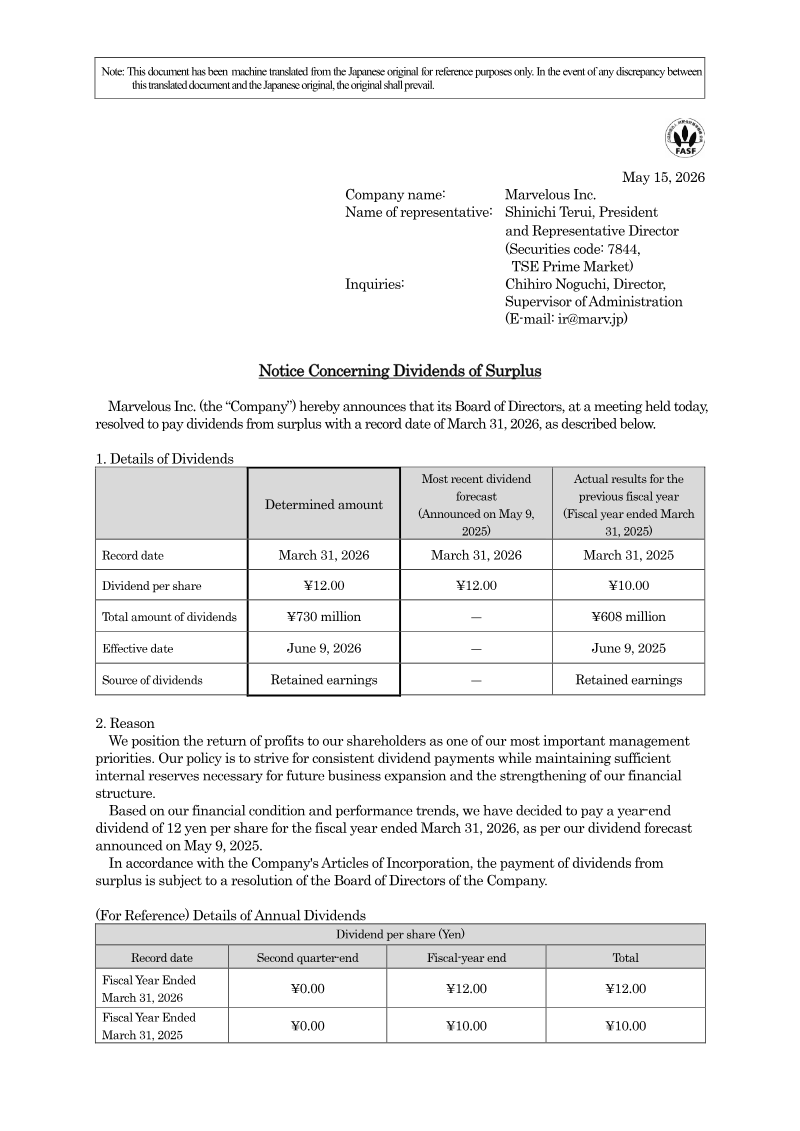

Marvelous Inc., a Tokyo‑listed developer and publisher, announced that its Board of Directors has resolved to pay a year‑end dividend for the fiscal year ending March 31, 2026. The dividend is set at ¥12.00 per share, totaling ¥730 million for all shareholders recorded on March 31, 2026. The payment will be made on June 9, 2026, sourced from retained earnings. This figure matches the company’s previously forecasted dividend announced on May 9, 2025, and represents an increase from the ¥10.00 per share dividend paid for the fiscal year ending March 31, 2025 (¥608 million total). The company emphasizes that dividend distribution is a key management priority, balanced against the need to preserve sufficient internal reserves for future growth and financial stability. The decision follows a Board resolution in accordance with the Articles of Incorporation, which require such approval for dividends from surplus. The announcement covers only Japan‑based operations and pertains to the fiscal year 2026, with no additional geographic or segment details provided. No survey methodology is involved; the information derives from internal financial results and board deliberations.

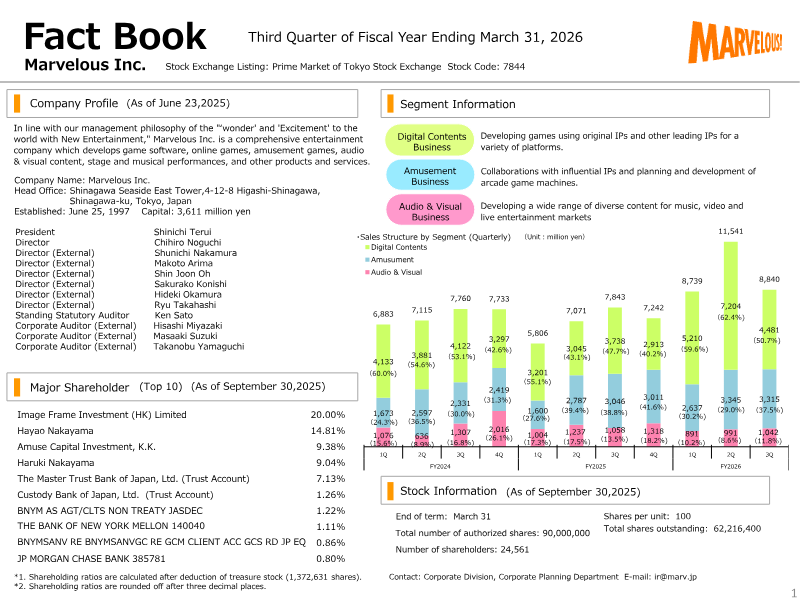

Marvelous · 2026

Marvelous · 2026

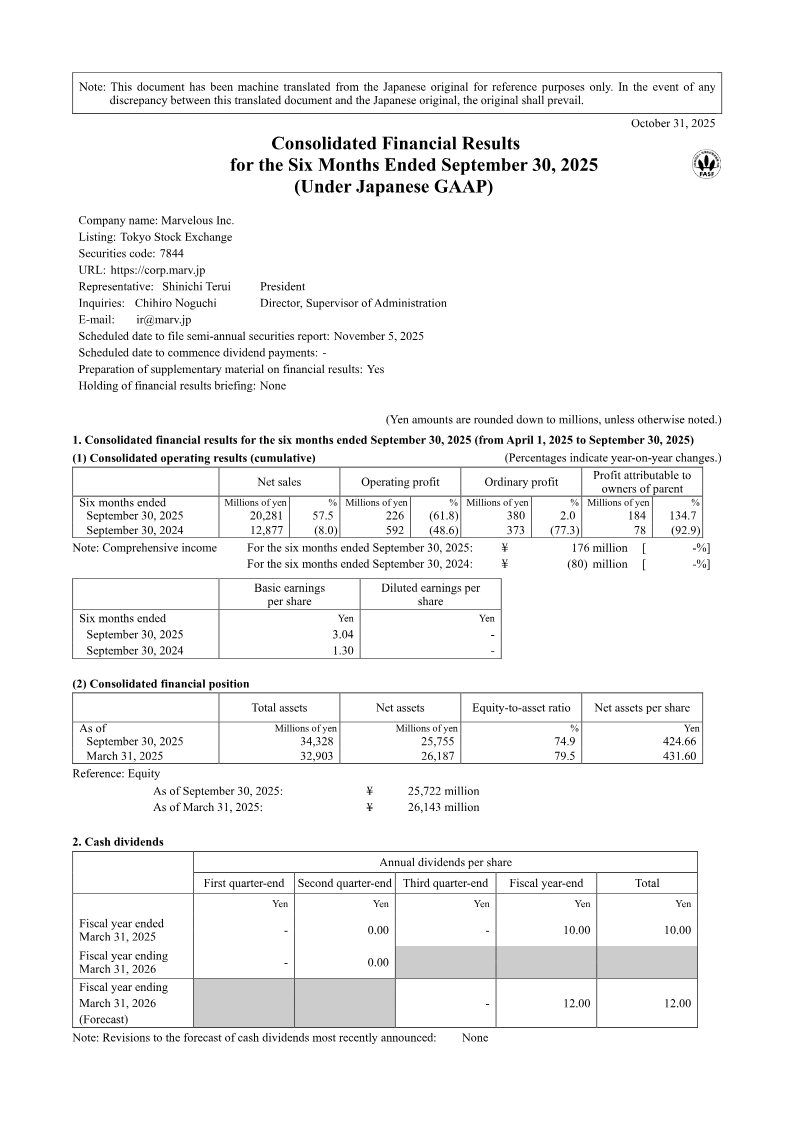

Marvelous · 2025

Marvelous · 2025

Marvelous

Marvelous

Marvelous

Marvelous

Marvelous

Marvelous

Marvelous

Capcom · 2026

Capcom Co. · 2026

Capcom · 2026

Sony Group Corporation · 2026

FRANCE BED HOLDINGS CO. · 2026

Square Enix · 2026

CyberAgent · 2026

Nippon Ichi Software · 2026

Square Enix · 2026

GungHo Online Entertainment · 2026

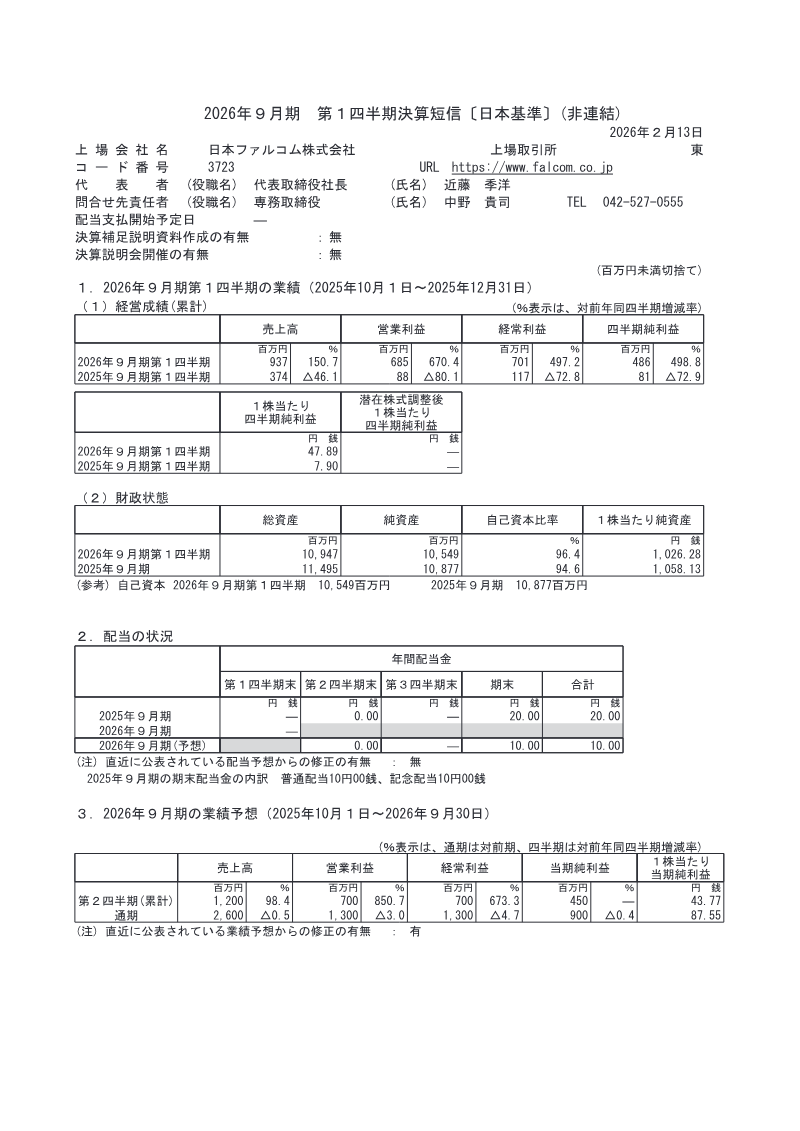

Nihon Falcom Corporation · 2026

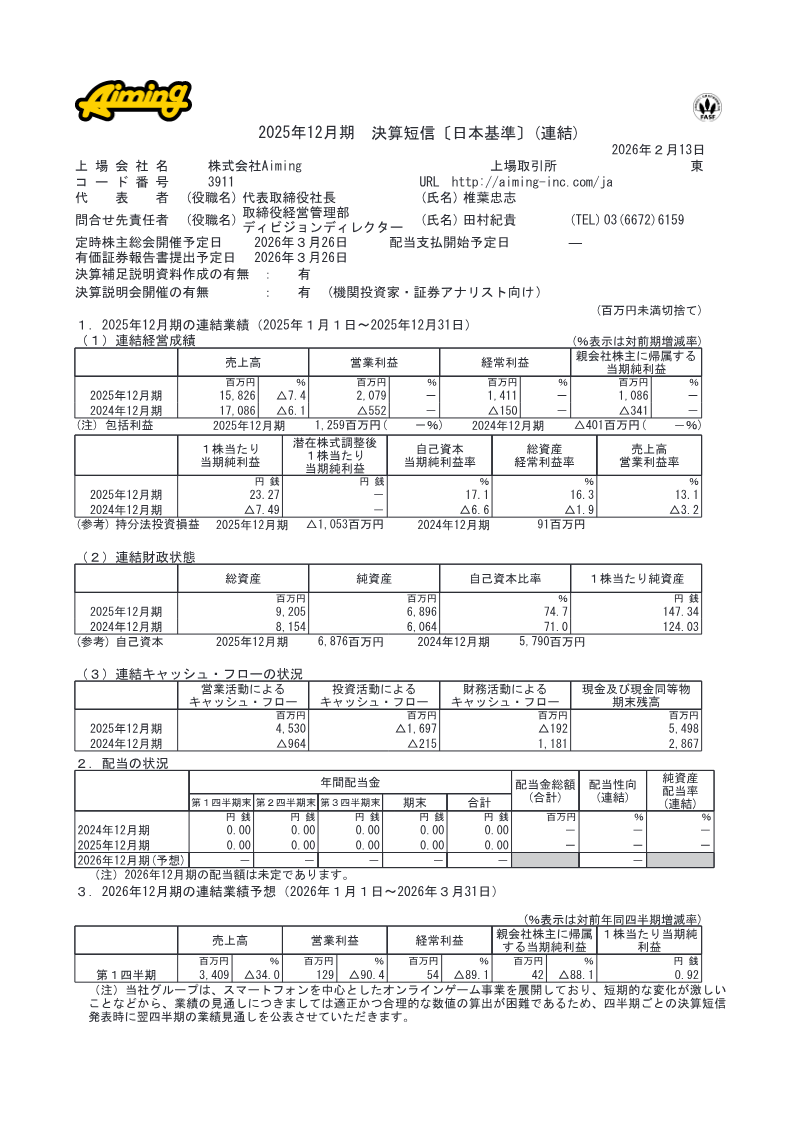

Aiming · 2026