Investment

Report

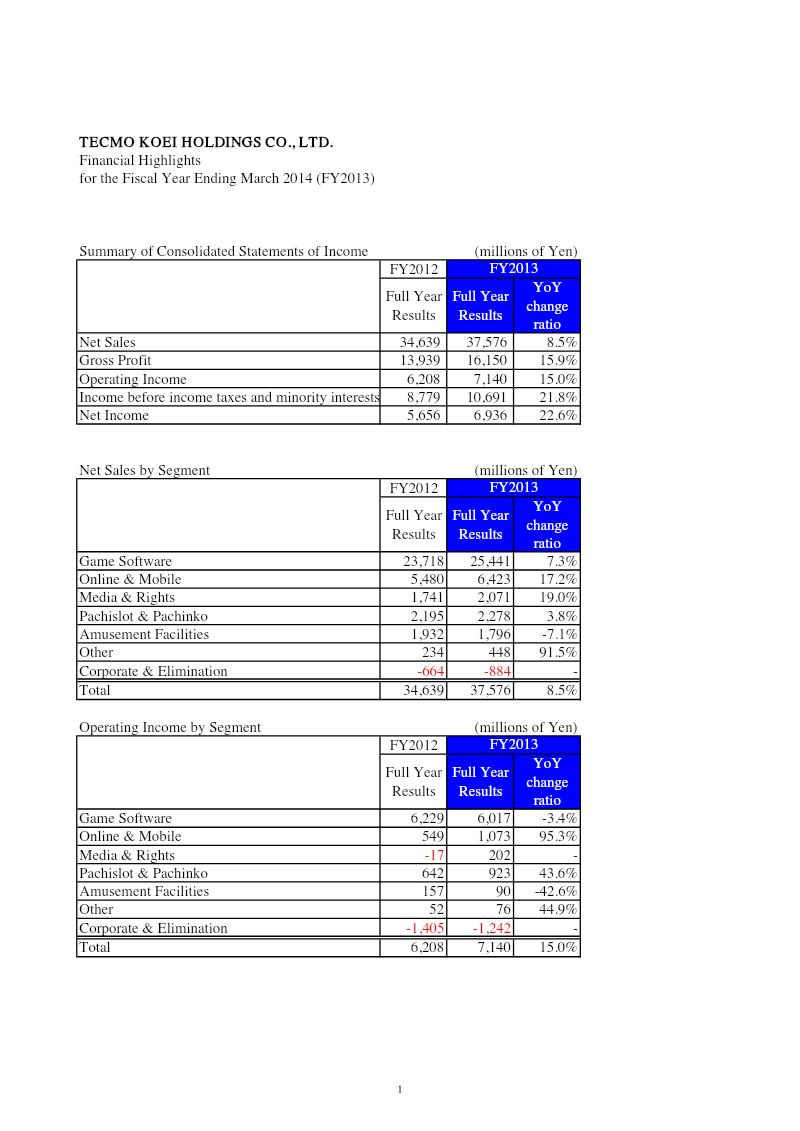

Financial Highlights: FY2013

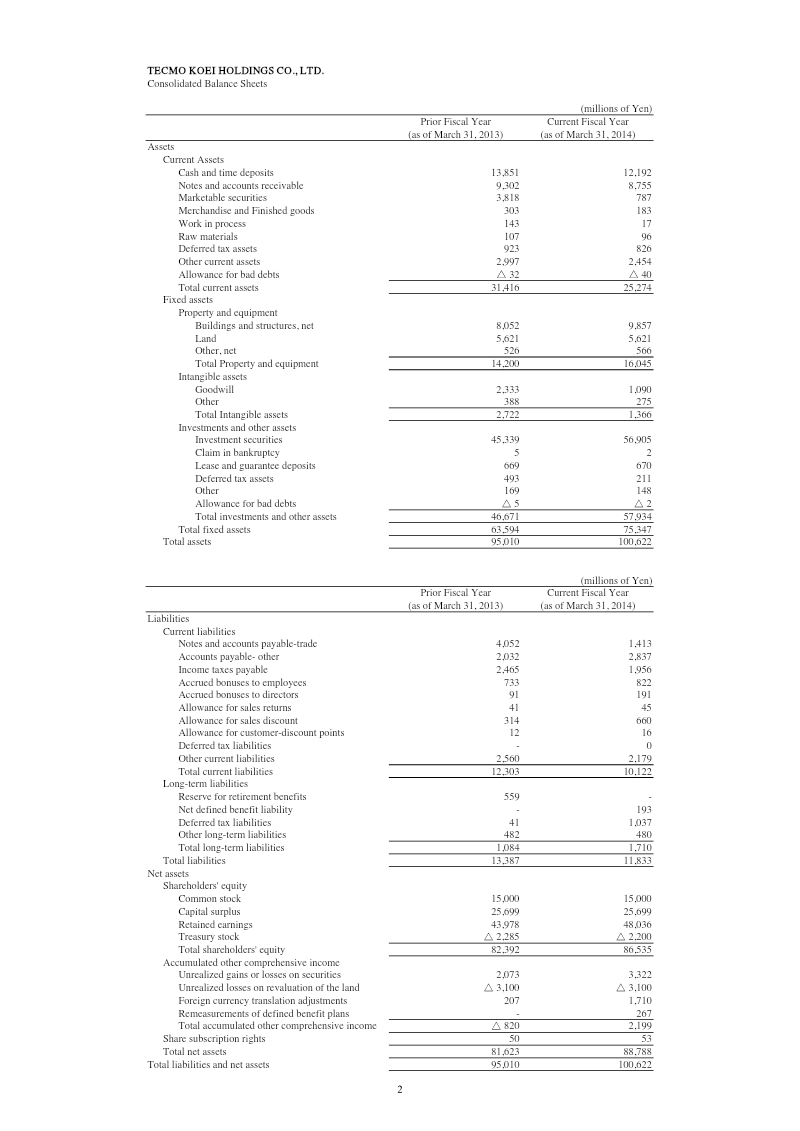

Financial highlights for the fiscal year ending March 2014 demonstrate a solid growth trajectory for Tecmo Koei Holdings. Net sales increased by 8.5 % to ¥37,576 million, driven primarily by a 7.3 % rise in Game Software sales and a notable 17.2 % jump in Online & Mobile revenue, while Media & Rights grew 19 %. Operating income expanded 15.0 % to ¥7,140 million; the Online & Mobile segment alone contributed a 95.3 % surge in operating profit, offsetting modest declines in Game Software and Amusement Facilities. Profitability metrics improved markedly: income before taxes rose 21.8 % to ¥10,691 million and net income climbed 22.6 % to ¥6,936 million. Gross profit margin widened from 40.2 % in FY2012 to 43.0 % in FY2013, reflecting efficient cost management across segments. Balance‑sheet strength is evident. Total assets grew 5.9 % to ¥100,622 million, largely due to a jump in investment securities and property & equipment. Current assets fell 19 % as cash and marketable securities were reduced, yet liquidity remained robust with current assets still exceeding current liabilities. Shareholders’ equity increased 5.4 % to ¥86,535 million, supported by retained earnings growth and a modest reduction in treasury stock. The data cover the Japanese market for FY2013, with segmental performance broken down by product lines. Figures are presented in millions of yen and reflect consolidated financial statements, providing a comprehensive view of the company’s operational and financial health during the period.

Koei Tecmo

Report

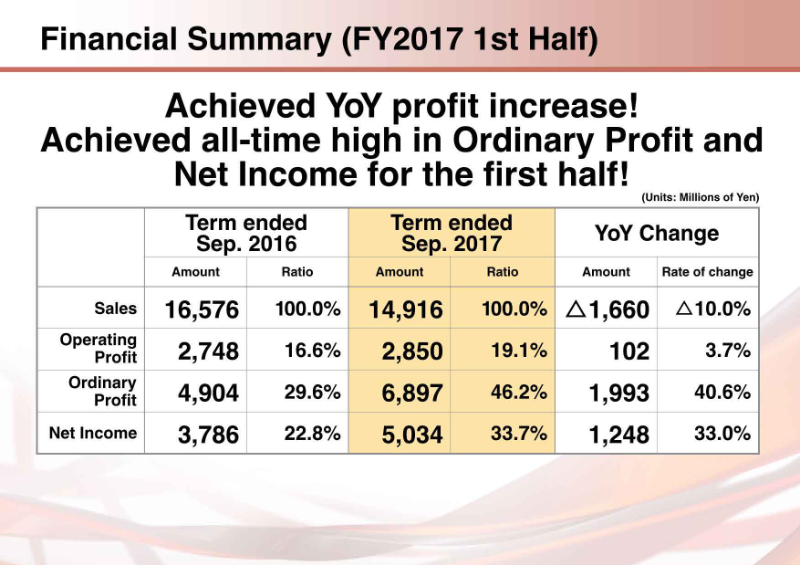

Fiscal Year Ending March 2018: 1st Half Financial Results

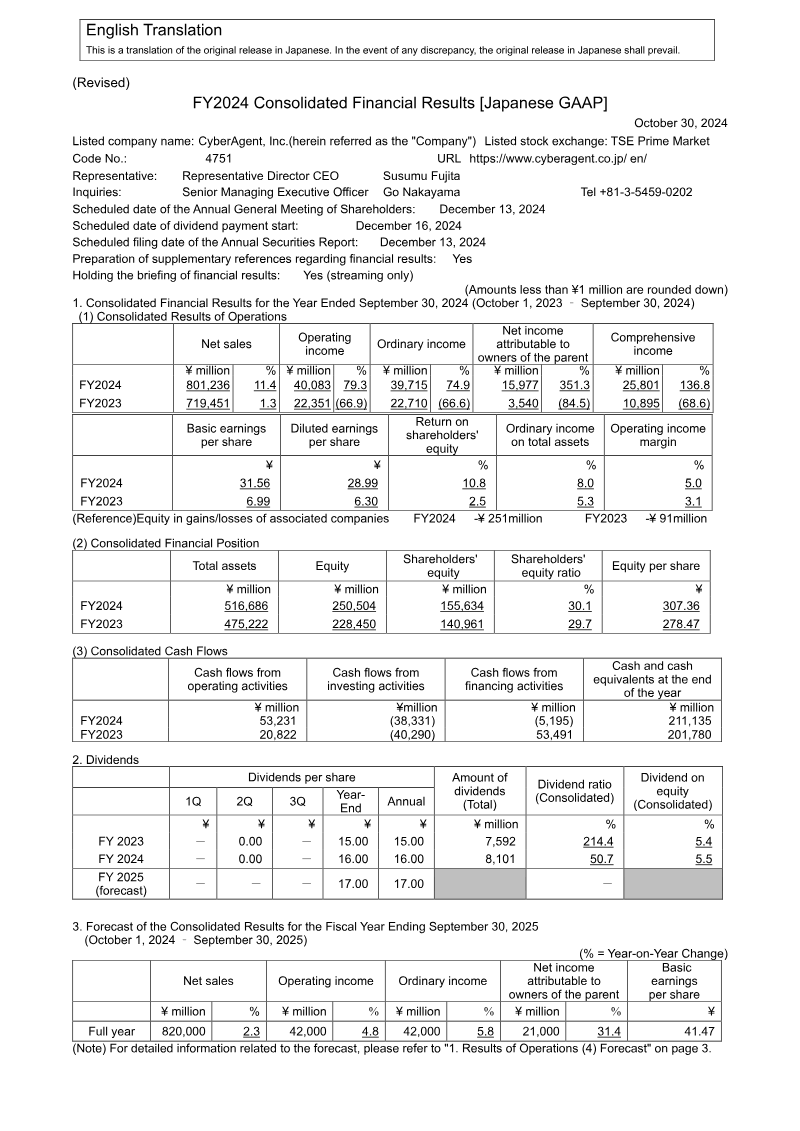

The fiscal year ending March 2018 first‑half results demonstrate a robust upward trajectory for the company, with sales rising 10 % YoY to ¥16.6 billion and operating profit increasing 3.7 % to ¥2.85 billion. Ordinary profit and net income reached record highs, up 40.6 % to ¥6.90 billion and 33.0 % to ¥5.03 billion respectively, reflecting strong performance across entertainment and IP‑licensing segments. Geographically, domestic sales accounted for 74.8 % of total revenue, while overseas sales grew from ¥4.35 billion to ¥5.03 billion, a 15.6 % increase. Growth was most pronounced in Asia (45.9 %) and Europe (25.7 %), with North America showing modest gains of 11.9 %. Unit sales mirrored revenue trends, with overseas units rising 92.9 % and North American units doubling. The company’s portfolio expansion is evident through multiple high‑profile releases, including “Nioh,” “Fire Emblem Warriors,” and “Maji‑Tama × X.I.P. Live.” IP licensing activities generated significant revenue, with new titles on PlayStation 4, Nintendo Switch, and mobile platforms. Strategic collaborations—such as the alliance with HEROZ for AI technology—and cross‑media ventures (film adaptations and themed attractions) underline a diversified growth strategy. Capital allocation remained steady, with FY2017 capital expenditures at ¥8.4 billion and depreciation expenses at ¥6.0 billion, supporting ongoing development and real‑estate investments. Dividend policy continued to increase, with a planned dividend of ¥70 per share for FY2018. Overall, the first‑half performance confirms the company’s trajectory toward its goal of achieving record profits through a strong lineup and expanded IP presence.

Koei Tecmo