Gaming Industry Report: Q4 2022

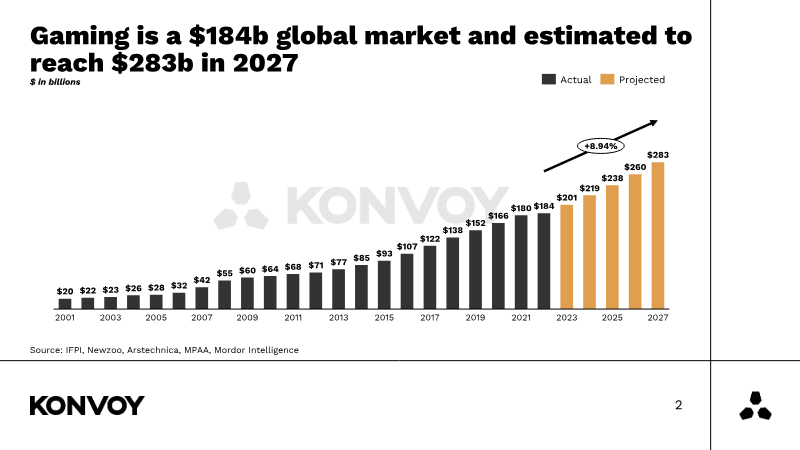

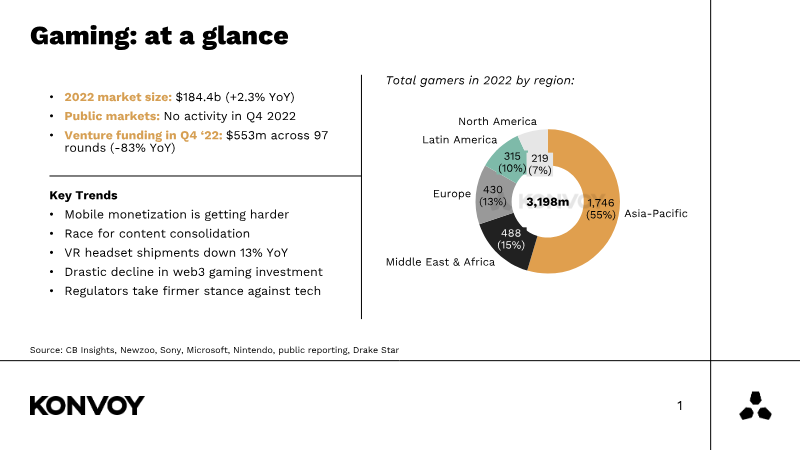

The analysis presents a comprehensive overview of the global gaming market in 2022 and its projected trajectory to 2027, emphasizing a modest expansion of the sector’s revenue base and a shifting investment landscape. The market reached $184.4 billion in 2022, a 2.3 % year‑over‑year increase, and is forecast to climb to $283 billion by 2027, reflecting an annual growth rate of roughly 9 %. Mobile platforms remain the dominant distribution channel, accounting for $116 billion of consumer spend in 2021, or 64 % of total gaming revenue, while console and emerging XR segments experience divergent pressures.

Venture capital activity illustrates a pronounced contraction after a 2021 peak, with total funding falling from $8.8 billion to $5.3 billion in 2022 and growth‑stage deals declining despite a stable number of transactions. Funding for web3 gaming collapsed by 83 % in Latin America and saw a global downturn, driven by concerns over token utility, game quality, and high-profile fraud incidents. Concurrently, regulatory scrutiny intensified, particularly around data‑privacy measures such as Apple’s IDFA and Google’s AAID, which have raised user‑acquisition costs and forced developers to prioritize content depth over advertising efficiency.

Corporate liquidity underscores a robust M&A environment: gaming firms collectively hold $47.7 billion in cash, while major tech companies with gaming divisions command $157 billion. Nevertheless, gaming‑focused ETFs underperformed, with ESPO and GAMR posting year‑to‑date declines of 35 % and 37 % respectively. The report draws on a blend of public market data, venture‑capital databases, and industry surveys from sources such as CB Insights, Newzoo, and major console manufacturers, covering all major regions and spanning the period from 2019 through Q4 2022.