Bilan du Marché Français: 2025

39 pages~77 min full read

The French video game market demonstrated significant resilience in 2025, generating €5.856 billion in total revenue, a 2.9% increase over the previous year. This performance marks the second-highest in the industry’s history, solidifying its position as a cornerstone of the national cultural economy. Growth was primarily fueled by a rebound in console hardware sales and a record-breaking 11% surge in the mobile sector, which reached €1.792 billion. The market maintains a balanced ecosystem, with consoles commanding a 44% share, followed by mobile at 31% and PC gaming at 26%.

Software remains the primary revenue driver, accounting for over two-thirds of the total market. While physical game sales faced a double-digit decline, this was effectively mitigated by the expansion of digital content, including microtransactions and downloadable content. Electronic Arts emerged as the leading publisher across console and PC platforms, while the mobile landscape remains almost entirely dominated by free-to-play models, which now represent 94% of mobile revenue.

The industry’s reach expanded to 40.2 million players, characterized by a maturing demographic where adults comprise 88% of the base. High engagement levels persist, with 76% of players gaming on a weekly basis and a growing trend toward cross-platform usage. Alongside this growth, there is a heightened emphasis on responsible gaming. Parental involvement has reached new heights, with 67% of parents actively monitoring gaming habits through PEGI classifications and standardized parental control tools. This commitment to safety, supported by organizations like the SELL and events such as Paris Games Week, ensures that the industry continues to thrive as a mature, socially responsible, and culturally significant sector within France.

SELL – Syndicat des Éditeurs de Logiciels de Loisirs · 2025

SELL – Syndicat des Éditeurs de Logiciels de Loisirs · 2025

SELL – Syndicat des Éditeurs de Logiciels de Loisirs · 2023

SELL – Syndicat des Éditeurs de Logiciels de Loisirs

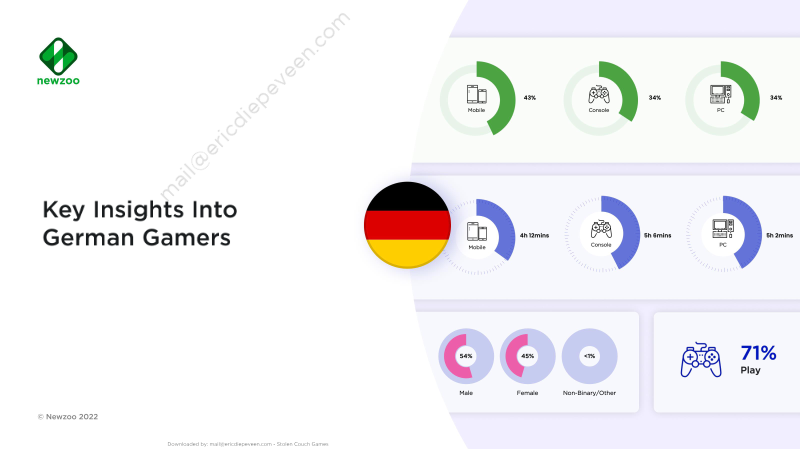

Newzoo · 2022

IIDEA – Italian Interactive Digital Entertainment Association

Newzoo · 2025

GameRefinery · 2022

Bandai Namco · 2019

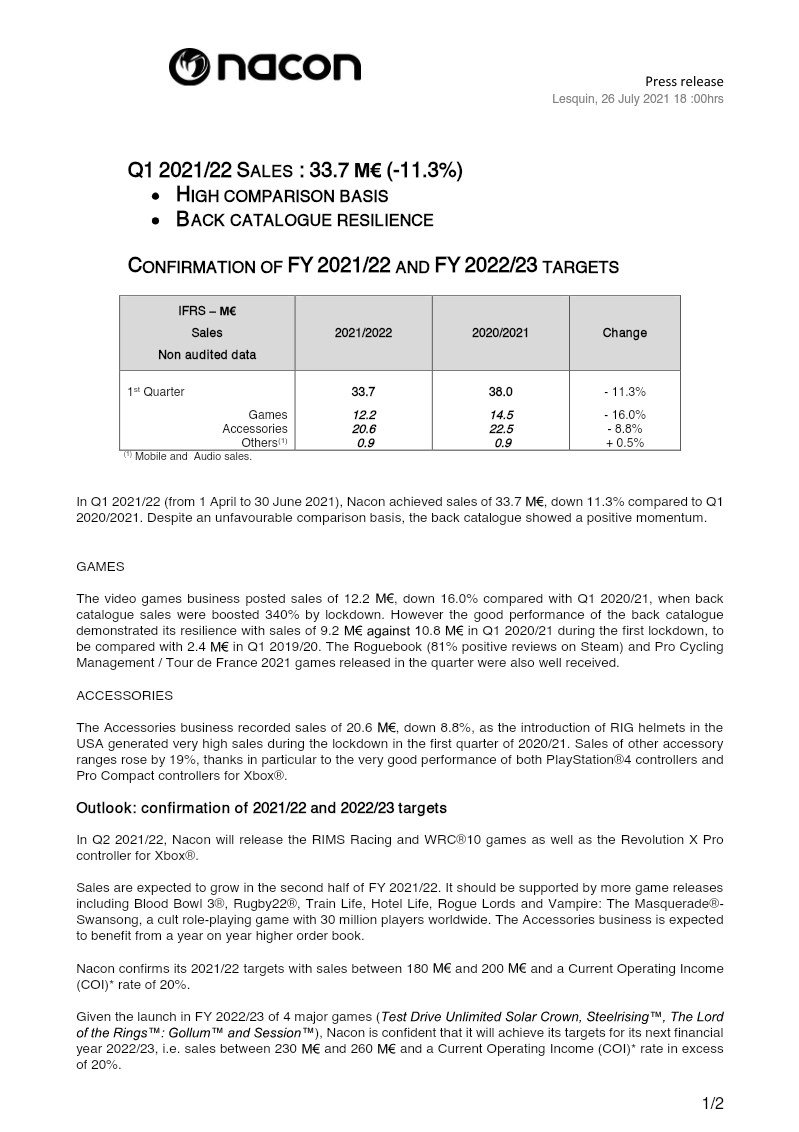

Nacon

GeoPoll

Lumikai

Ubisoft · 2026

Niko Partners · 2026

Bryter · 2026

GameAnalytics · 2026