Investment

Report

Sprawozdanie z badania rocznego sprawozdania finansowego: 2024

The audit report confirms that PCF Group Spółka Akcyjna’s 2024 financial statements, prepared under International Financial Reporting Standards and European regulatory requirements, present a true and fair view of the company’s financial position as of 31 December 2024. The audited figures show total assets of PLN 42,225 thousand and equity of PLN 18,893 thousand after a write‑down for investments in subsidiaries. Revenue from contracts with customers reached PLN 166,457 thousand, while assets and liabilities related to such contracts were valued at PLN 9,580 thousand and PLN 5,808 thousand respectively. The audit identified key areas of significant judgment: valuation of contract assets and liabilities, impairment testing for investments in dependent entities, and capitalization of development costs for new games. In each case, the auditor performed substantive procedures including policy reviews, contract analysis, and discounted cash flow calculations to obtain sufficient evidence. The report also highlights uncertainty surrounding deferred tax assets of PLN 52,659 thousand due to projected future tax outcomes. Management’s responsibility for ongoing operations and internal controls is affirmed, with no material misstatement detected in the accompanying activity report or corporate governance statement. The audit was conducted in accordance with Polish and EU auditing standards, with the auditor maintaining independence throughout. Overall, the report delivers a clean opinion on the financial statements and related disclosures for the 2024 reporting period.

PCF Group

Report

Notice Regarding Variance in Performance Forecast

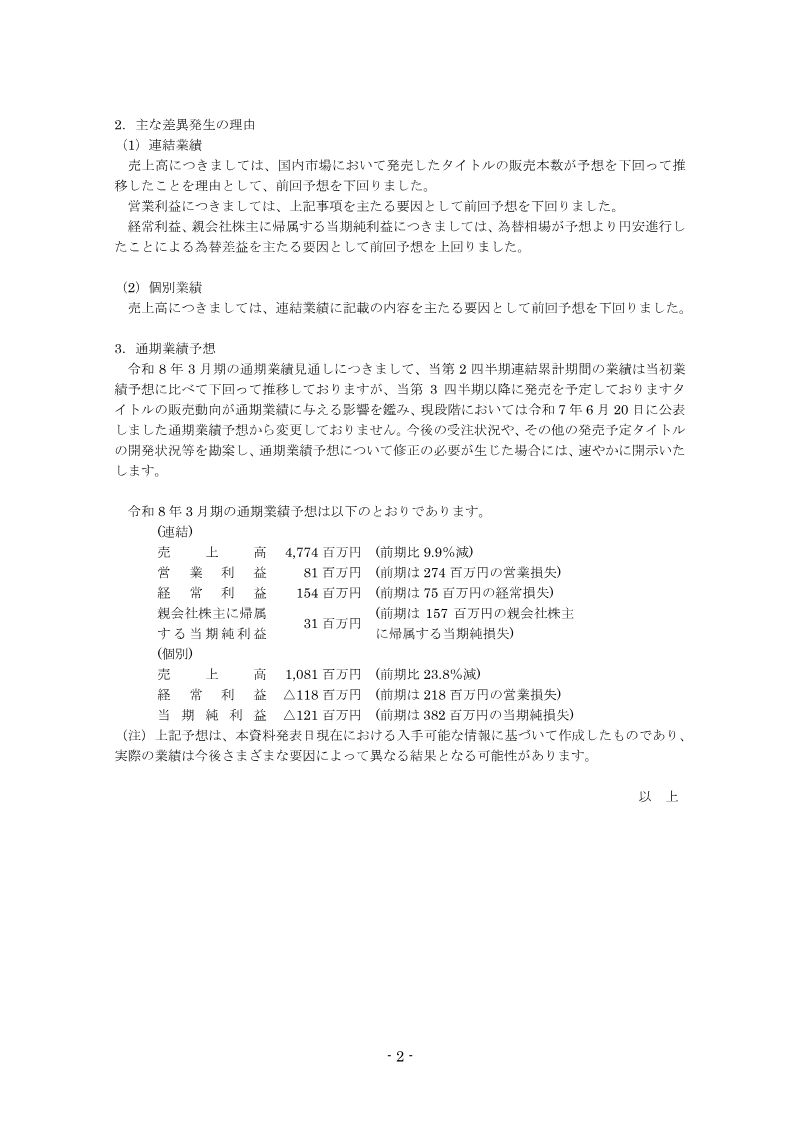

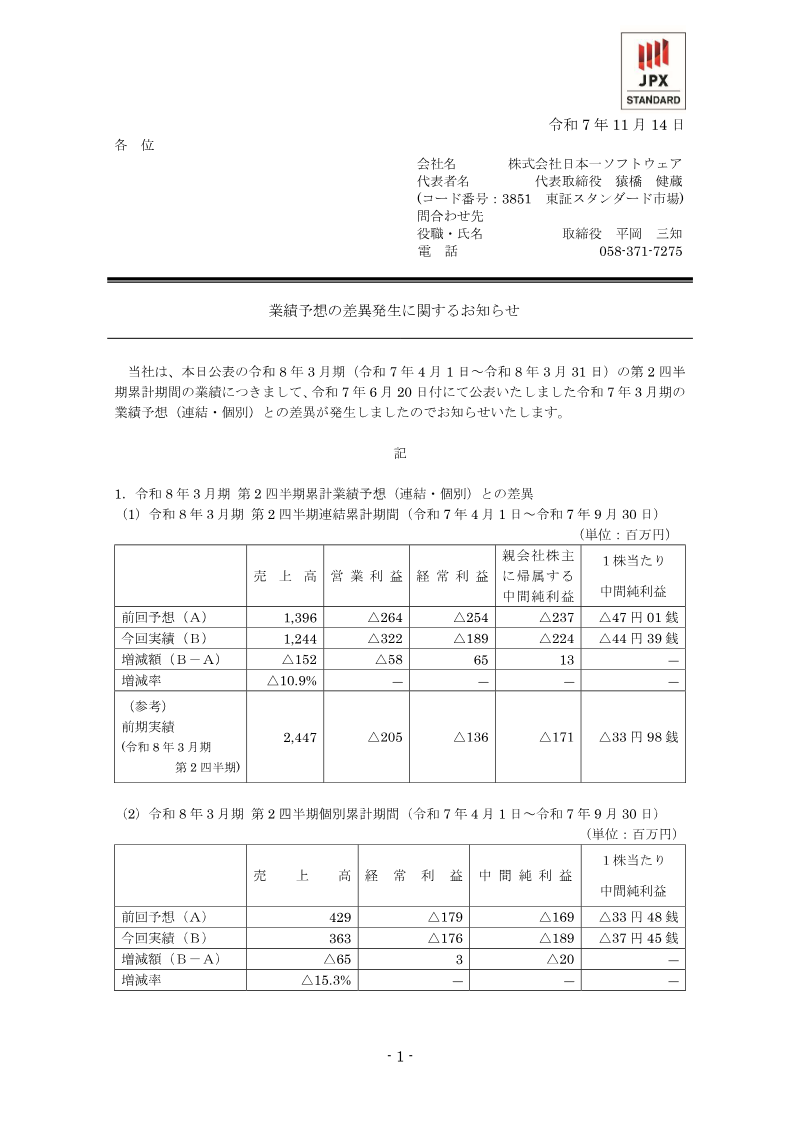

The notice informs shareholders that the second‑quarter cumulative performance for fiscal year 2028 (April 1 – September 30, 2027) differs from the previously issued forecast for fiscal year 2027. For the consolidated entity, revenue fell by ¥152 million (10.9 %) to ¥1,244 million, operating profit dropped by ¥58 million, while net income attributable to parent shareholders rose by ¥13 million due to a stronger yen‑depreciation effect. The individual subsidiary’s revenue declined by ¥65 million (15.3 %) to ¥363 million, with a modest increase in net profit of ¥4 yen per share. The primary causes cited are lower domestic sales volumes for newly released titles and a weaker yen that boosted foreign‑currency gains. Operating profit was impacted mainly by the sales shortfall, whereas ordinary and net profits benefited from favorable exchange movements. The company maintains its full‑year 2028 outlook unchanged, projecting consolidated revenue of ¥4,774 million (9.9 % decline YoY), operating profit of ¥81 million (up from a prior loss of ¥274 million), ordinary profit of ¥154 million, and parent‑shareholder net income of ¥31 million. For the individual entity, revenue is expected at ¥1,081 million (23.8 % decline), ordinary profit of –¥118 million, and net income of –¥121 million. The forecast reflects current information as of the notice date, with a disclaimer that future results may vary.

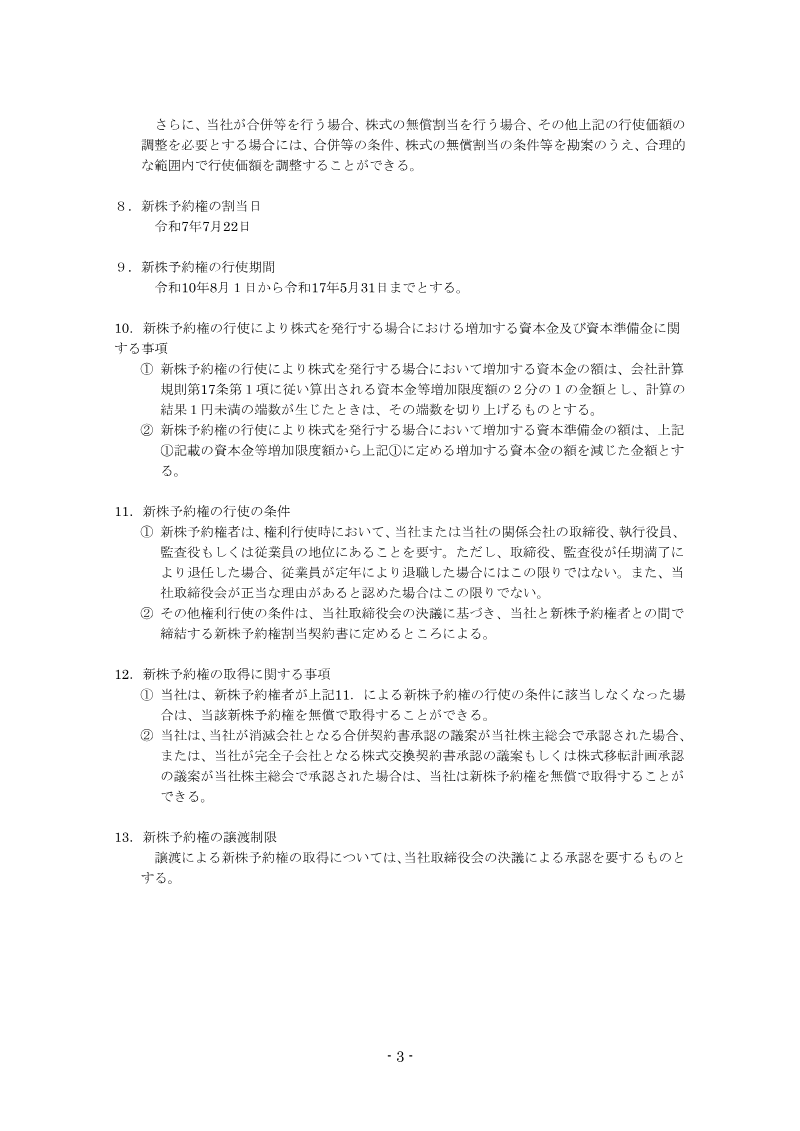

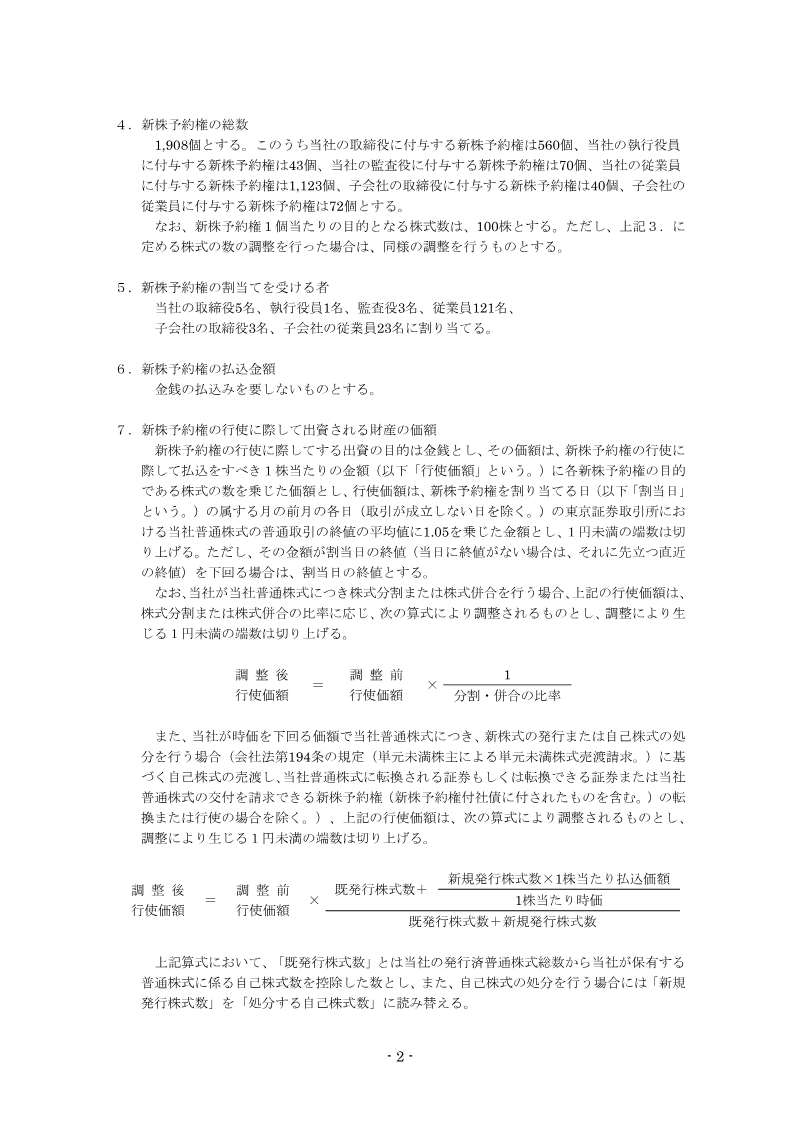

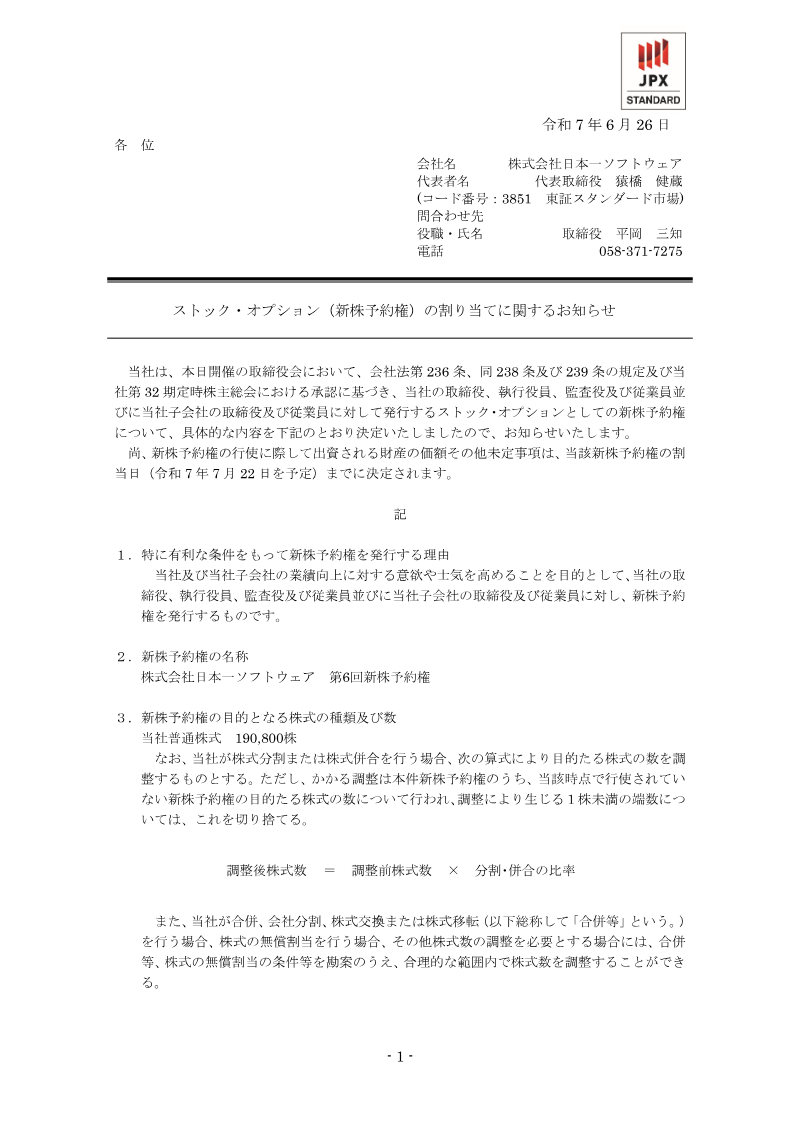

Nippon Ichi Software