Investment

Whitepaper

African Game Developer Resource Kit: Funding and Financing

The African game development landscape faces a unique set of financial challenges and opportunities characterized by a growing ecosystem of independent studios seeking to scale within a global market. The primary objective of this analysis is to map the diverse funding mechanisms available to African creators, ranging from traditional venture capital and private equity to specialized grants and publisher-led financing. By examining the current economic infrastructure, it becomes clear that while the continent possesses a wealth of creative talent and a rapidly expanding youth population, access to sustainable capital remains a significant barrier to entry for many emerging developers. Key findings indicate that successful financing often depends on a studio’s ability to navigate both local and international investment climates. Data suggests that early-stage studios frequently rely on bootstrapping or small-scale grants, while more mature entities are increasingly attracting interest from global publishers looking for original intellectual property and untapped market potential. The scope of this assessment covers the broader Sub-Saharan African region, focusing on major hubs such as South Africa, Nigeria, and Kenya, and spans the current fiscal period to provide a contemporary snapshot of the industry’s financial health. Methodologically, the insights are derived from a synthesis of market trends, investment patterns, and the specific requirements of various funding bodies. The analysis concludes that for the African gaming sector to reach its full economic potential, there must be a concerted effort to bridge the gap between creative output and investor readiness. This involves not only increasing the volume of available capital but also educating developers on the nuances of equity, revenue-sharing models, and the strategic importance of intellectual property management in securing long-term growth.

Games Industry Africa

Report

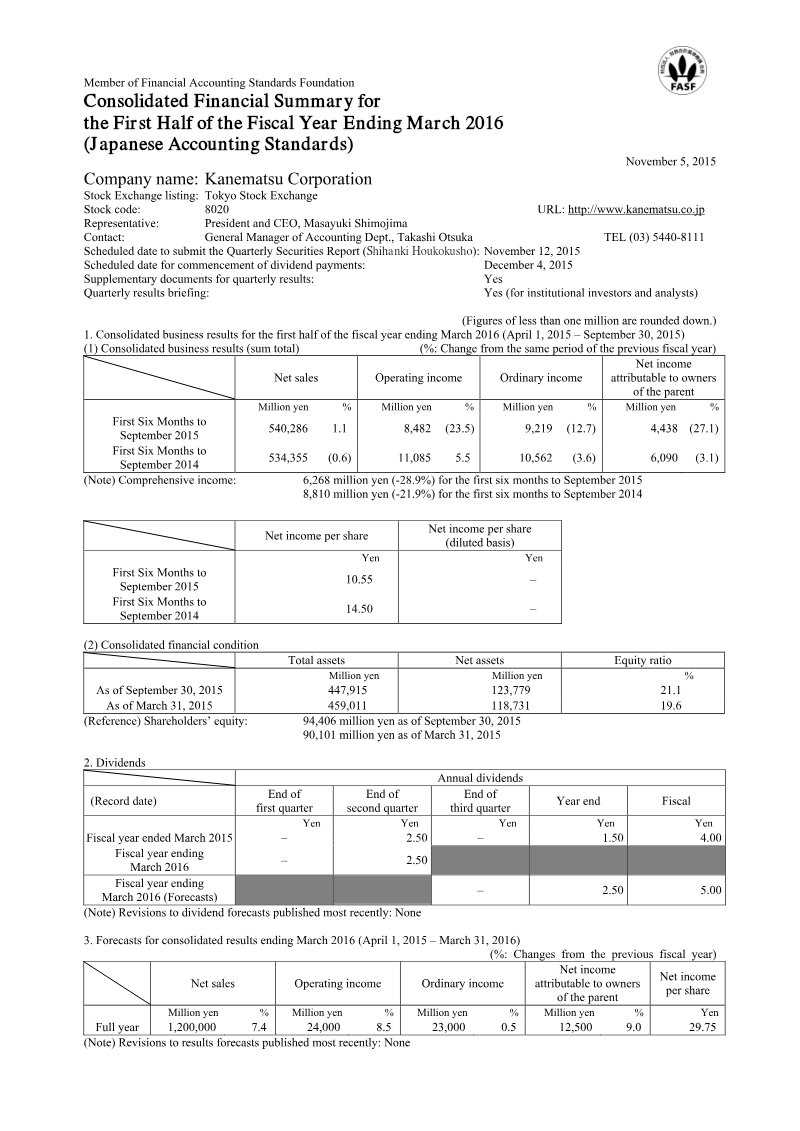

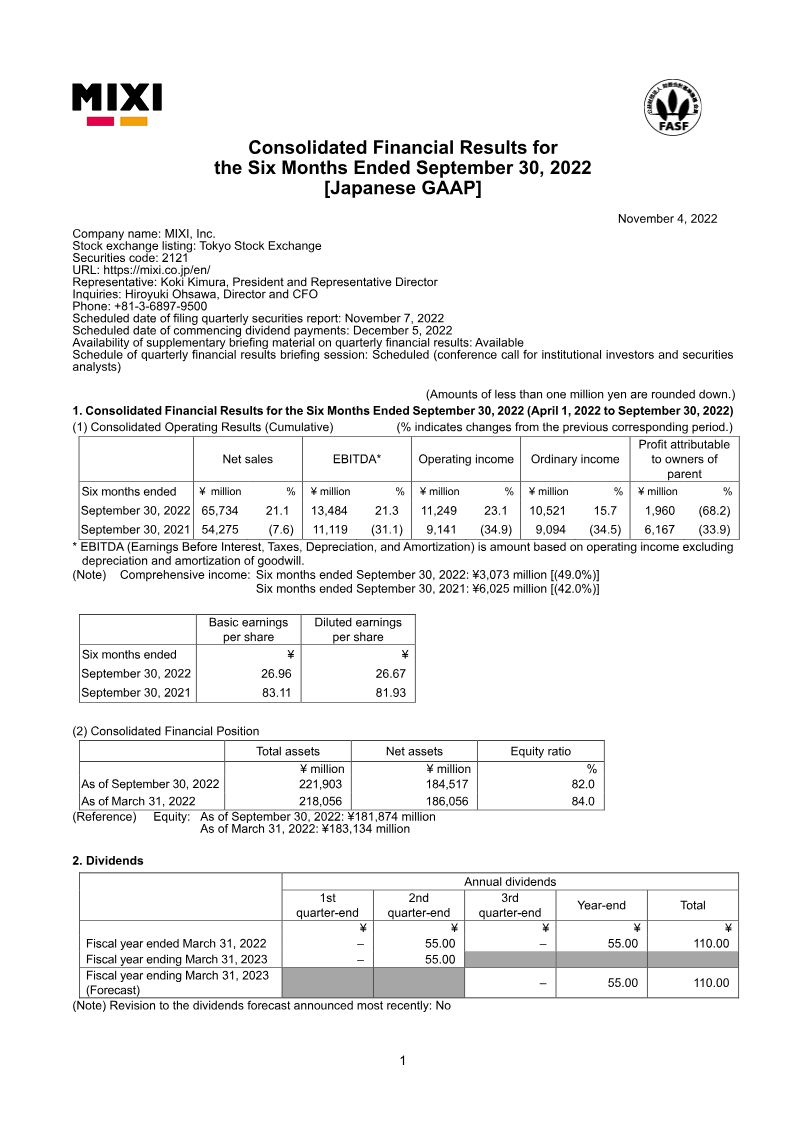

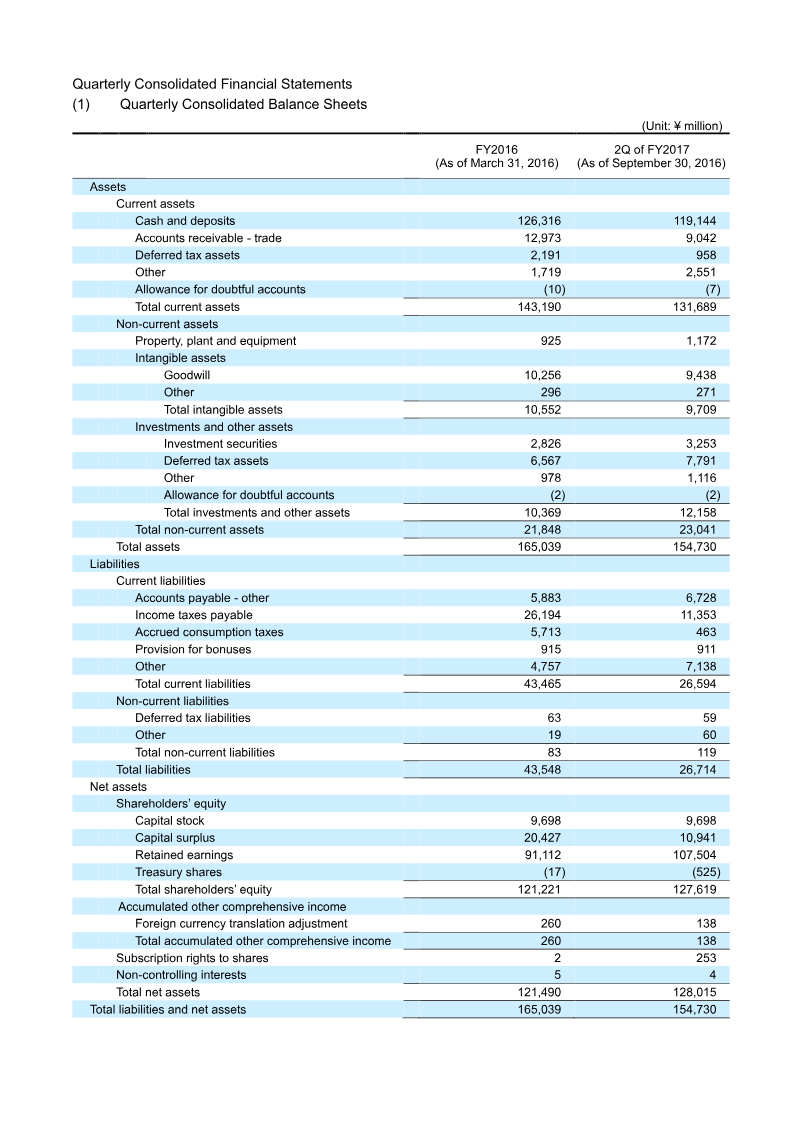

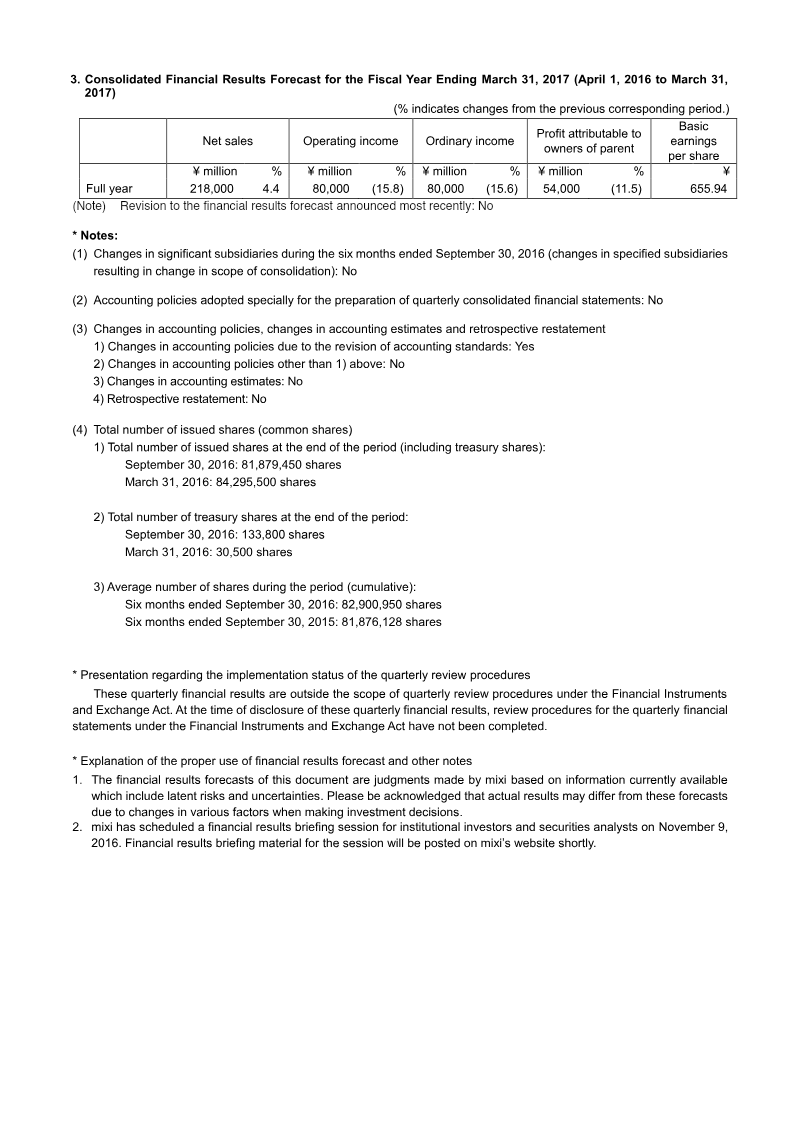

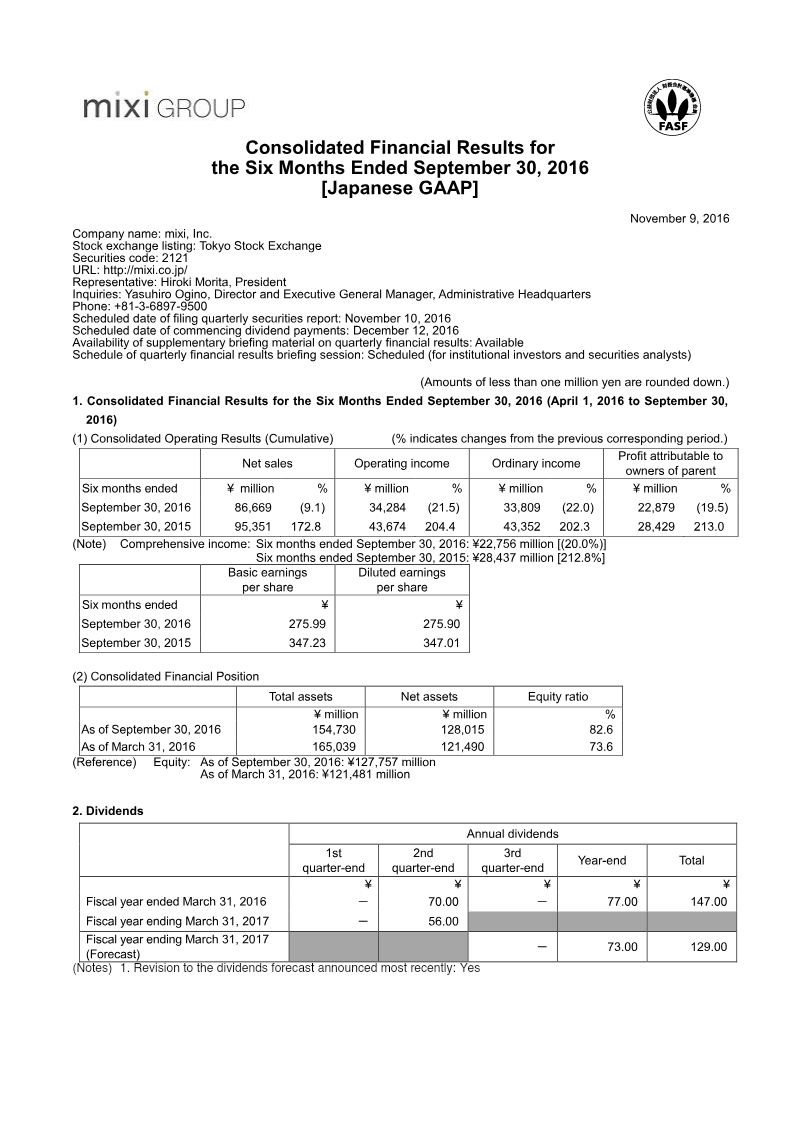

Financial Results: First Half of Fiscal Year Ending March 2013

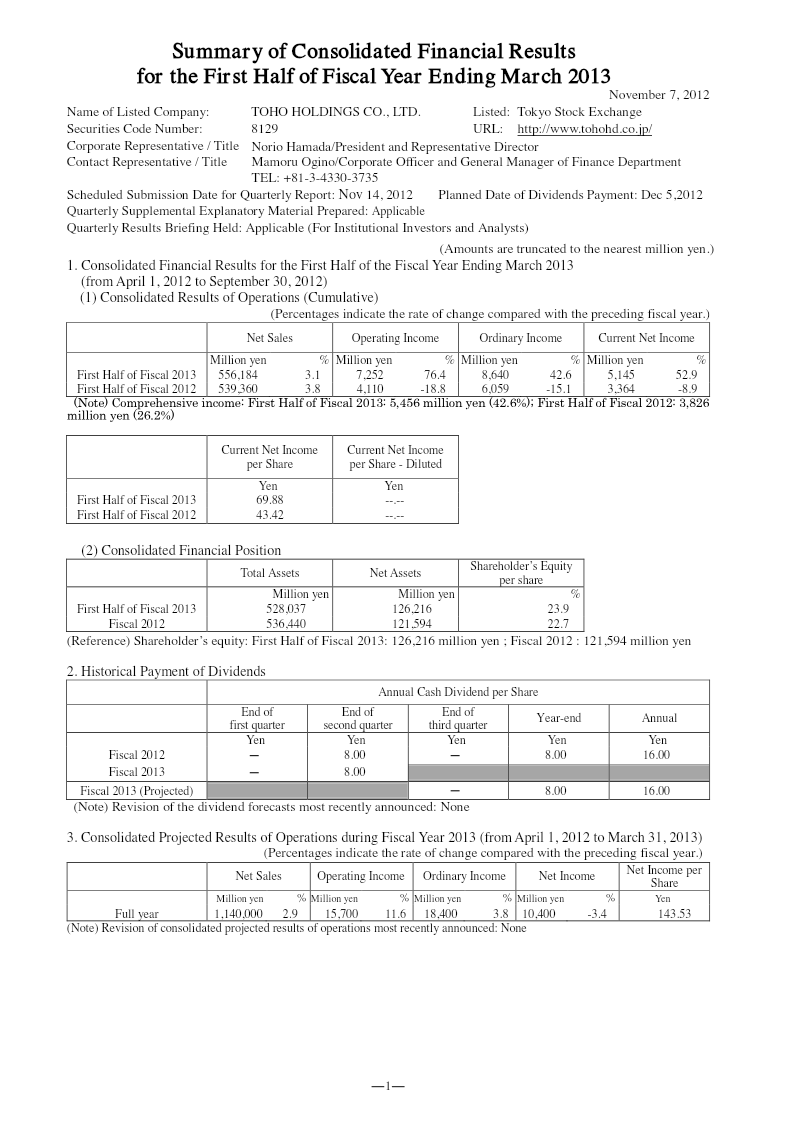

TOHO HOLDINGS CO., LTD. reported its consolidated financial results for the first half of the fiscal year ending March 2013, covering the period from April 1, 2012, to September 30, 2012. The company’s primary objective during this period was to navigate a challenging market environment characterized by a 6.0% average reduction in National Health Insurance (NHI) drug prices. To maintain competitiveness, the group utilized a strategy balancing customer support services with pharmaceutical sales, alongside efforts to address distribution inefficiencies and pricing gaps between NHI and market rates. Financial performance showed positive growth across key metrics compared to the same period in the previous year. Net sales reached 556,184 million yen, a 3.1% increase, while operating income rose significantly by 76.4% to 7,252 million yen. Ordinary income and net income also saw substantial gains, increasing by 42.6% and 52.9%, respectively. The pharmaceutical wholesaling segment served as the primary driver of this growth, reporting 535,234 million yen in sales and a 214.6% increase in segment profit. Conversely, the dispensing pharmacy segment experienced a 13.8% decline in segment profit, attributed to the costs associated with establishing new pharmacies and hiring additional pharmacists. The company’s financial position remained stable, with total assets of 528,037 million yen and a shareholder equity ratio of 23.9%. During this period, the company implemented a change in its depreciation method for tangible fixed assets acquired after April 1, 2012, to align with revisions in the Corporation Tax Law. Despite the operational challenges posed by regulatory price revisions, the company maintained its full-year earnings projections, signaling confidence in its ongoing proposal-based marketing and service expansion strategies.

TOHO HOLDINGS CO.