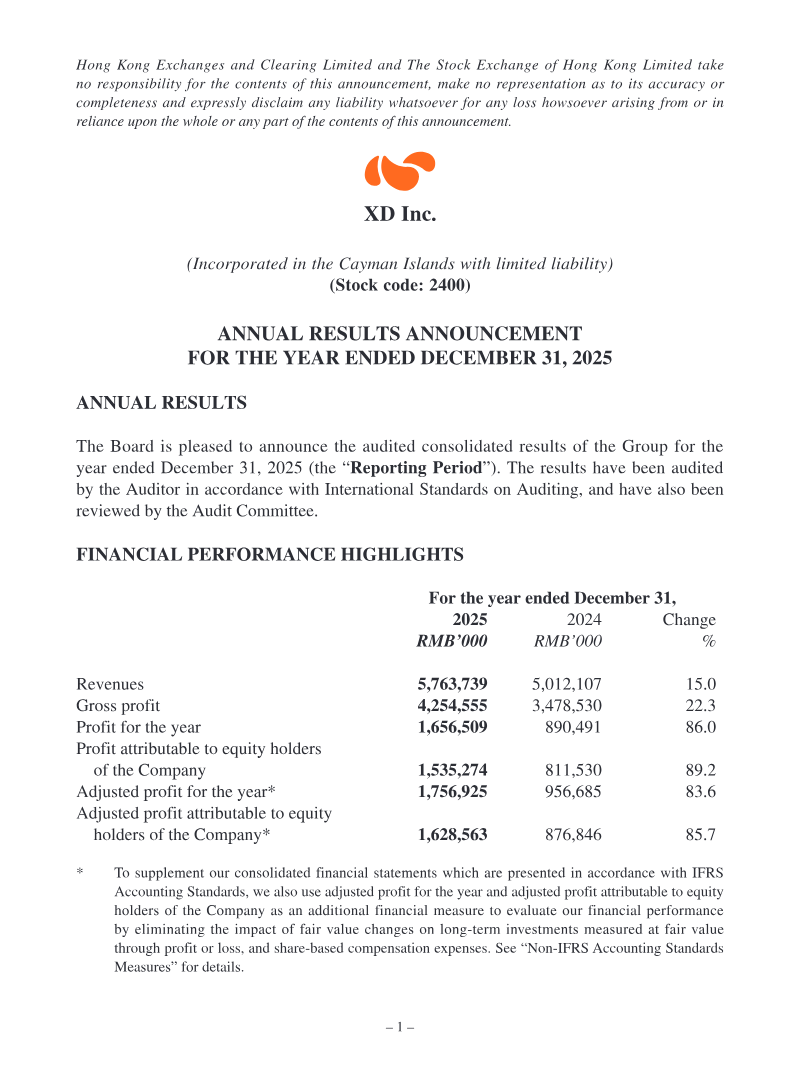

XD Inc. achieved substantial financial growth throughout the 2025 fiscal year, characterized by a 15% increase in total revenue to RMB 5.76 billion and a significant surge in profit attributable to equity holders, which reached RMB 1.54 billion. This performance was underpinned by a 10.5% rise in gaming revenue, bolstered by the success of titles such as Heartopia and Torchlight: Infinite, alongside a 24.7% revenue increase within the TapTap platform. The company’s financial health was further strengthened by an improved gross margin of 73.8% and a robust cash position of RMB 3.77 billion, supported by a strategic reduction in the cost of revenues and a lower gearing ratio of 22.5%.

The company’s strategic focus remains centered on cross-platform expansion and the integration of AI-driven development tools to secure long-term competitiveness. While financial metrics showed marked improvement, the company observed a decline in online game user metrics, specifically monthly active users and monthly paying users. To address these shifts, management has prioritized capital optimization through active share repurchases and the maintenance of employee incentive programs. Notably, the board opted against a final dividend for 2025, citing a commitment to capital reinvestment and a need to address corporate governance concerns regarding the consolidation of the chairman and CEO roles.

These results reflect a period of operational consolidation and international market penetration for the China-based firm. The financial figures, which have been reviewed by the Audit Committee and aligned with the group’s consolidated statements, demonstrate a transition toward higher profitability and operational efficiency. By leveraging the acquisition of the Torchlight intellectual property and refining advertising algorithms on the TapTap platform, the company aims to sustain its growth trajectory despite the challenges posed by fluctuating user engagement metrics in the broader gaming sector.

Giant Network Group · 2026

Archosaur Games · 2026

Meridian Play · 2026

GREE

Bilibili

Tencent

Tencent Holdings Limited

Tencent

Pearl Abyss · 2026

Modern Times Group · 2026

GungHo Online Entertainment · 2026

Kakao Games · 2026