FinancialSega Sammy Holdings

Consolidated Financial Results: Fiscal Year Ended March 31, 2026

24 pages~51 min full read

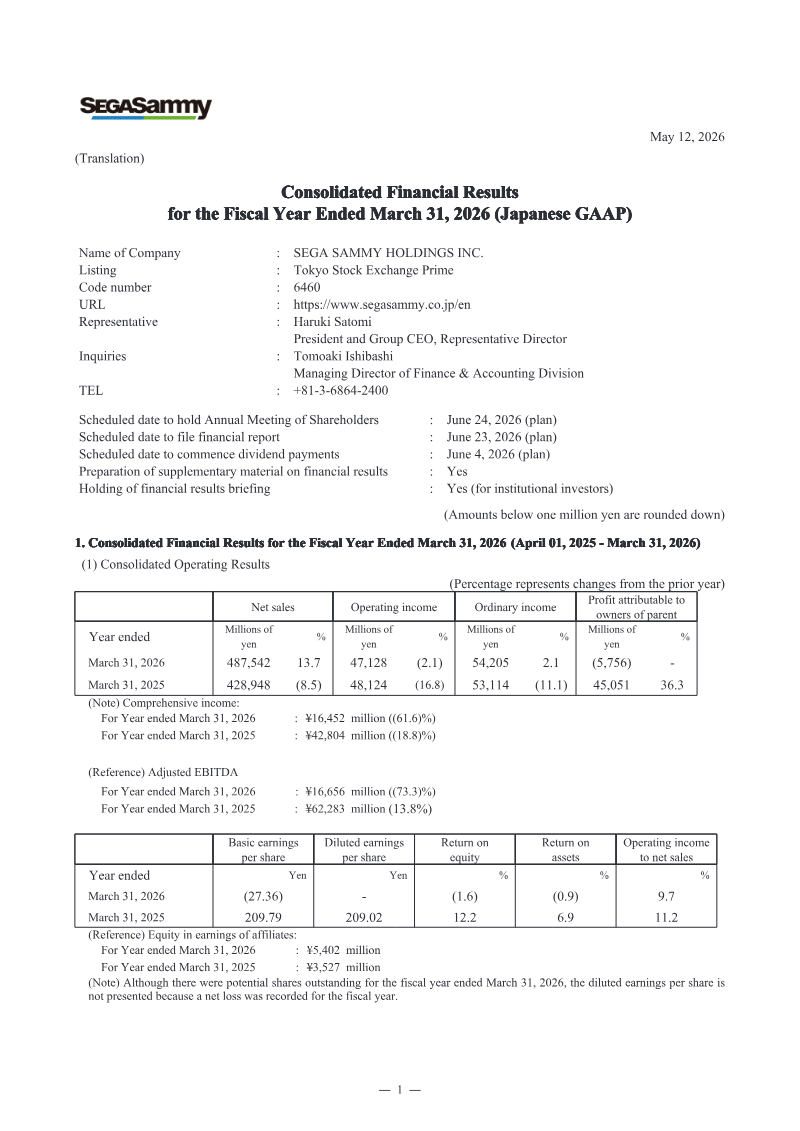

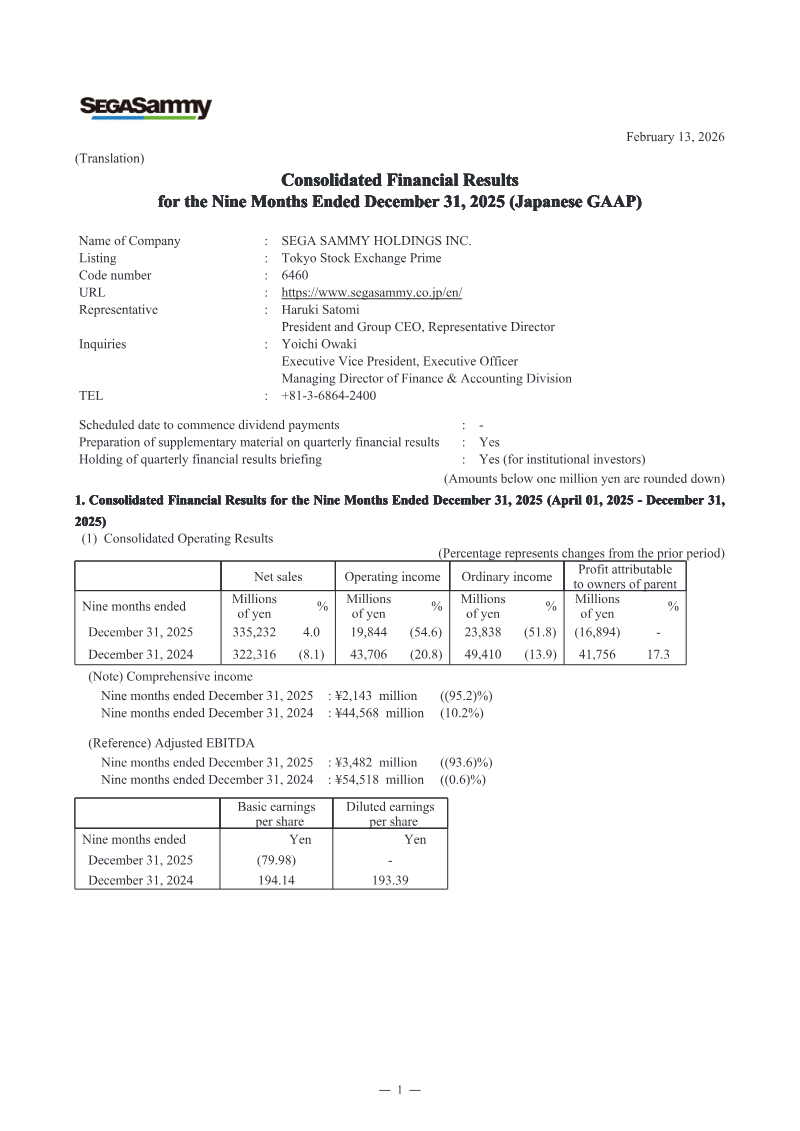

Sega Sammy’s fiscal year ending March 31, 2026 delivered a mixed financial picture. Net sales rose 13.7 % to ¥487,542 million, driven largely by third‑party and U.S. film production income, yet operating income slipped 2.1 % to ¥47,128 million and the group recorded a net loss of ¥5.756 billion attributable to owners of parent. Adjusted EBITDA collapsed 73.3 % to ¥16,656 million, largely due to goodwill and intangible asset impairments from the acquisitions of Rovio, Stakelogic and GAN. Despite these losses, shareholder returns remained robust with ¥55 per share in dividends and a ¥20 billion share buy‑back, totaling approximately ¥31.4 billion in returns.

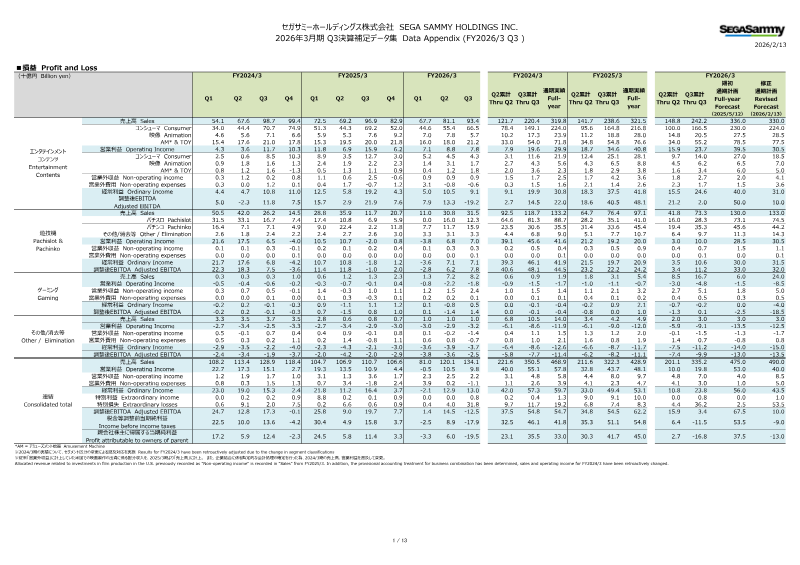

The Gaming segment experienced a sharp rebound in sales, with net sales up 35.9 % to ¥132.2 billion, largely from a 36 % increase in Pachislot & Pachinko and a 364 % surge in third‑party gaming sales. Ordinary income climbed 58.8 % to ¥33.3 billion, and adjusted EBITDA grew 38.8 % to ¥33.7 billion; however, the segment posted a substantial operating loss of ¥19.4 billion. Total assets fell by ¥17.4 billion, liabilities rose by ¥9.2 billion, and net assets declined by ¥26.6 billion, with cash and equivalents dropping to ¥154 million.

Capital efficiency measures included a ¥20 billion treasury stock cancellation and significant goodwill write‑downs—¥31.99 billion on Rovio goodwill and ¥18.05 billion on Stakelogic assets—resulting in a total goodwill write‑down of ¥28.71 billion. Net assets per share fell from ¥1,782.73 to ¥1,750.15, and basic earnings per share swung from a profit of ¥209.79 to a loss of ¥27.36, with no diluted EPS reported due to the net loss.

Looking ahead, management projects a 4.6 % revenue increase for FY 2027 but anticipates a 5.6 % decline in operating income, while maintaining its dividend policy. The company’s financial trajectory reflects a transition from growth‑driven sales expansion to a focus on restructuring and capital efficiency amid significant impairment losses.

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2026

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2025

Sega Sammy Holdings · 2024

Sega Sammy Holdings · 2024

Sega Sammy Holdings

Sega Sammy Holdings

Sega Sammy Holdings

Sony Group Corporation · 2026

Bandai Namco · 2026

InvestGame · 2025

Square Enix · 2025

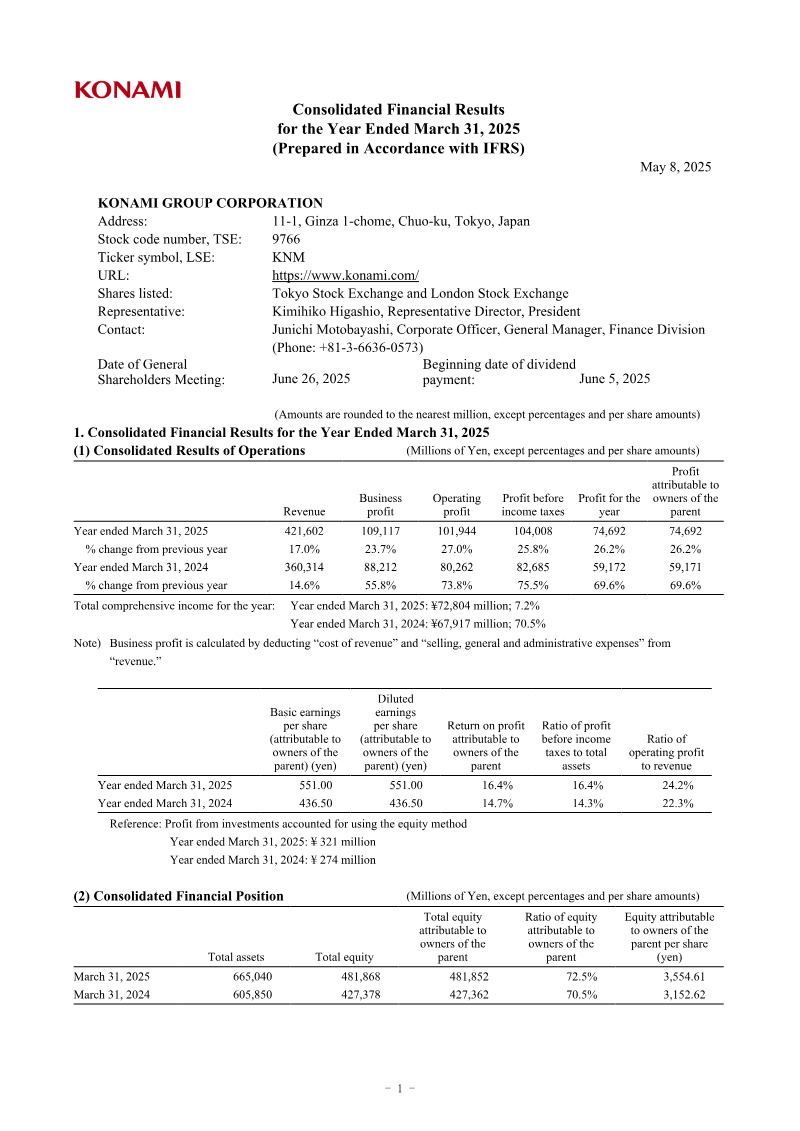

Konami · 2025

Nintendo · 2024

Bandai Namco · 2022

Bandai Namco · 2021

GREE · 2017

Bandai Namco · 2017

GREE Inc. · 2016

Bandai Namco · 2014