FinancialFRANCE BED HOLDINGS CO.

Consolidated Financial Results: Fiscal Year Ended March 31, 2026

1 May 20268 pages~10 min full read

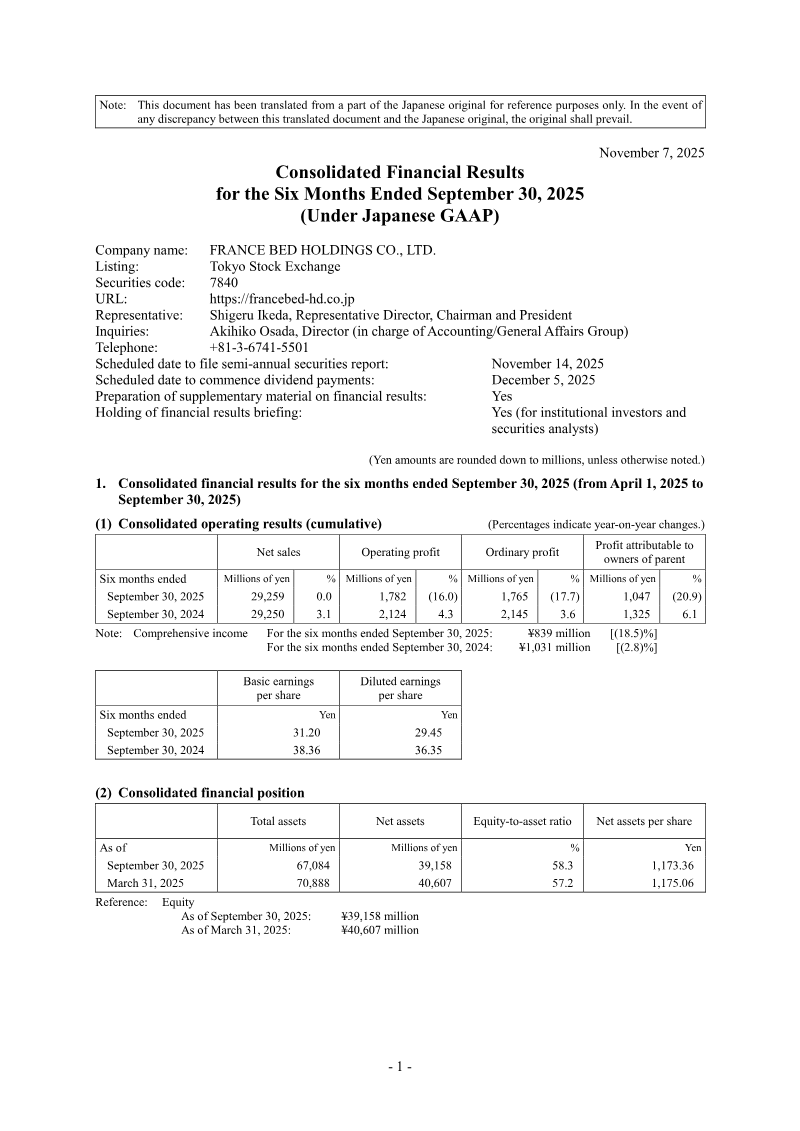

France Bed Holdings reported a 20.9% year-on-year decline in profit attributable to owners of the parent, totaling 1,047 million yen for the six months ending September 30, 2025.

See it on page 1Operating profit for the first half of the fiscal year fell 16.0% to 1,782 million yen, while ordinary profit decreased 17.7% to 1,765 million yen.

See it on page 6Net sales for the first half remained essentially flat at 29,259 million yen compared to the same period in the previous year.

See it on page 1The company maintained its full-year earnings forecast for the fiscal year ending March 31, 2026, projecting 62,300 million yen in net sales and 4,750 million yen in operating profit.

See it on page 2As of September 30, 2025, the company reported total assets of 67,084 million yen and an equity-to-asset ratio of 58.3%.

See it on page 5Cash flows from operating activities provided 2,541 million yen during the first half, supported by ongoing capital allocation toward property, plant, equipment, and treasury share purchases.

See it on page 8Basic earnings per share for the six-month period dropped to 31.20 yen, down from 38.36 yen in the prior year.

See it on page 1France Bed Holdings Co., Ltd. released its consolidated financial results for the six-month period ending September 30, 2025, prepared in accordance with Japanese GAAP. The report details the company’s operating performance, financial position, and cash flow status, while maintaining its previously announced earnings forecasts for the full fiscal year ending March 31, 2026.

During the first half of the fiscal year, the company reported net sales of 29,259 million yen, remaining essentially flat compared to the same period in the previous year. However, profitability metrics experienced a decline, with operating profit falling 16.0% to 1,782 million yen and ordinary profit decreasing 17.7% to 1,765 million yen. Profit attributable to owners of the parent reached 1,047 million yen, representing a 20.9% year-on-year decline. Basic earnings per share for the period were 31.20 yen, down from 38.36 yen in the prior year.

The company’s financial position as of September 30, 2025, shows total assets of 67,084 million yen and net assets of 39,158 million yen, resulting in an equity-to-asset ratio of 58.3%. Cash flows from operating activities provided 2,541 million yen, while investing and financing activities reflected ongoing capital allocation, including the purchase of treasury shares and continued investment in property, plant, and equipment.

Looking ahead to the full fiscal year ending March 31, 2026, the company maintains its forecast of 62,300 million yen in net sales and 4,750 million yen in operating profit. These projections reflect a modest growth expectation of 2.8% in sales and 1.1% in operating profit compared to the previous fiscal year. The company continues to operate under stable accounting policies with no significant changes in the scope of consolidation.