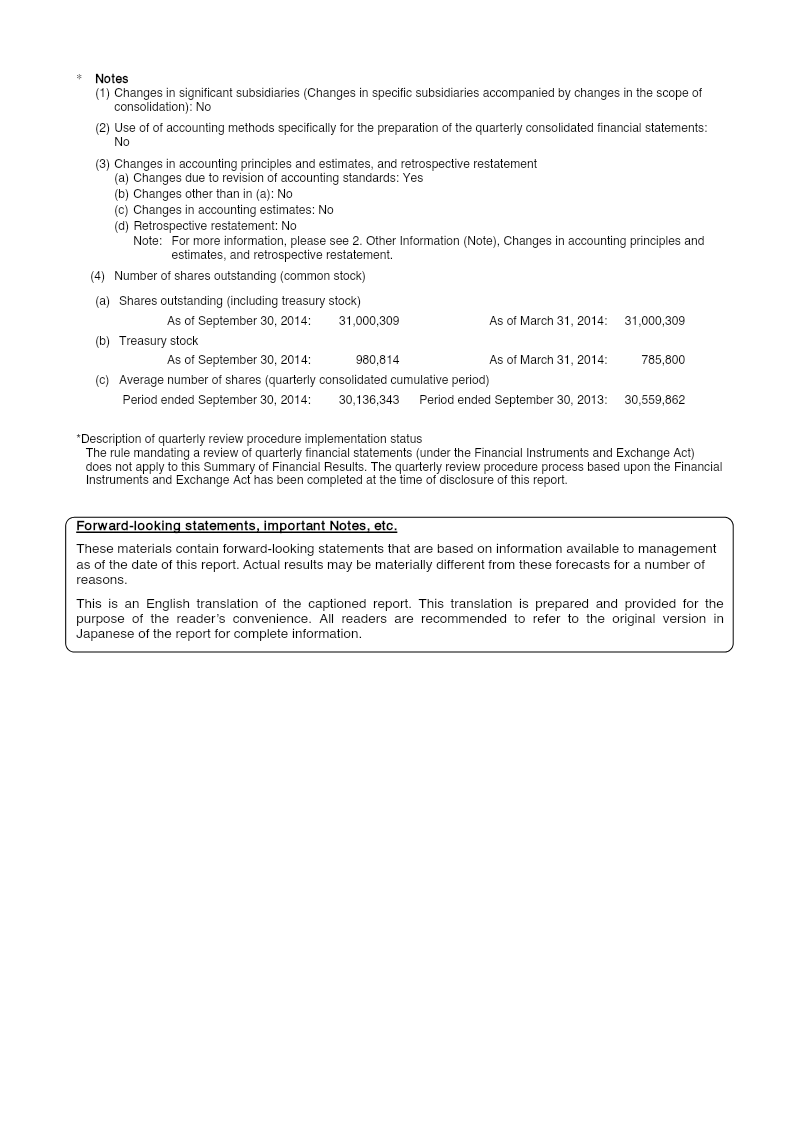

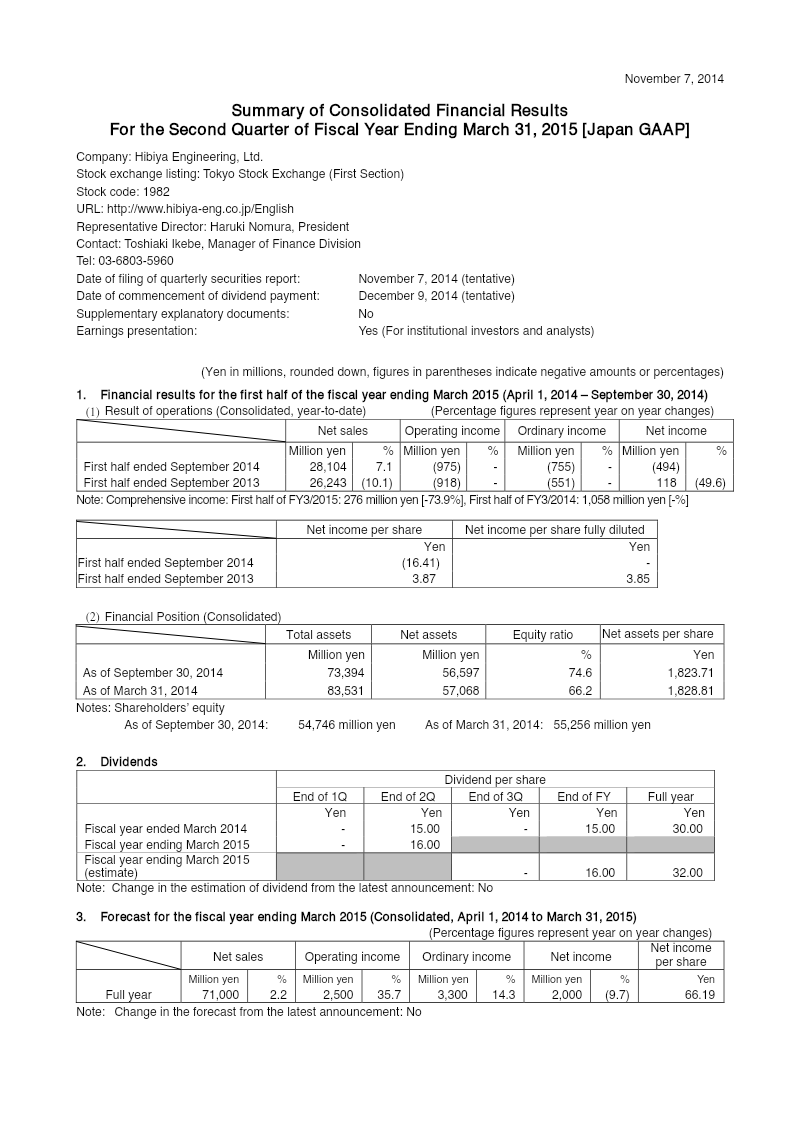

Japan

Report

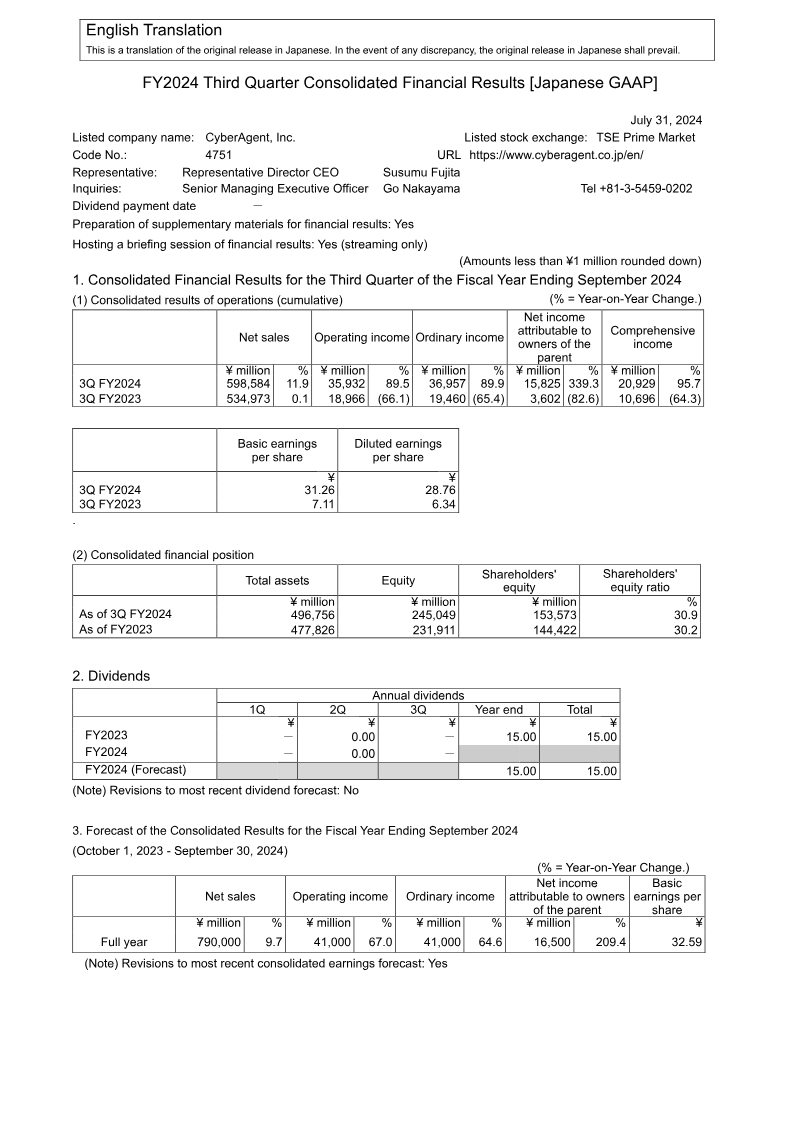

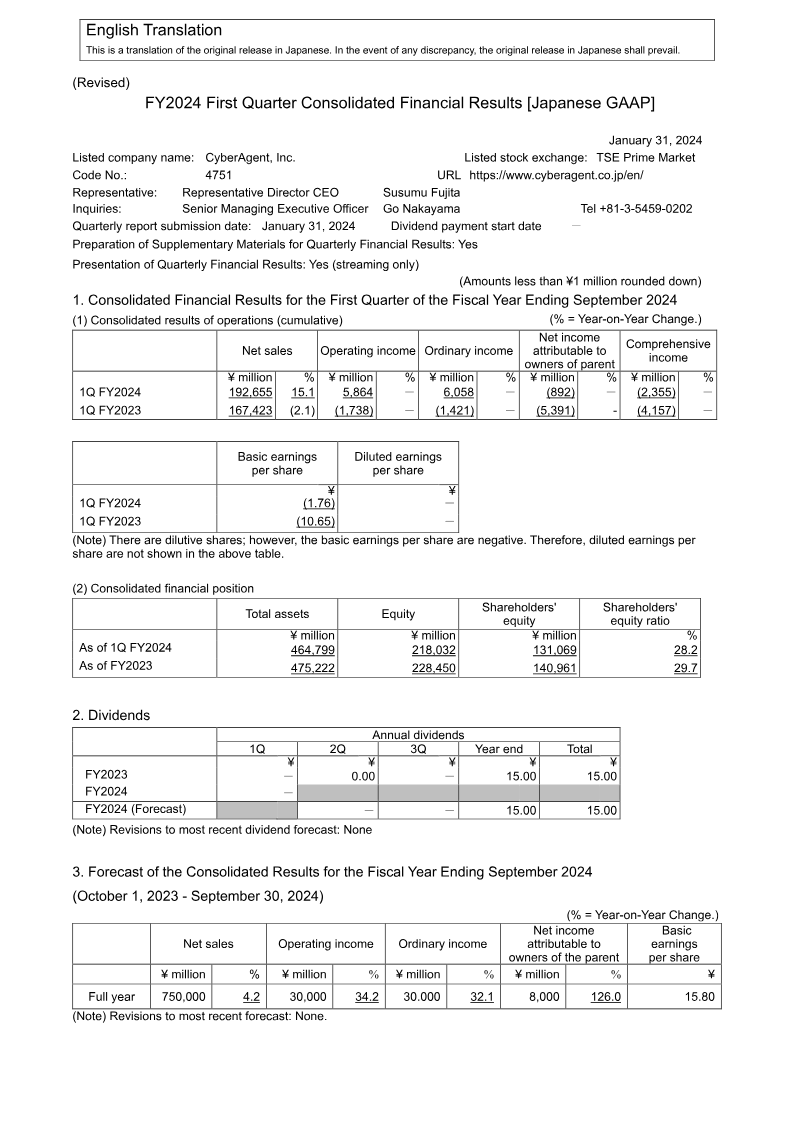

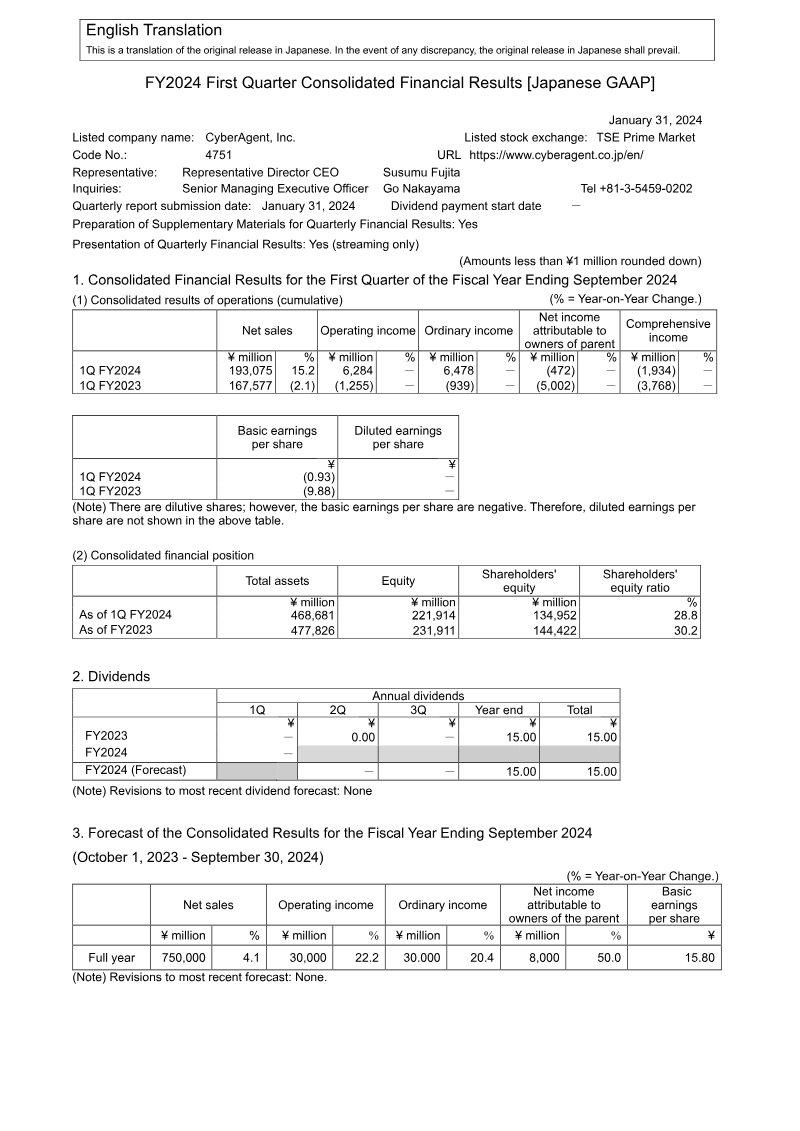

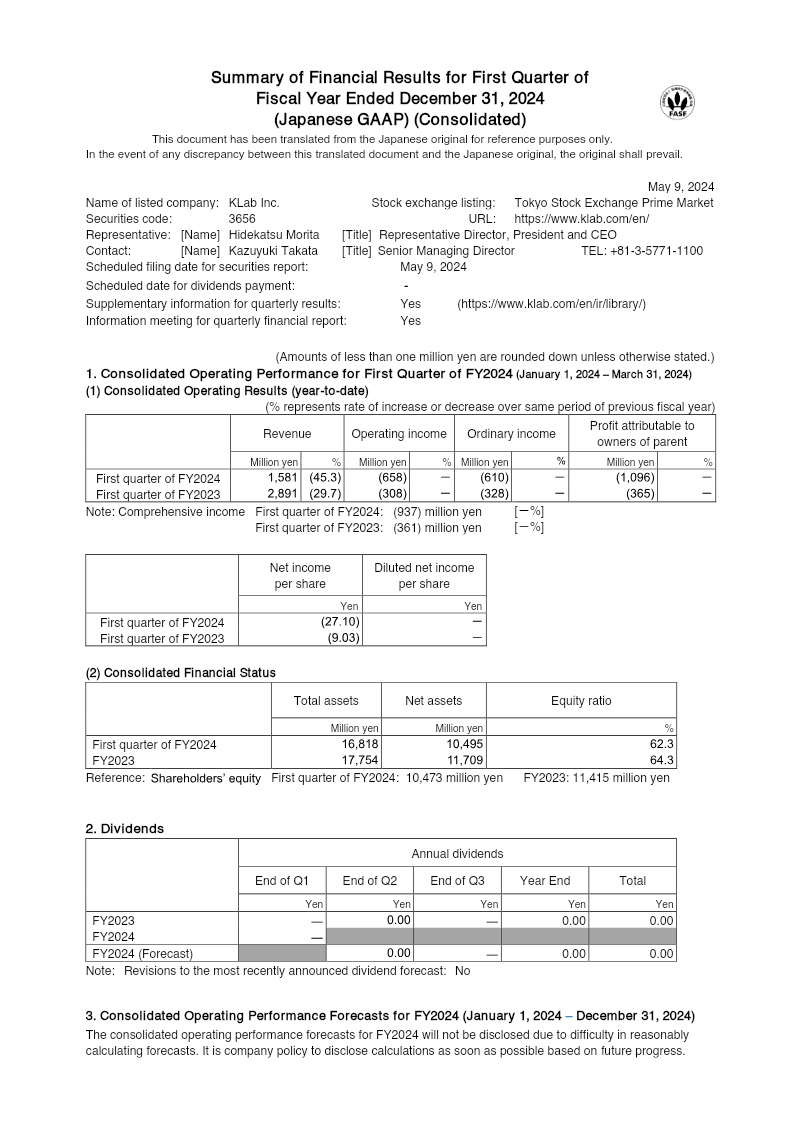

Summary of Financial Results for First Quarter: Fiscal Year Ended December 31, 2024

KLab Inc. reports a sharp decline in first‑quarter 2024 operating performance, with revenue falling 45.3 % to ¥1,581 million from ¥2,891 million in the same period of FY2023. Operating income turned a loss of ¥658 million, compared with a ¥308 million loss previously. Gross profit swung to a ¥95 million loss, and ordinary income fell to a ¥610 million loss. Net income deteriorated further to a ¥1,096 million loss, reflecting higher interest and investment‑related expenses. Comprehensive income also declined to a ¥937 million loss, driven by a significant valuation gain on available‑for‑sale securities and foreign‑currency translation adjustments. Total assets decreased to ¥16,818 million from ¥17,755 million, while shareholders’ equity fell to ¥10,178 million, lowering the equity ratio to 62.3 % from 64.3 %. Cash and deposits rose modestly, but current liabilities increased to ¥4,767 million, partly due to new short‑term debt. The company’s debt profile shows a reduction in long‑term debt but an increase in short‑term obligations. KLab’s segment analysis indicates that its core game business remains the primary revenue driver, yet the blockchain‑related segment has been excluded from consolidation after a partial divestiture of BLOCKSMITH&Co. The company continues to pursue large‑scale mobile titles and hybrid casual games, while cutting outsourcing and personnel costs to improve cash flow. Recent capital‑raising activities include the issuance of 19th Stock Acquisition Rights and a 1st series unsecured bond, totaling approximately ¥2.94 billion in net proceeds. Overall, the report highlights ongoing operating deficits and negative cash flows, prompting management to implement cost‑reduction measures, asset sales, and new development initiatives to strengthen liquidity and address doubts about the group’s ongoing‑concern status.

KLab

Report

1Q FY2025 Presentation Material

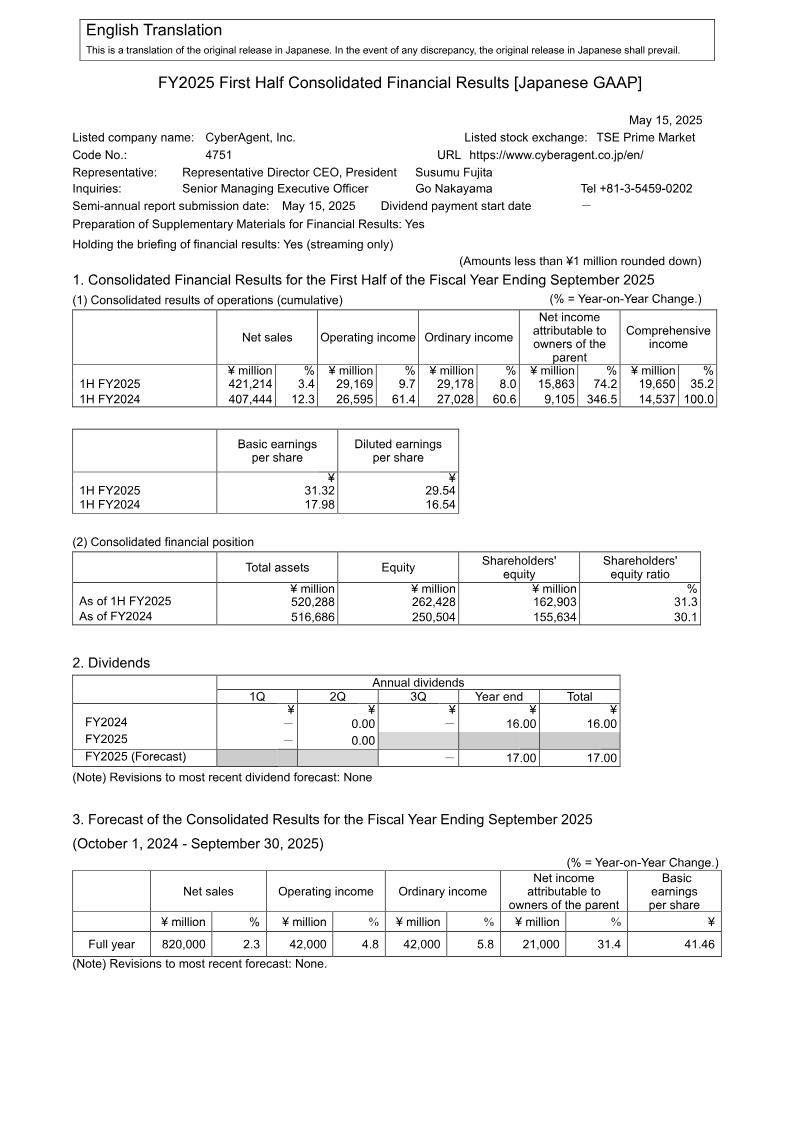

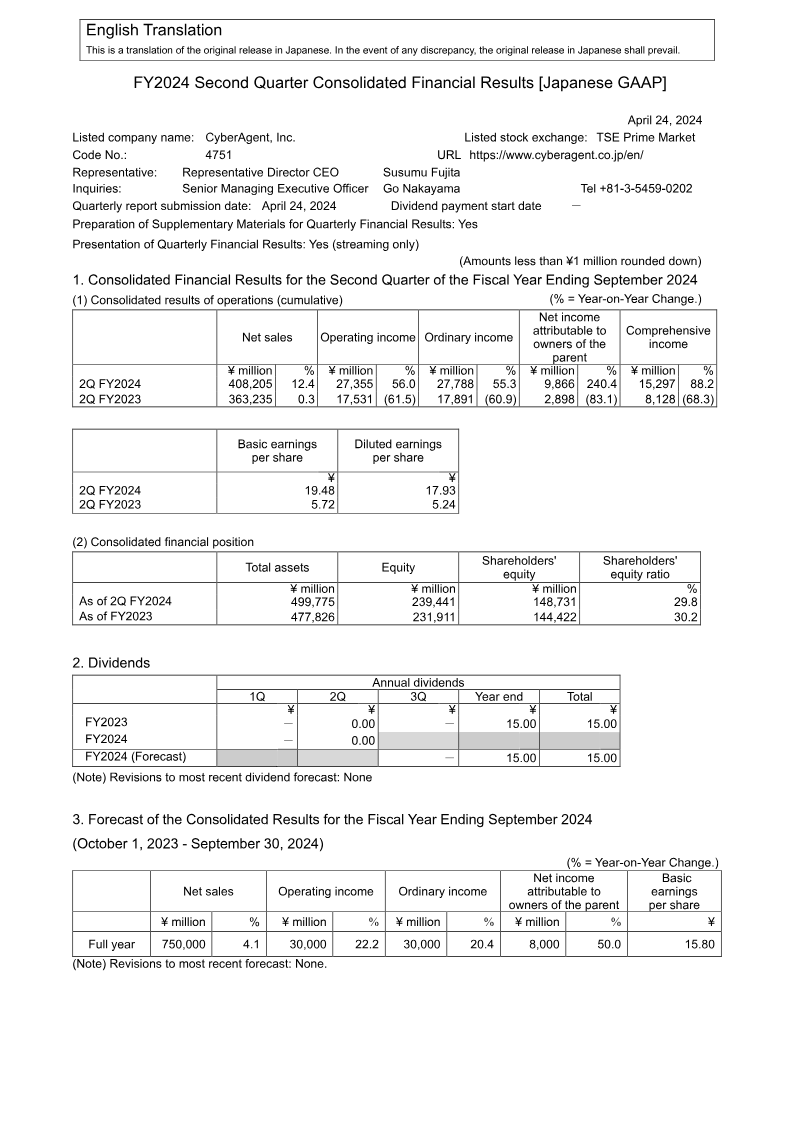

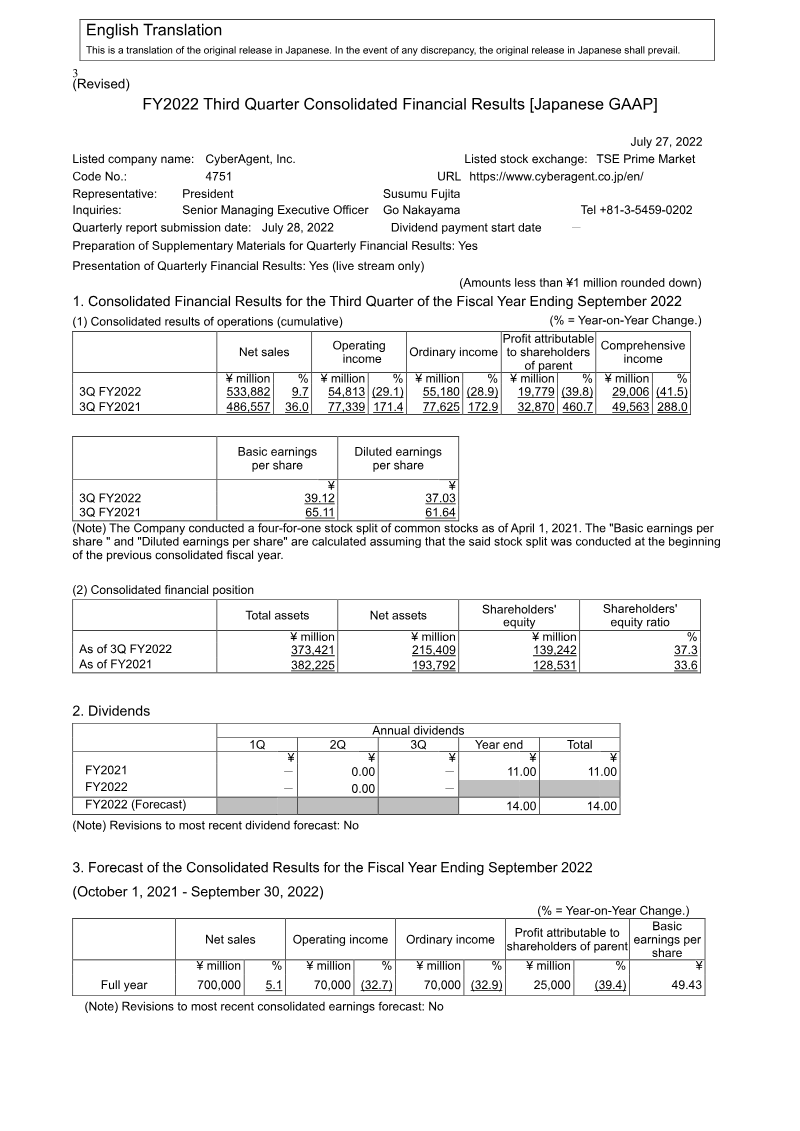

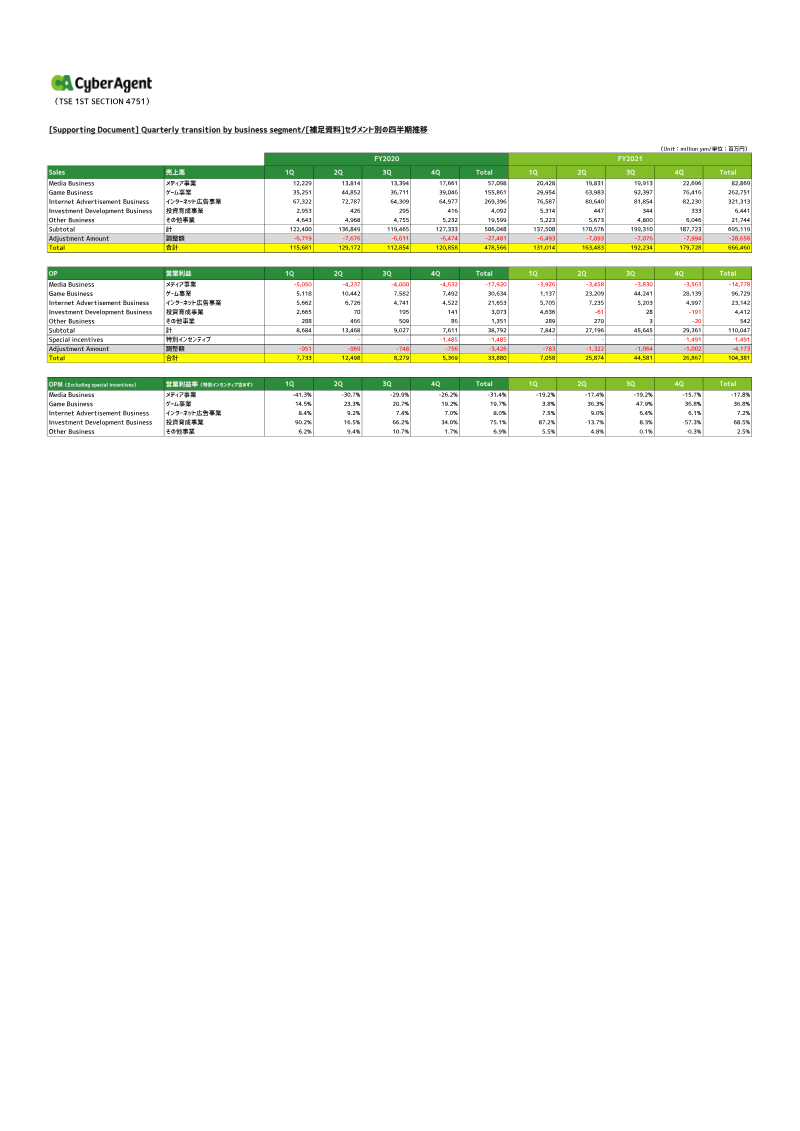

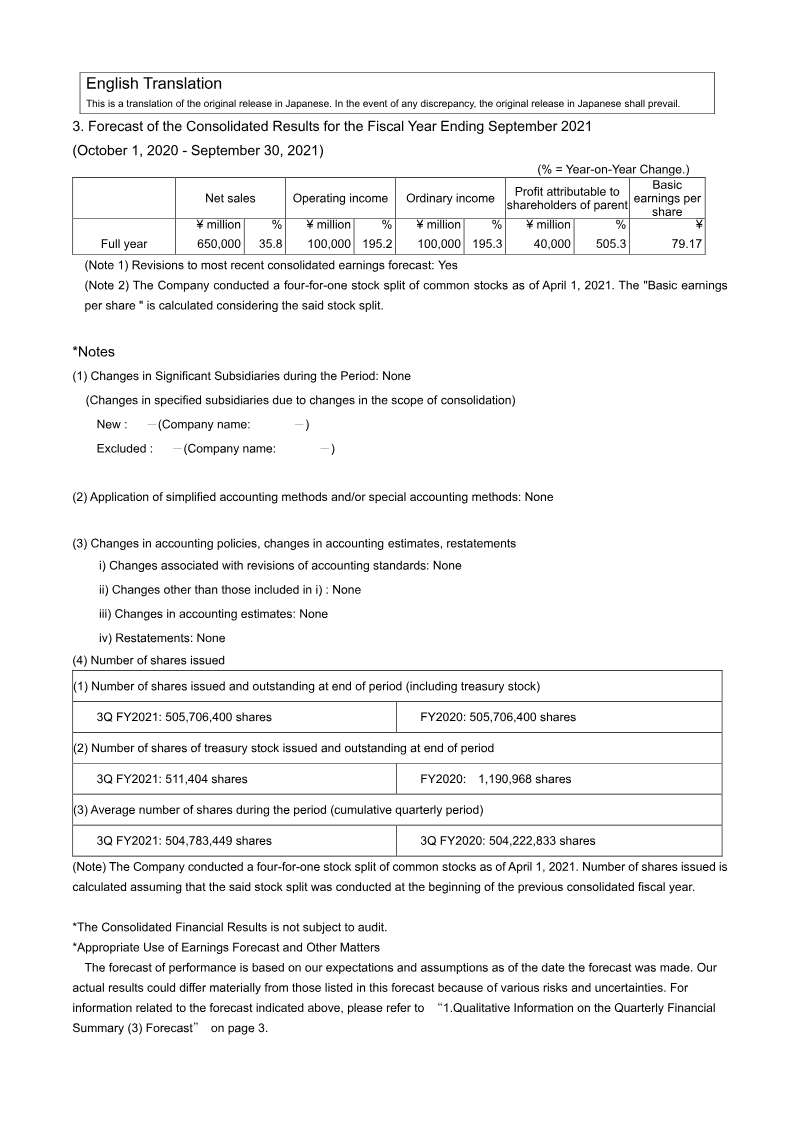

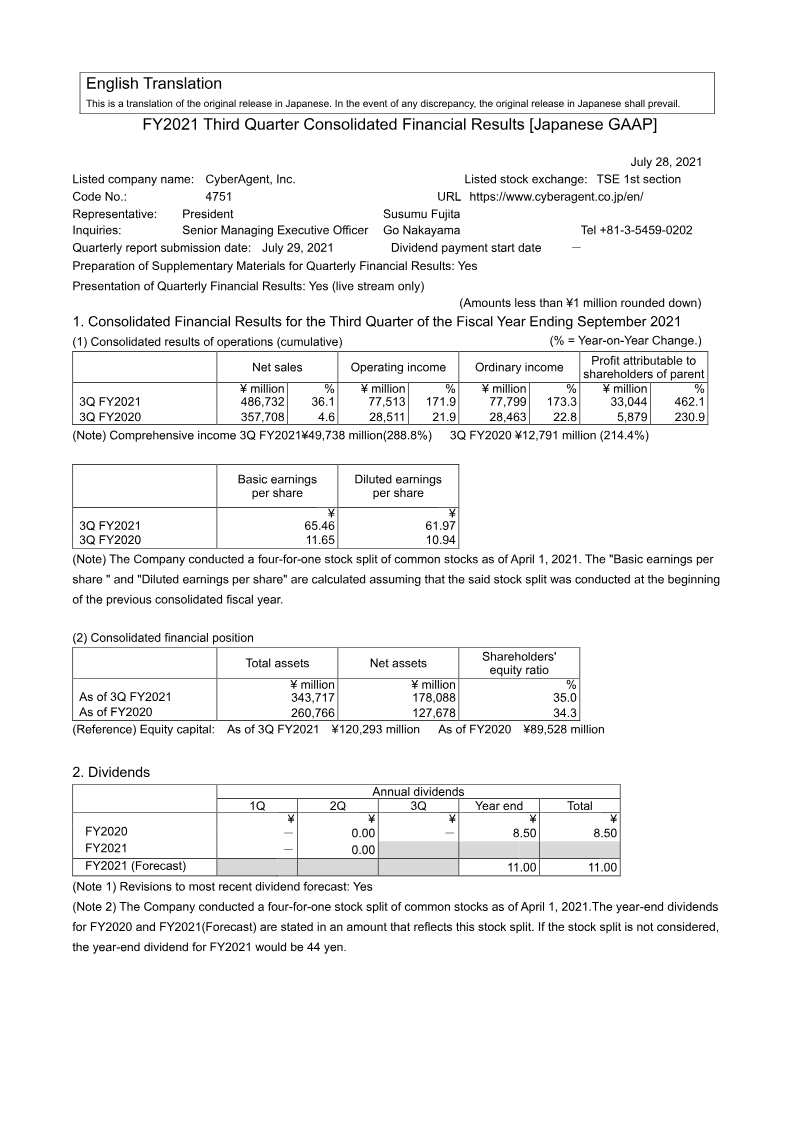

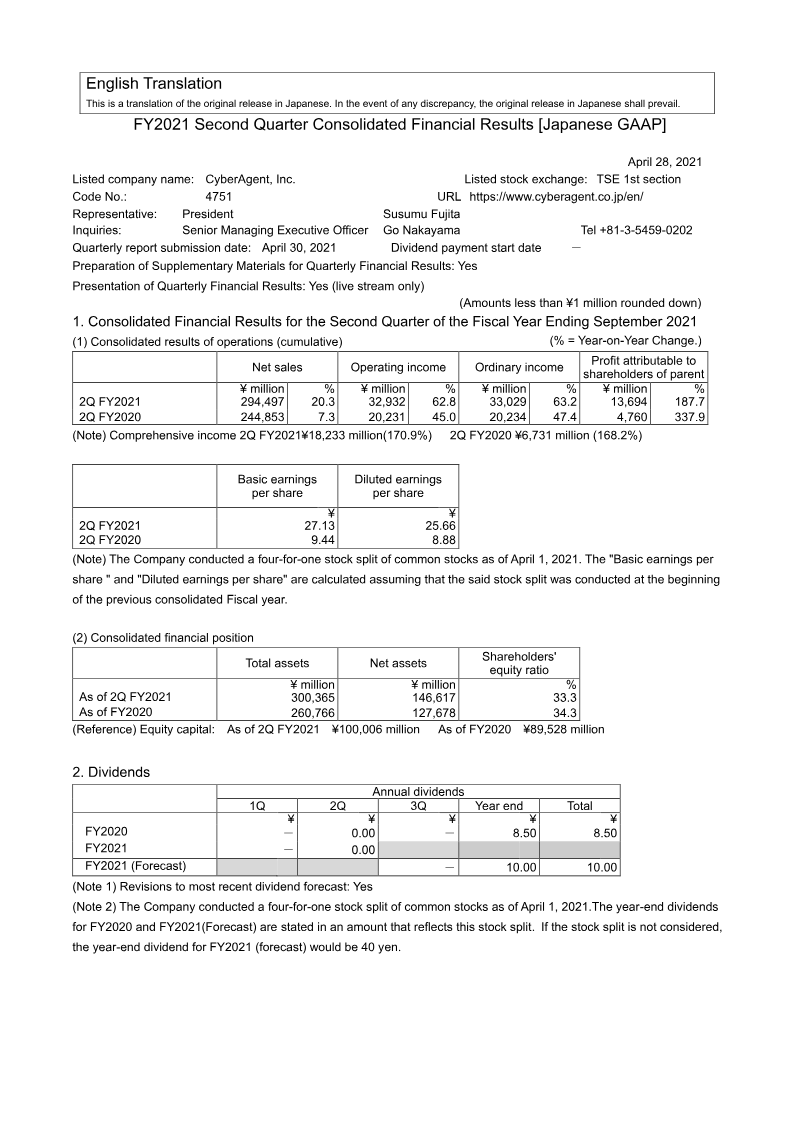

The presentation outlines CyberAgent’s FY 2025 financial outlook, operational highlights, and strategic priorities across its Media & IP, Internet Advertising, and Game divisions. FY 2025 revenue is projected at ¥820 billion with operating profit of ¥42 billion, representing 24.9 % and 19.8 % of the year‑to‑date targets, respectively. First‑quarter results show a 5.6 % YoY sales increase to ¥203.8 billion and a 32.1 % rise in operating profit to ¥8.3 billion, driven largely by a 10.5 % lift in Media & IP sales (¥55.6 billion) and an 11.8 % growth in Internet Advertising sales (¥117.7 billion). The Game segment, however, posted a 15.1 % YoY decline to ¥38.2 billion and a 4.1 % drop in operating profit, attributed to slower releases despite strong performance of new titles. Operating margins improved from 3.3 % in FY 2024 to 4.1 % in FY 2025, supported by a 32 % increase in operating income. SG&A expenses rose 4.4 % YoY to ¥45.7 billion, while cash deposits increased 11.3 % YoY to ¥205.6 billion, reflecting liquidity strengthening. Strategically, the company is shifting from a Media‑only model to an integrated Media & IP business, aiming to generate global IPs through ABEMA and new production units such as CA Soa Inc. The medium‑to‑long‑term plan emphasizes investment in high‑profit IP content, game development, and advertising technology leveraging AI to enhance ad effectiveness. The presentation also lists a pipeline of over six new games for FY 2025, including international releases, and outlines organizational changes to support the expanded IP focus.

CyberAgent