FinancialNihon Falcom Corporation

Nihon Falcom Q1 FY2026 Financial Results (Japanese GAAP, Non-Consolidated)

13 Feb 20268 pages~5 min full read

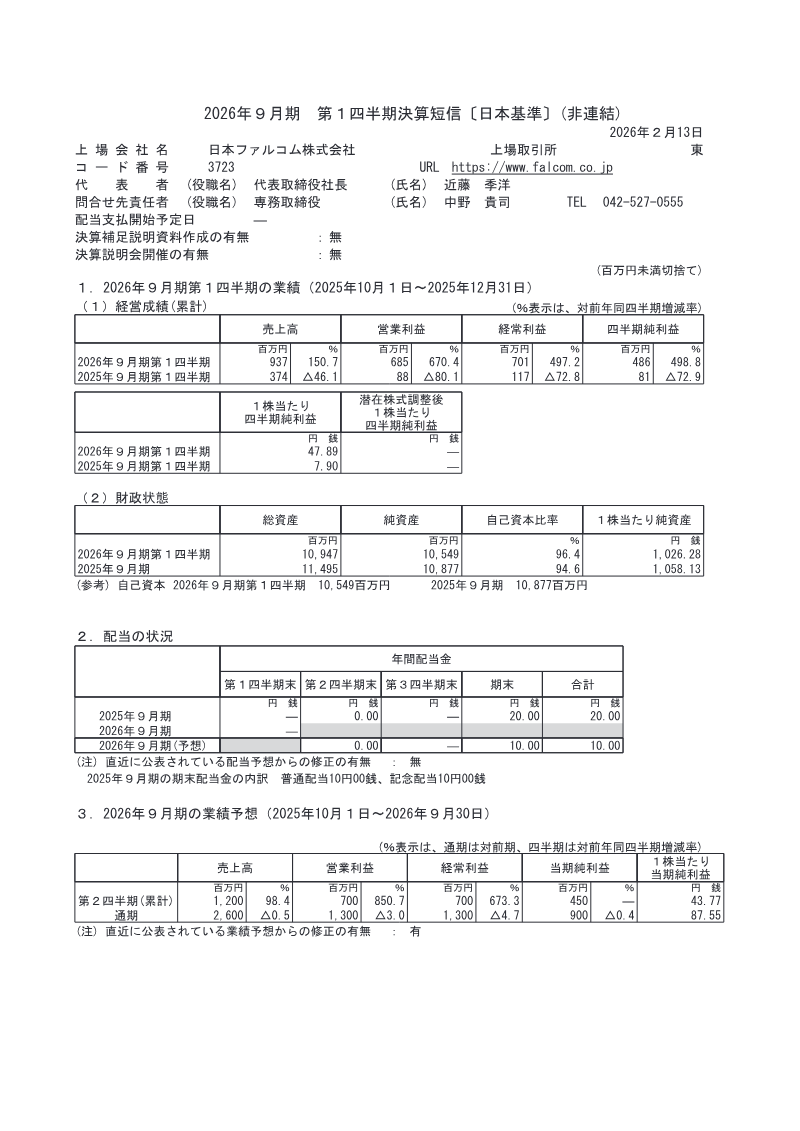

Nihon Falcom reported a 150.7% year-over-year increase in Q1 FY2026 net sales to 937 million yen, with operating income surging 670.4% to 685 million yen.

See it on page 7The licensing division drove the majority of revenue, generating 888 million yen—a 218.3% increase—largely due to the global multi-platform rollout of 'The Legend of Heroes: Trails in the Sky the 1st'.

See it on page 4Domestic product sales declined by 47.6% to 49 million yen, reflecting a strategic shift toward development cycles for upcoming titles.

See it on page 4Management maintained the full-year net sales forecast at 2.6 billion yen, citing caution regarding the market reception of future projects like 'Kyoto Xanadu' and 'Trails in the Sky the 2nd'.

See it on page 5The company maintains a strong financial position with a 96.4% equity ratio, despite a slight decrease in total assets to 10.9 billion yen following a 608 million yen share buyback.

See it on page 6Revenue growth is increasingly tied to international markets and multi-platform availability across Nintendo Switch, PlayStation 5, and Steam.

See it on page 4Nihon Falcom’s financial results for the first quarter of the fiscal year ending September 2026 reveal significant year-over-year growth driven by strong international licensing performance. For the three-month period ending December 31, 2025, net sales reached 937 million yen, a 150.7% increase over the previous year. Profitability saw even sharper gains, with operating income rising 670.4% to 685 million yen and net income increasing 498.8% to 486 million yen.

The licensing division served as the primary growth engine, generating 888 million yen in sales, a 218.3% increase. This surge was fueled by the global rollout of The Legend of Heroes: Trails in the Sky the 1st across multiple platforms, alongside continued international sales of the Trails and Ys series. Conversely, the product division, which handles direct domestic sales, saw revenue decline by 47.6% to 49 million yen, reflecting a period focused on development and upcoming releases.

Geographically, the results highlight a heavy reliance on global markets and multi-platform availability, including Nintendo Switch, PlayStation 5, and Steam. Looking ahead, the company has upwardly revised its mid-term forecasts due to the steady performance of its flagship titles. However, full-year forecasts remain unchanged at 2.6 billion yen in net sales, as management remains cautious regarding the timing and market reception of upcoming projects like Kyoto Xanadu and the worldwide simultaneous release of Trails in the Sky the 2nd.

The financial position remains stable with a high equity ratio of 96.4%. Total assets decreased slightly to 10.9 billion yen, primarily due to a 608 million yen share buyback and dividend payments. The company continues to focus on its single segment of game development and licensing, leveraging its established intellectual properties to maintain high profit margins.