Marvelous Inc. announced that its Audit & Supervisory Board will propose a change of accounting auditor at the 29th Annual General Meeting on June 23, 2026. The outgoing auditor, PricewaterhouseCoopers Japan LLC, will complete its term at that meeting; the incoming firm is Crowe Toyo & Co., based in Tokyo, with engagement partners Satoshi Tamakawa and Yuki Ishikawa. The board cited a comprehensive review of audit structure suitability, fee reasonableness, independence, and quality control as the basis for selecting Crowe Toyo & Co. No audit opinions from the past three years were applicable, and the outgoing auditor expressed no objections to the transition. The board confirmed that the change is appropriate.

The notice covers a single Japanese company listed on the TSE Prime Market, focusing solely on the auditor transition for fiscal year 2026. No statistical data or broader industry analysis is provided; the document serves as a formal disclosure to shareholders and regulators. The methodology involves an internal comparative review of audit firms, with the board’s resolution reflecting its assessment that Crowe Toyo & Co. better aligns with Marvelous Inc.’s business scale and audit needs. The announcement ensures compliance with Article 193‑2 of the Financial Instruments and Exchange Act, fulfilling statutory disclosure requirements for auditor changes.

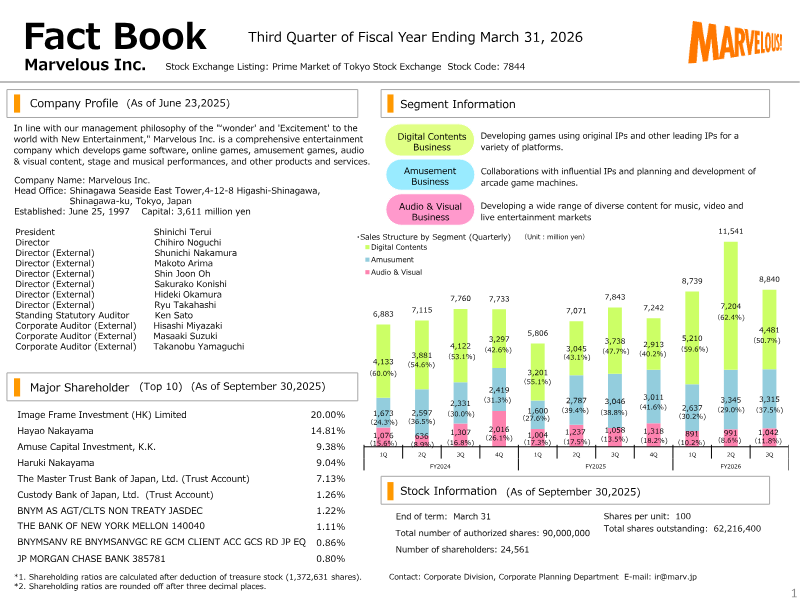

Marvelous · 2026

Marvelous · 2026

Marvelous · 2025

Marvelous · 2025

Marvelous

Marvelous

Marvelous

Marvelous

Marvelous

Marvelous

Marvelous

Capcom · 2026

Capcom Co. · 2026

Capcom · 2026

Sony Group Corporation · 2026

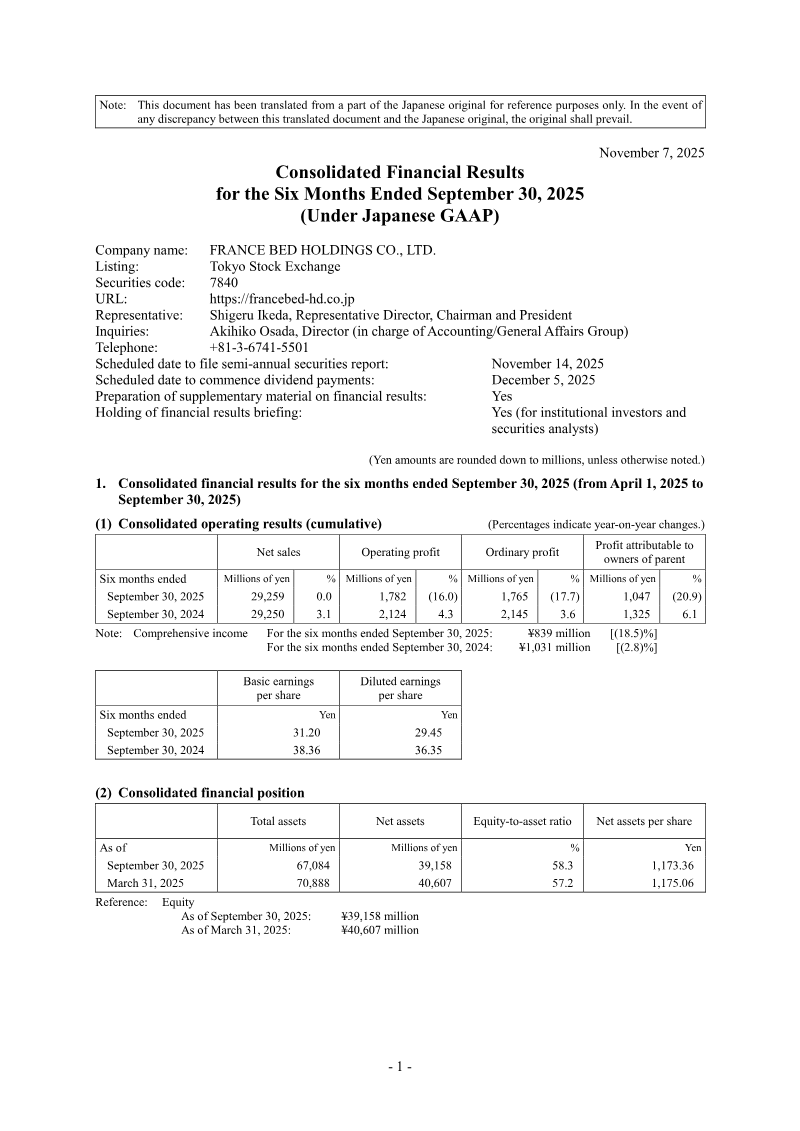

FRANCE BED HOLDINGS CO. · 2026

Square Enix · 2026

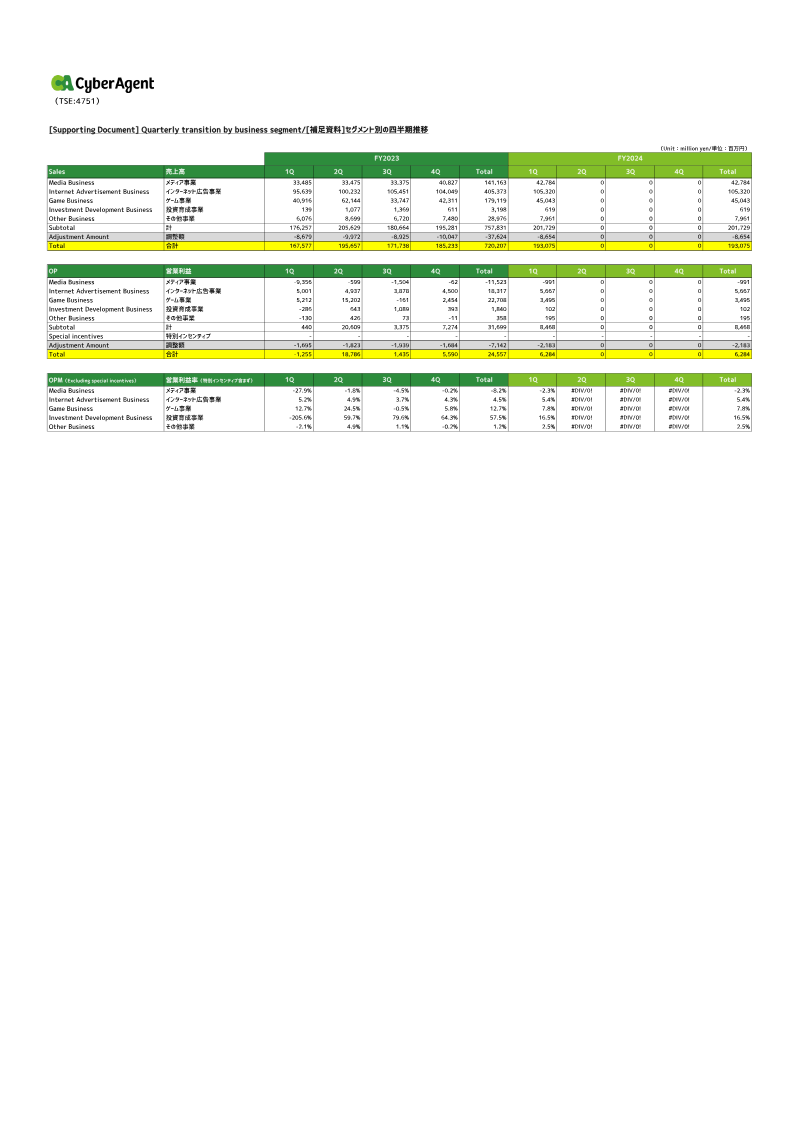

CyberAgent · 2026

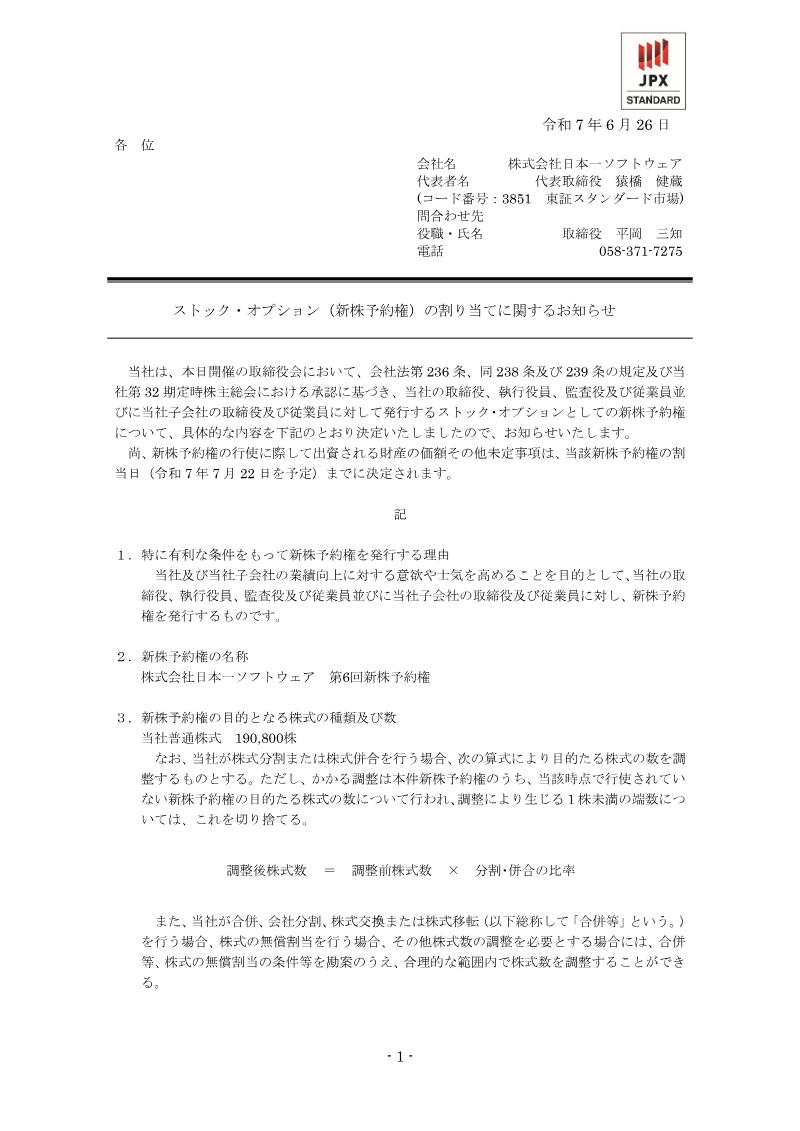

Nippon Ichi Software · 2026

Square Enix · 2026

GungHo Online Entertainment · 2026

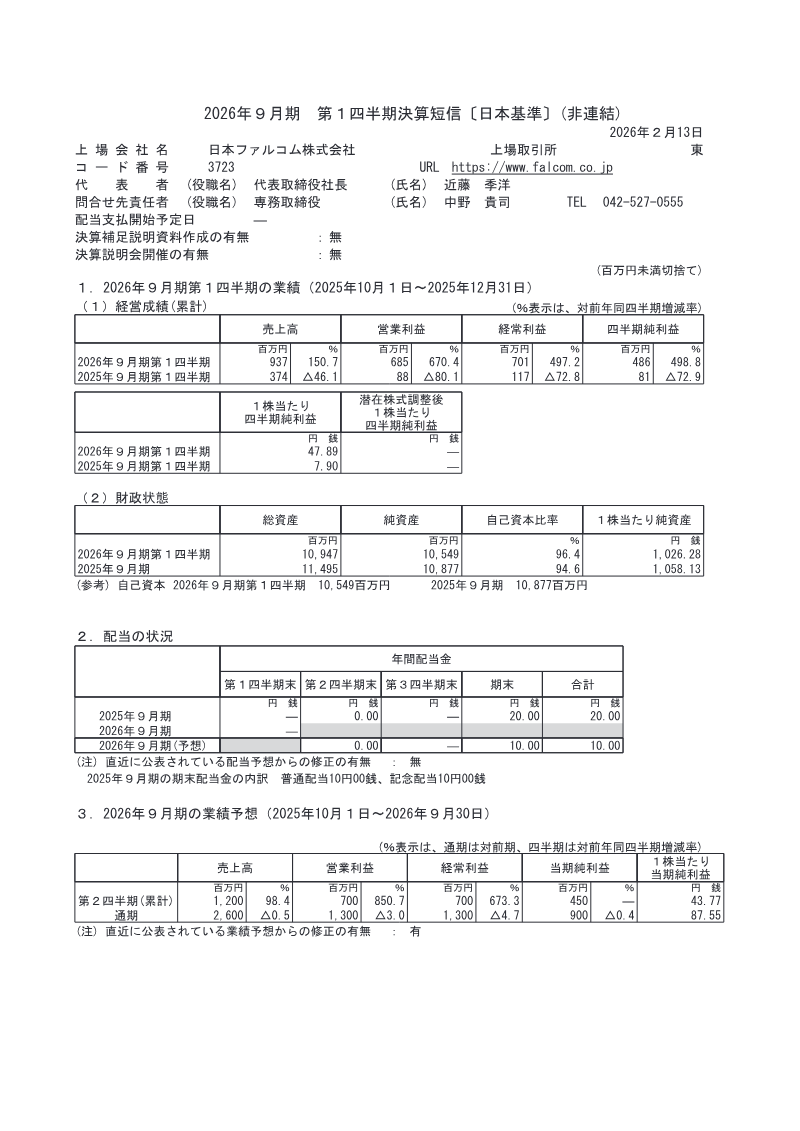

Nihon Falcom Corporation · 2026

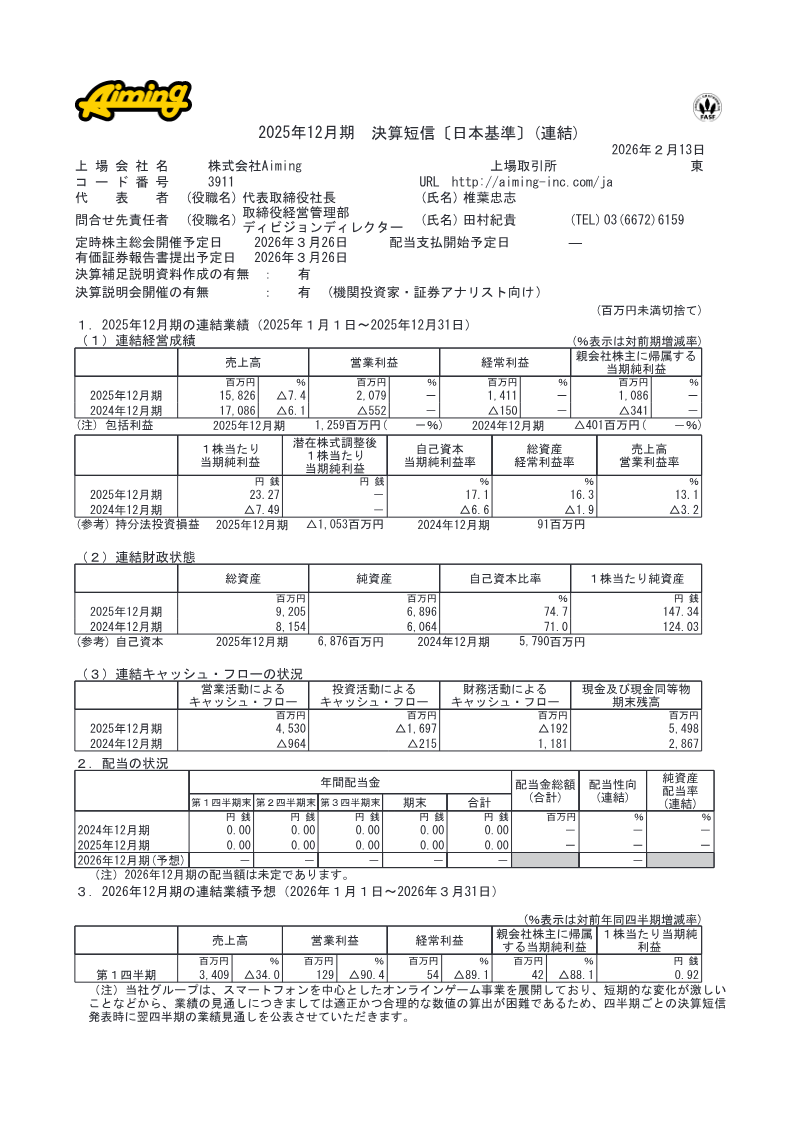

Aiming · 2026