PresentationGungHo Online Entertainment

Financial Results Briefing FY2025

1 Feb 202624 pages~10 min full read

GungHo is executing a strategic pivot from the domestic Japanese mobile market to a global, multi-platform model, with overseas net sales projected to reach 66% of total revenue in FY2025, up from 11.4% in 2016.

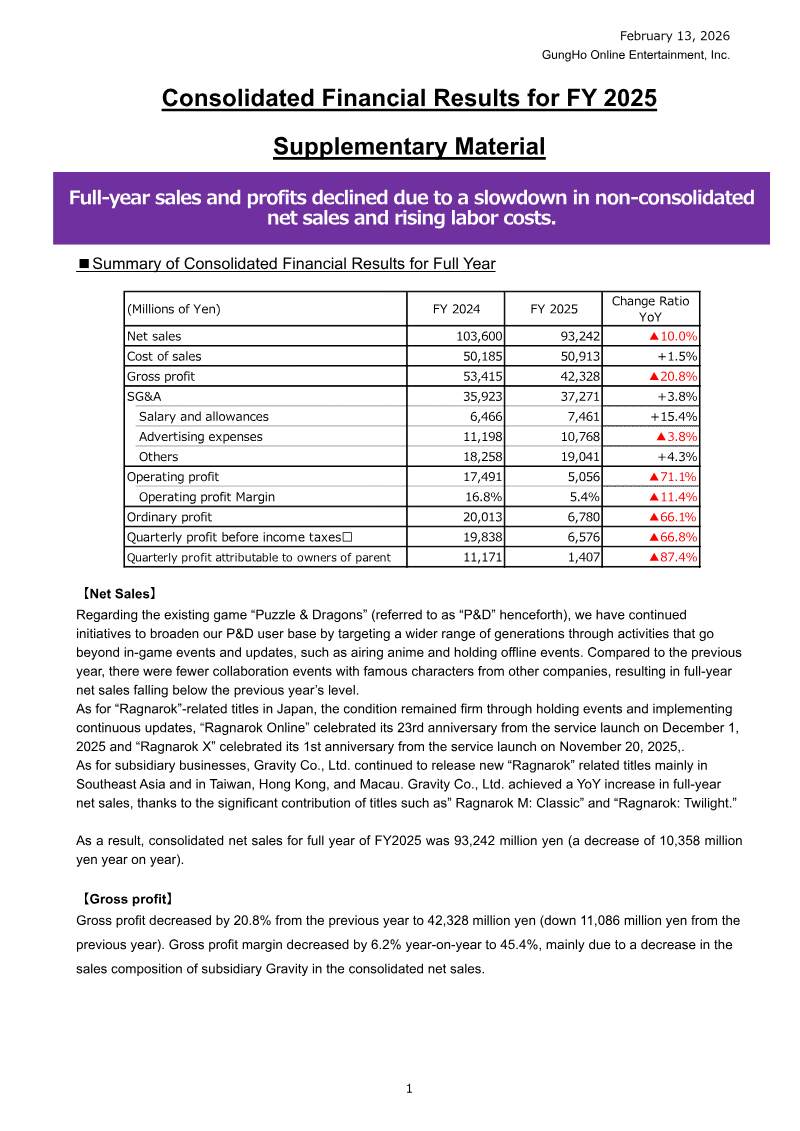

See it on page 5Consolidated net sales and operating profit are in a four-year decline, with quarterly performance metrics dropping from a peak of over 16,000 to approximately 7,750.

See it on page 22The company is addressing the softening sales of legacy mobile titles and decreased revenue from its subsidiary Gravity by leveraging high-profile collaborations with brands like Sanrio and Digimon.

See it on page 23Future growth is anchored in the expansion of the Ragnarok franchise, including the upcoming launch of Ragnarok Online 3 in Asian markets and the introduction of Ragnarok X: Next Generation to EMEA regions.

See it on page 14GungHo is shifting its development focus toward action-oriented console and PC intellectual properties, highlighted by the upcoming release of Let It Die: Inferno.

See it on page 11To compete in the global market, the company is integrating more technologically ambitious features, such as 100-player raid mechanics, into its new project pipeline.

See it on page 10GungHo Online Entertainment is currently undergoing a fundamental strategic pivot, transitioning from a primary focus on the domestic Japanese mobile market toward a global, multi-platform distribution model. This evolution targets North America and Europe specifically through the development of action-oriented intellectual properties for console and PC. The success of this shift is evidenced by the dramatic rise in the overseas net sales ratio, which is projected to reach 66% in fiscal year 2025, up from just 11.4% in 2016. Key drivers for this international expansion include the upcoming launch of Let It Die: Inferno and the continued global scaling of the Ragnarok and Puzzle & Dragons franchises across more than 150 countries.

Despite this aggressive geographic expansion, the company faces immediate financial headwinds characterized by a contraction in consolidated net sales and operating profit. Quarterly performance data reveals a downward trajectory over a four-year period, with peak values declining from over 16,000 to approximately 7,750 in the most recent quarter. This downturn is largely attributed to softening sales of legacy mobile titles and a reactional decrease in revenue from the subsidiary Gravity. To stabilize these core assets, the company is utilizing high-profile collaborations with major brands such as Sanrio and Digimon to maintain domestic user engagement while simultaneously preparing for the launch of Ragnarok Online 3 in major Asian markets.

The long-term outlook centers on a diversified portfolio that balances established mobile revenue with new, high-scale global releases. While current financial indicators reflect a period of contraction and volatility, the commitment to 100-player raid mechanics in upcoming titles and the expansion of Ragnarok X: Next Generation into EMEA markets signal a move toward more technologically ambitious projects. Ultimately, the transition toward a global-first strategy represents a necessary adaptation to the maturing domestic mobile landscape, aiming to replace declining legacy revenue with sustainable growth from international console and PC audiences.