FinancialSega Sammy Holdings

Full-Year Results for the Fiscal Year Ended March 2026: Major Questions in Results Briefing

6 pages~15 min full read

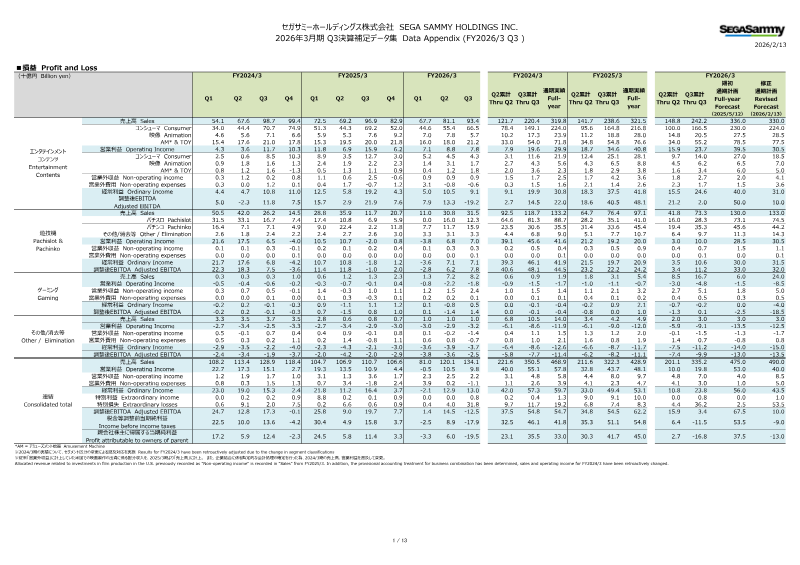

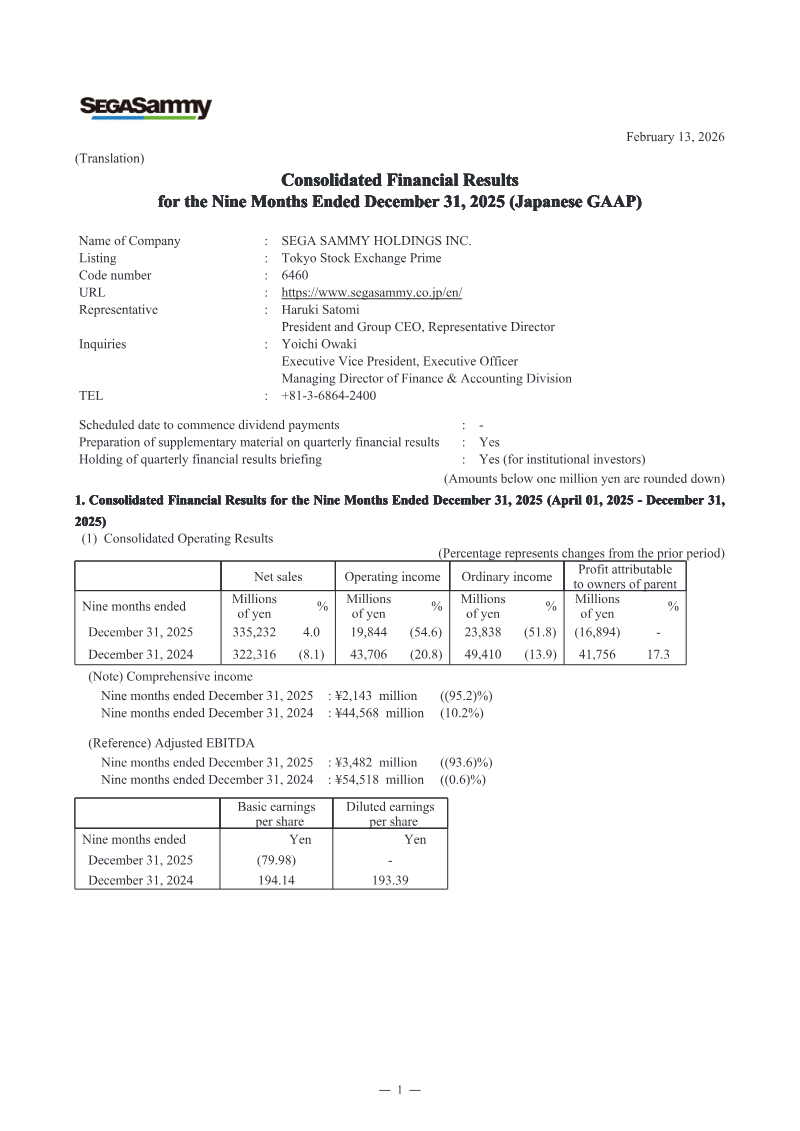

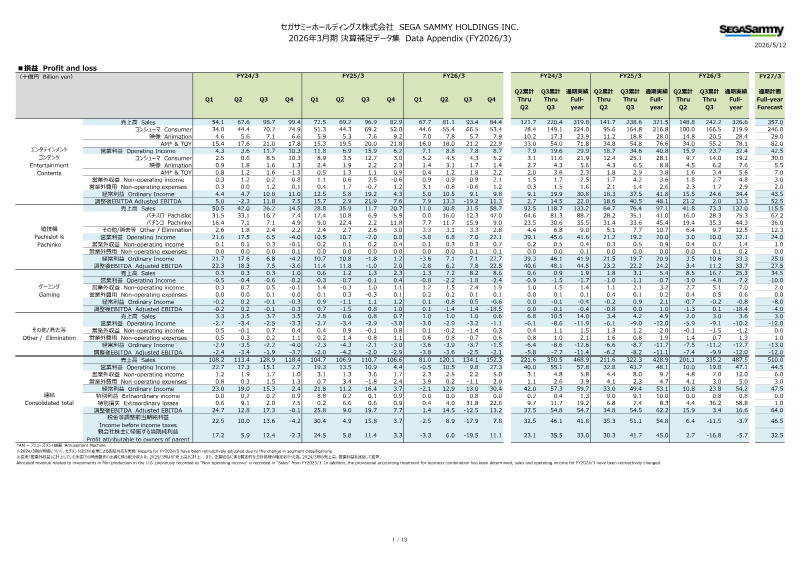

The briefing clarified Sega Sammy Holdings’ fiscal‑year 2026 performance and forward strategy amid evolving market conditions. Social factors such as AI demand and Middle East tensions were deemed manageable, with a 1.5 billion yen impact already factored into the Pachislot & Pachinko forecast; no material risks from Middle East events were anticipated. M&A activity will remain limited to small‑scale transactions, while the company continues to strengthen its content pipeline by releasing four major IP titles in FY2027/3, scheduled for the second half of the year to maximize full‑price sales. The firm highlighted a shift toward data‑driven pricing and promotion, leveraging AI to optimize global KPIs across Europe, North America, South America, Southeast Asia, and Africa. Repeat sales initiatives will be supported by anniversary events for Sonic (35th) and Persona (30th), as well as cross‑media projects such as the Sonic movie and transmedia expansions for Like a Dragon.

In gaming, the company expects FY2027/3 to be the bottom of losses for its Stakelogic unit, with a projected operating loss of 1.6 billion yen; structural reforms aim to reverse this trend by FY2028/3. The Gaming Business’s profitable segments—Gaming machine sales, GAN B2C, and PARADISE SEGASAMMY—will continue to drive earnings, while GAN B2B and Stakelogic receive targeted efficiency measures. PARADISE SEGASAMMY’s smart table development is positioned to reduce dealer training and operating costs, potentially expanding into international casinos. Overall, the company projects increased content production expenses in FY2028/3 due to a larger title slate and higher personnel costs, but anticipates corresponding profit growth from the expanded Full Game portfolio.

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2024

Sega Sammy Holdings · 2024

Sega Sammy Holdings

Sega Sammy Holdings

Sega Sammy Holdings

Sony Group Corporation · 2026

Bandai Namco · 2026

InvestGame · 2025

Square Enix · 2025

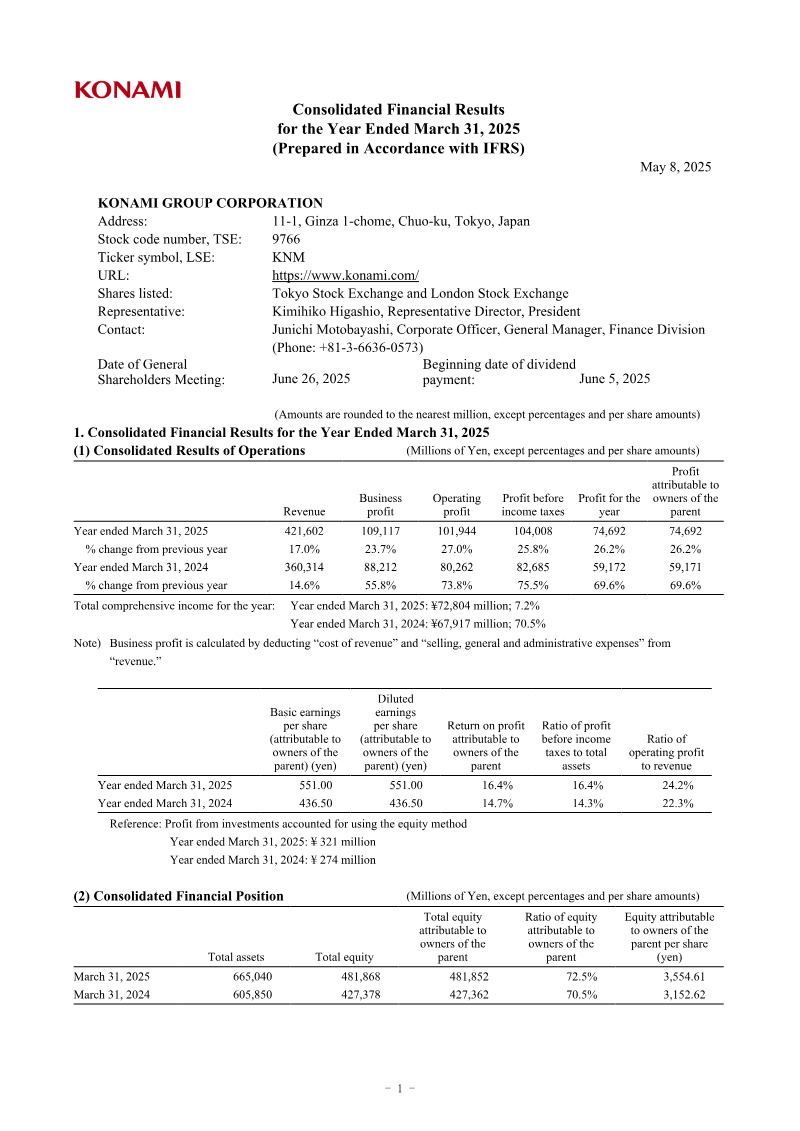

Konami · 2025

Nintendo · 2024

Bandai Namco · 2022

Bandai Namco · 2021

GREE · 2017

Bandai Namco · 2017

GREE Inc. · 2016

Bandai Namco · 2014