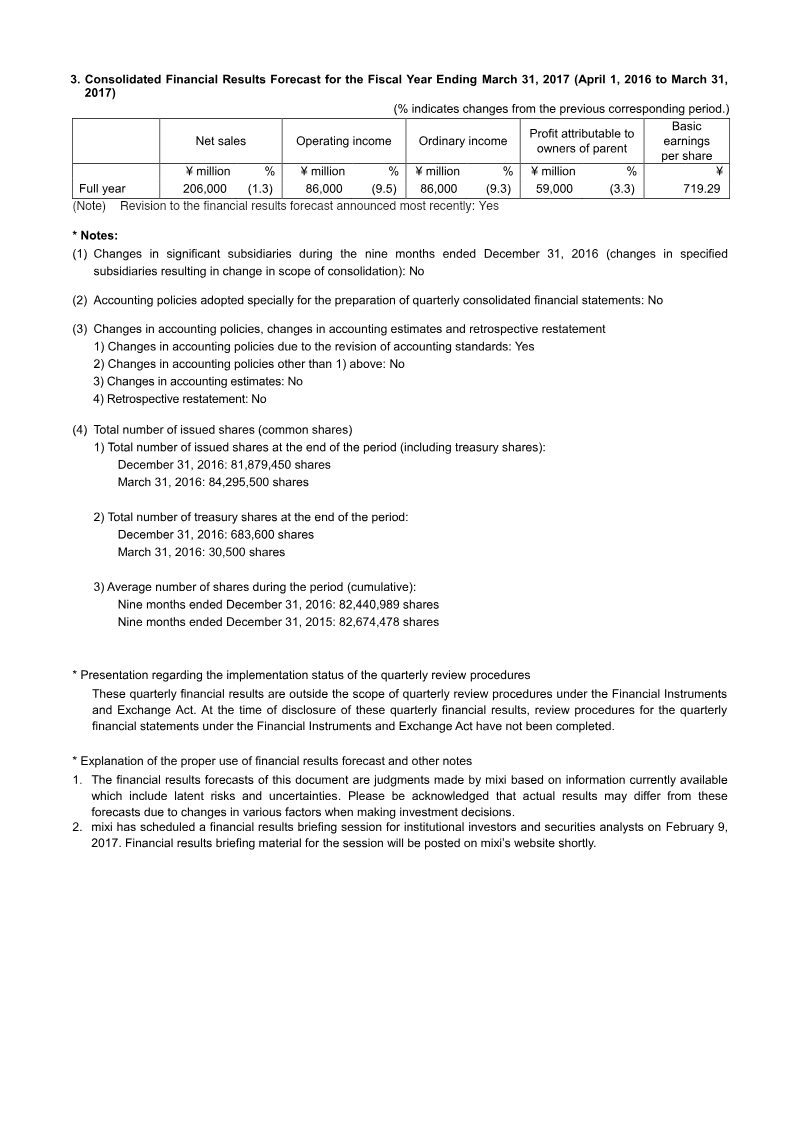

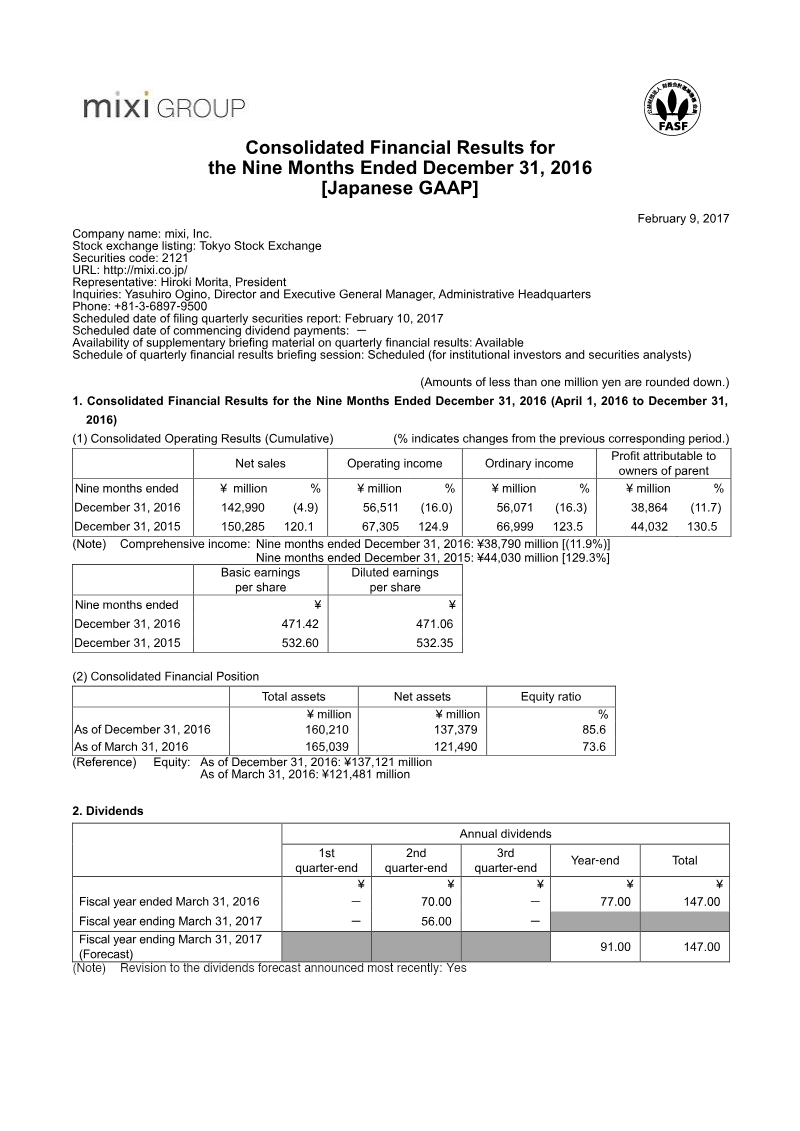

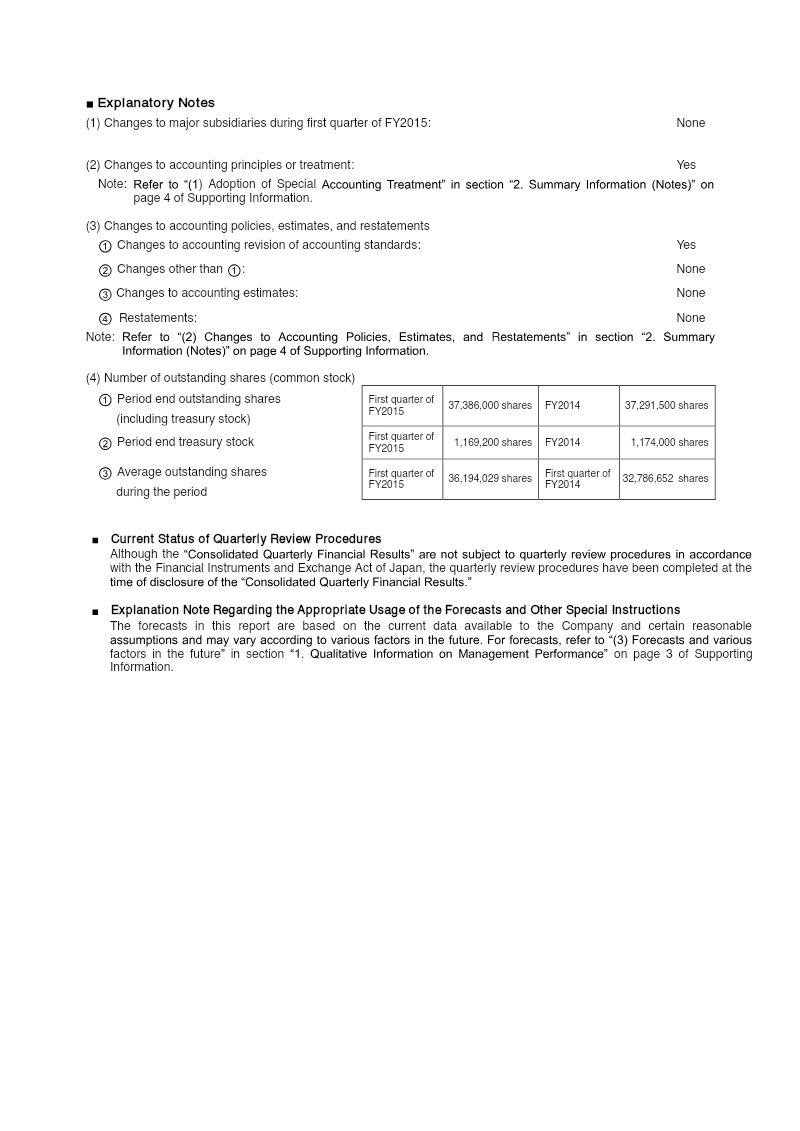

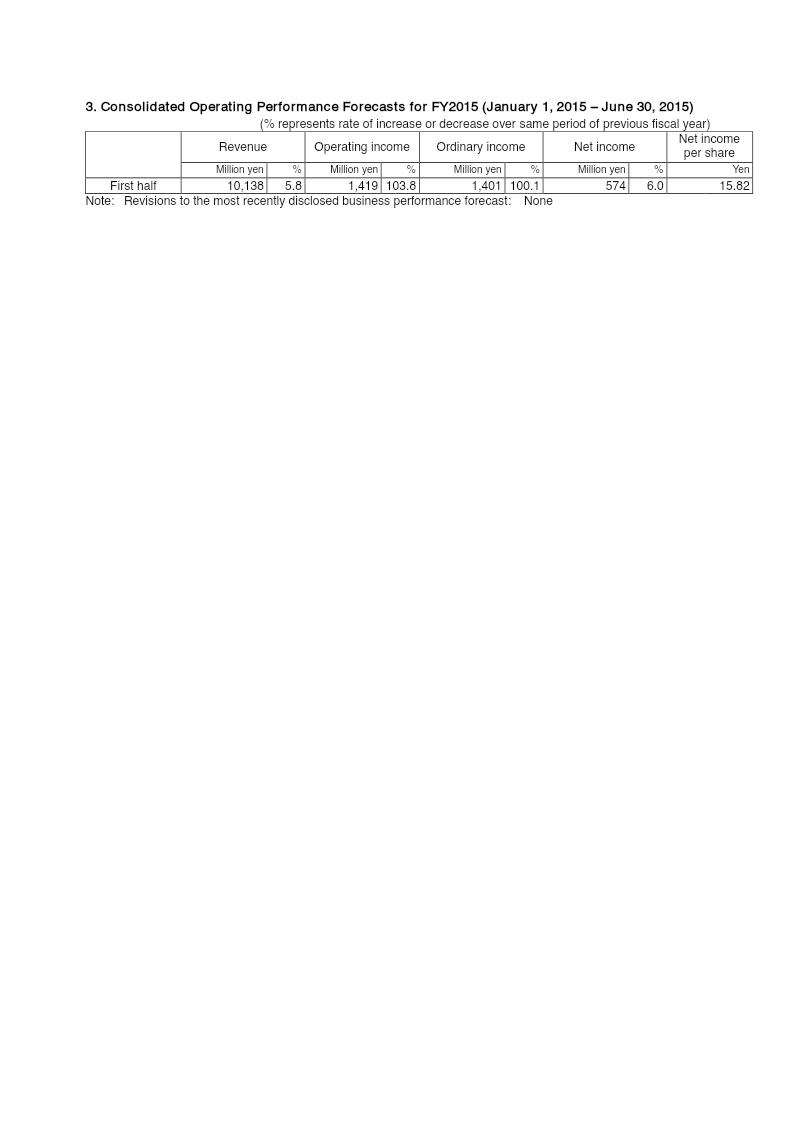

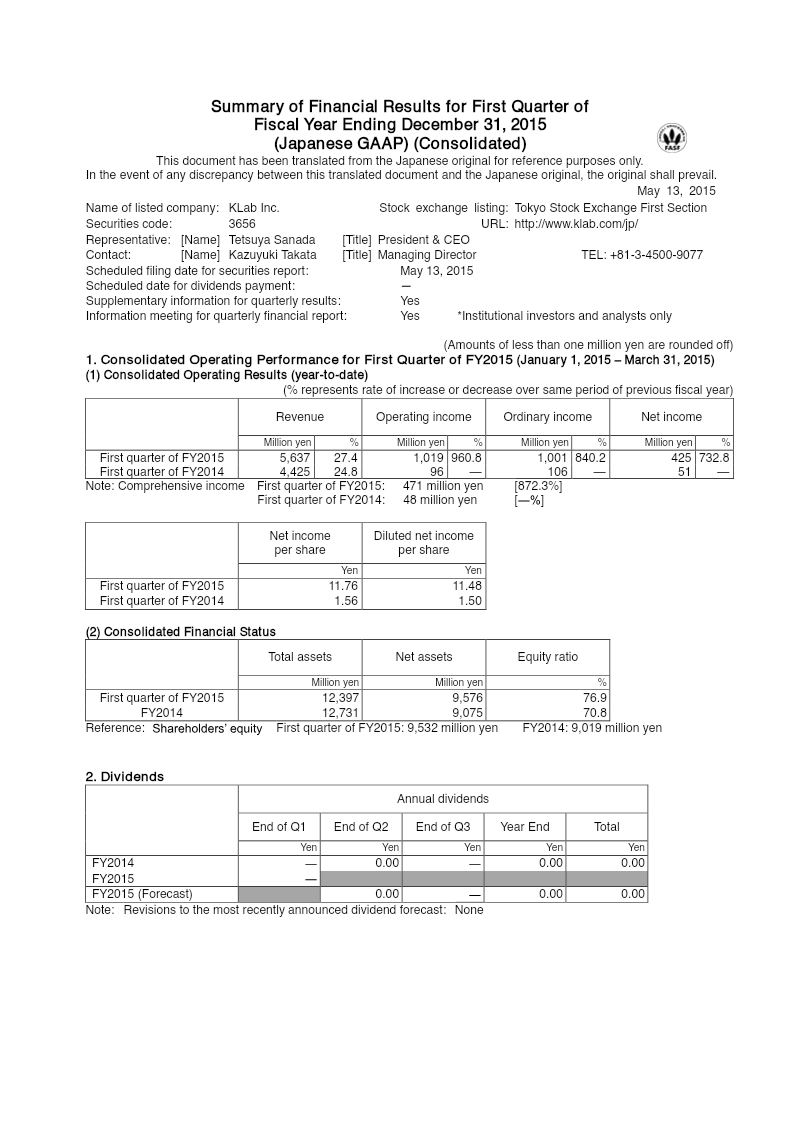

KLab Inc. reported first‑quarter fiscal 2015 results that marked a dramatic turnaround from the same period in FY2014. Consolidated revenue rose 27.4 % to ¥5,637 million, driven by strong sales of “Celestial Craft Fleet” and “Tales of Asteria,” while operating income surged 960.8 % to ¥1,019 million and net income climbed 732.8 % to ¥426 million. The company’s comprehensive income for the quarter reached ¥471 million, an 872 % increase over FY2014. Net assets grew to ¥9,576 million, reflecting a 5.2 % rise in retained earnings and an equity ratio of 76.9 %. Total assets declined slightly to ¥12,397 million as current assets fell due to lower cash and receivables, whereas intangible assets increased by ¥160 million. The first‑half forecast projects revenue of ¥10,138 million and net income of ¥574 million, indicating continued momentum. No dividends were declared for FY2014 or FY2015, and the forecasted dividend remains unchanged. The company applied a special accounting treatment for employee stock ownership plans, but this had no material impact on the quarterly statements. The fiscal year is covered under Japanese GAAP, with a sample of 37 million shares outstanding and an average of 36.2 million shares during the quarter. The report is based on consolidated financial statements, including balance sheets, income statements, and comprehensive income, with no significant changes in accounting policy beyond the adoption of a trust‑based employee stock plan.

KLab