FinancialSega Sammy Holdings

Q3 Results Presentation: Fiscal Year Ending March 2026

53 pages~74 min full read

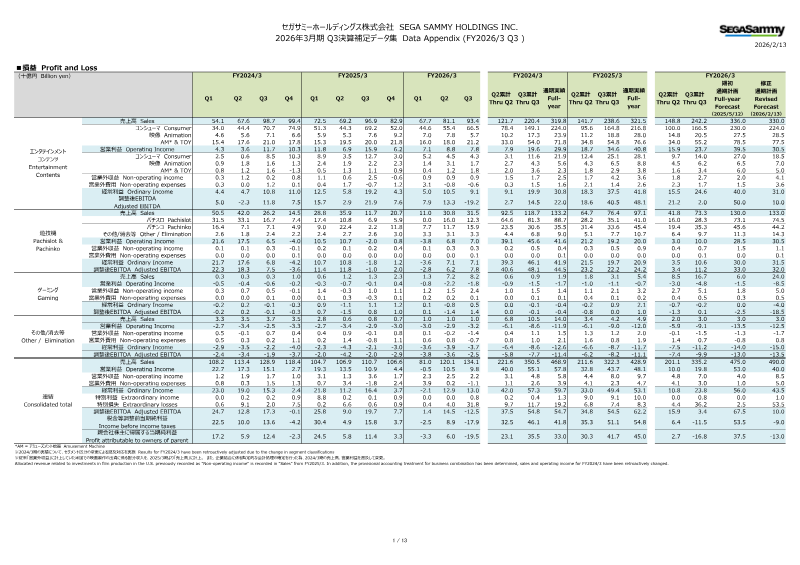

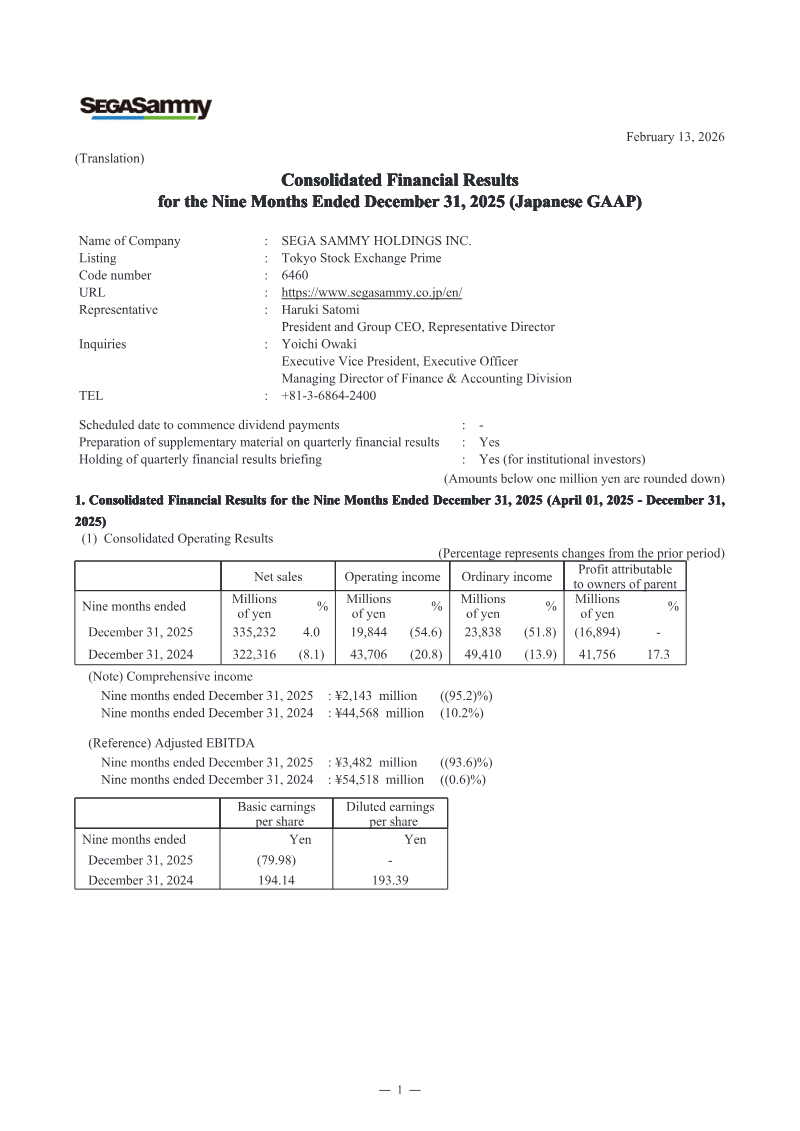

Sega Sammy Holdings faces a pivotal fiscal turning point, projecting its first net loss in eleven years at 13 billion yen for the fiscal year ending March 2026. This downturn is primarily driven by 46.3 billion yen in impairment losses related to the acquisitions of Rovio and Stakelogic, which failed to meet performance expectations amid market volatility and regulatory shifts. Consequently, the company is suspending large-scale mergers and acquisitions to prioritize capital efficiency, initiating a 20 billion yen share buyback, and pivoting toward a more disciplined, data-driven operational model.

The company’s performance remains bifurcated across its diverse business segments. The Pachislot and Pachinko division continues to serve as a financial anchor, exceeding profit forecasts through the successful deployment of flagship titles like Smart Pachislot Tokyo Revengers and e Hokuto No Ken 11. Conversely, the Consumer segment has struggled significantly, hampered by the underperformance of new full-game releases and free-to-play titles, including Sonic Rumble and Football Manager 26. While the Animation and AM & Toy segments demonstrate steady growth and the Transmedia business shows promise in licensing, these gains have been insufficient to offset the broader digital and consumer-facing setbacks.

Moving forward, the strategic focus shifts from aggressive expansion to the optimization of core intellectual properties, such as Sonic and Angry Birds. Management is prioritizing the development of a repeatable system for hit production and enhanced community engagement to stabilize long-term profitability. By reallocating resources toward internal development efficiency and strengthening its B2B omnichannel strategy, the company aims to navigate current market challenges while maintaining its regulatory obligations across international gaming jurisdictions. This transition marks a deliberate move away from acquisition-led growth toward a model centered on sustainable, high-quality content delivery.

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2024

Sega Sammy Holdings · 2024

Sega Sammy Holdings

Sega Sammy Holdings

Sega Sammy Holdings

Sony Group Corporation · 2026

Bandai Namco · 2026

InvestGame · 2025

Square Enix · 2025

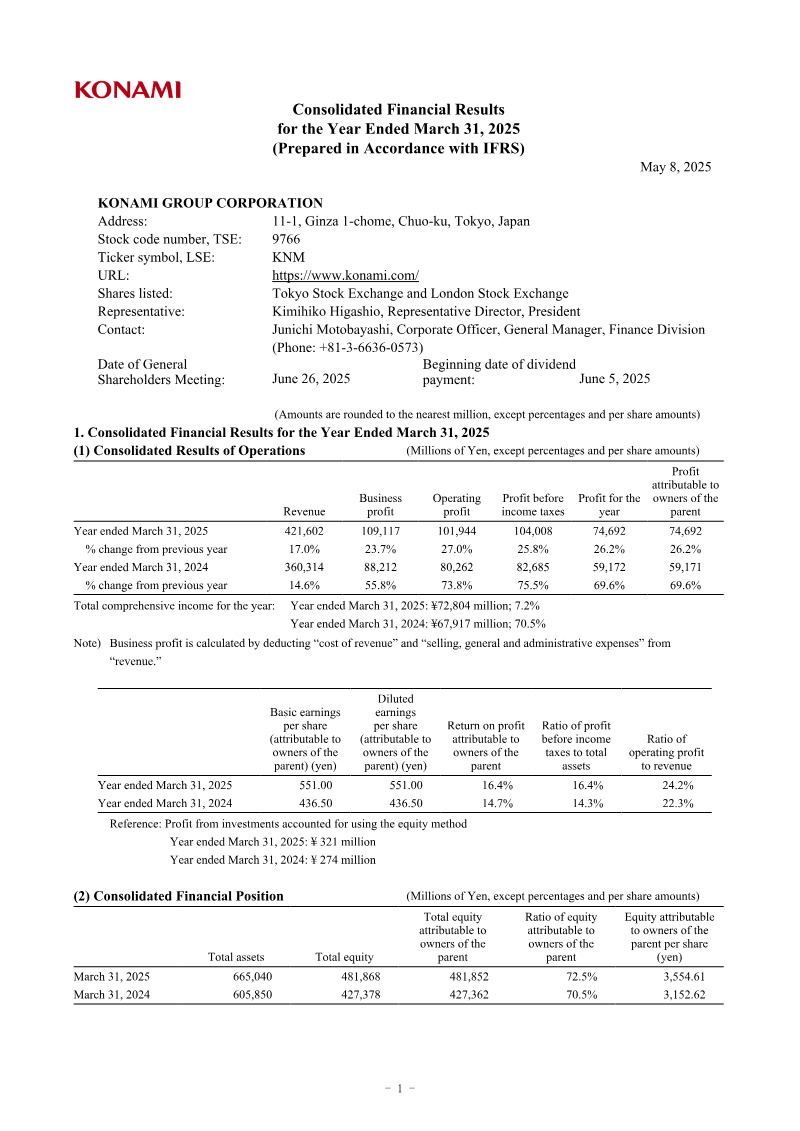

Konami · 2025

Nintendo · 2024

Bandai Namco · 2022

Bandai Namco · 2021

GREE · 2017

Bandai Namco · 2017

GREE Inc. · 2016

Bandai Namco · 2014