More from Bushiroad

View all

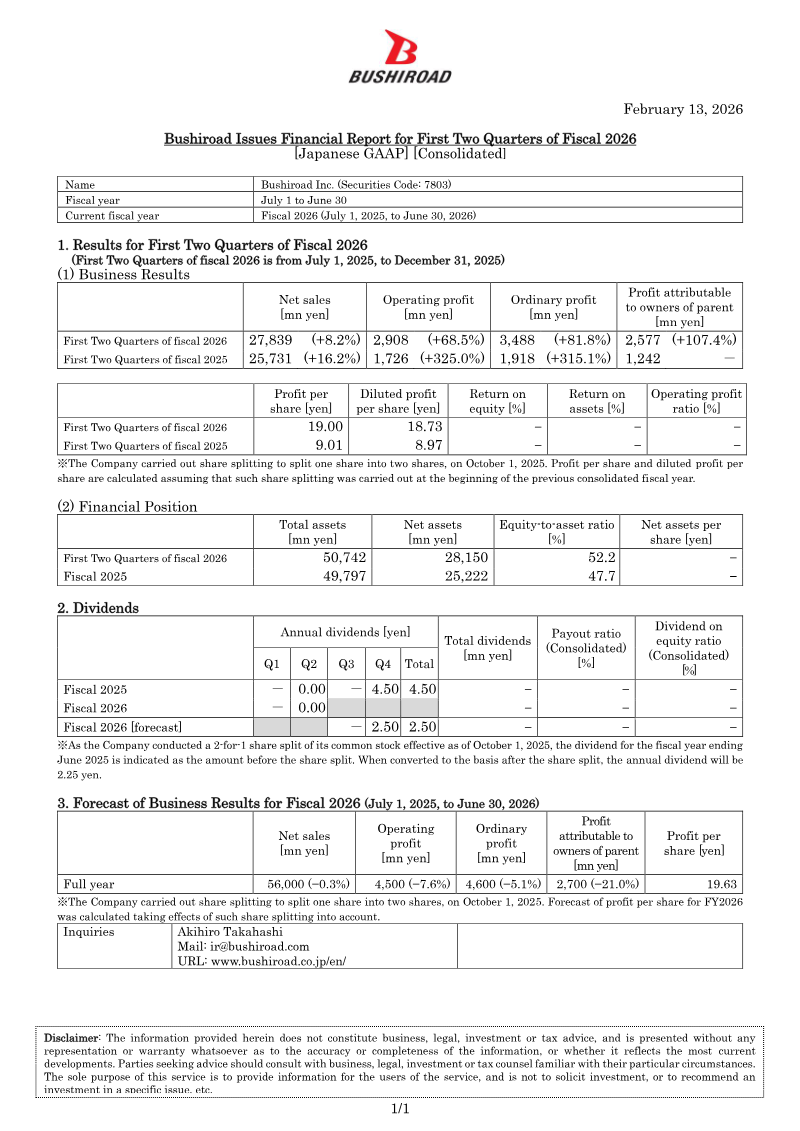

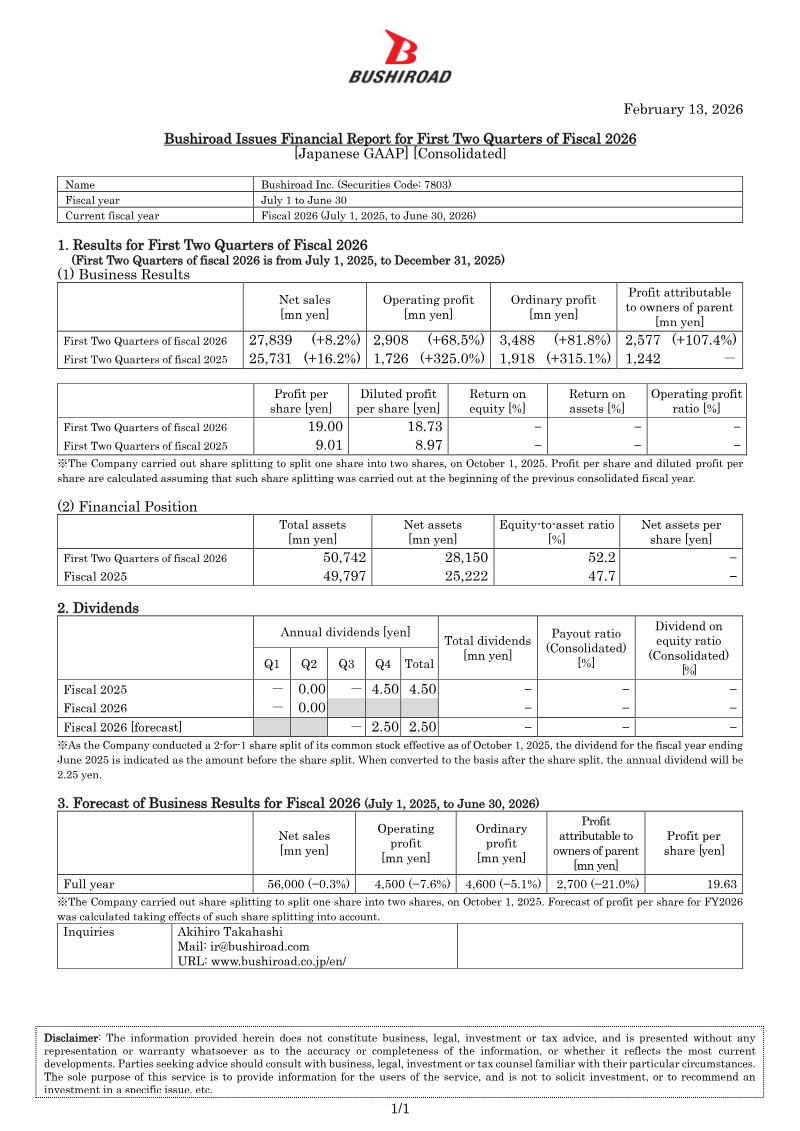

Financial

Bushiroad Issues Financial Report for First Two Quarters of Fiscal 2026

Bushiroad · 2026

Financial

FY2026 2Q Financial Results Briefing Material

Bushiroad · 2026

Financial

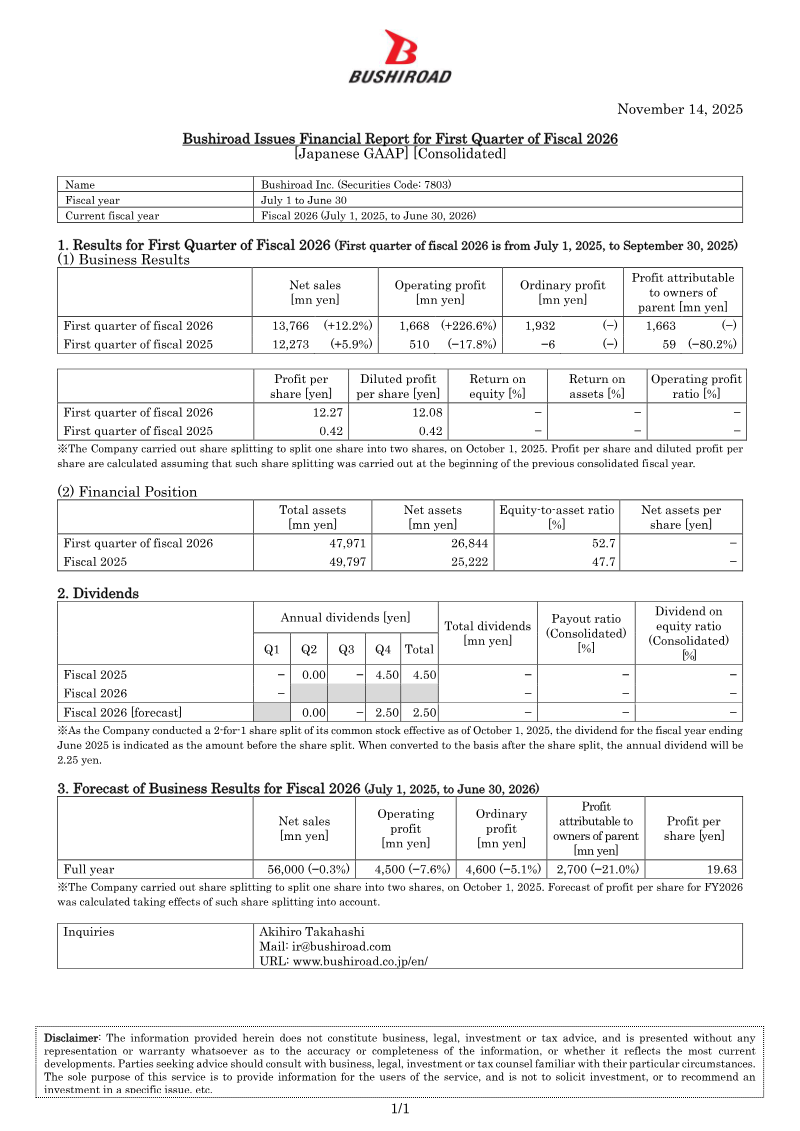

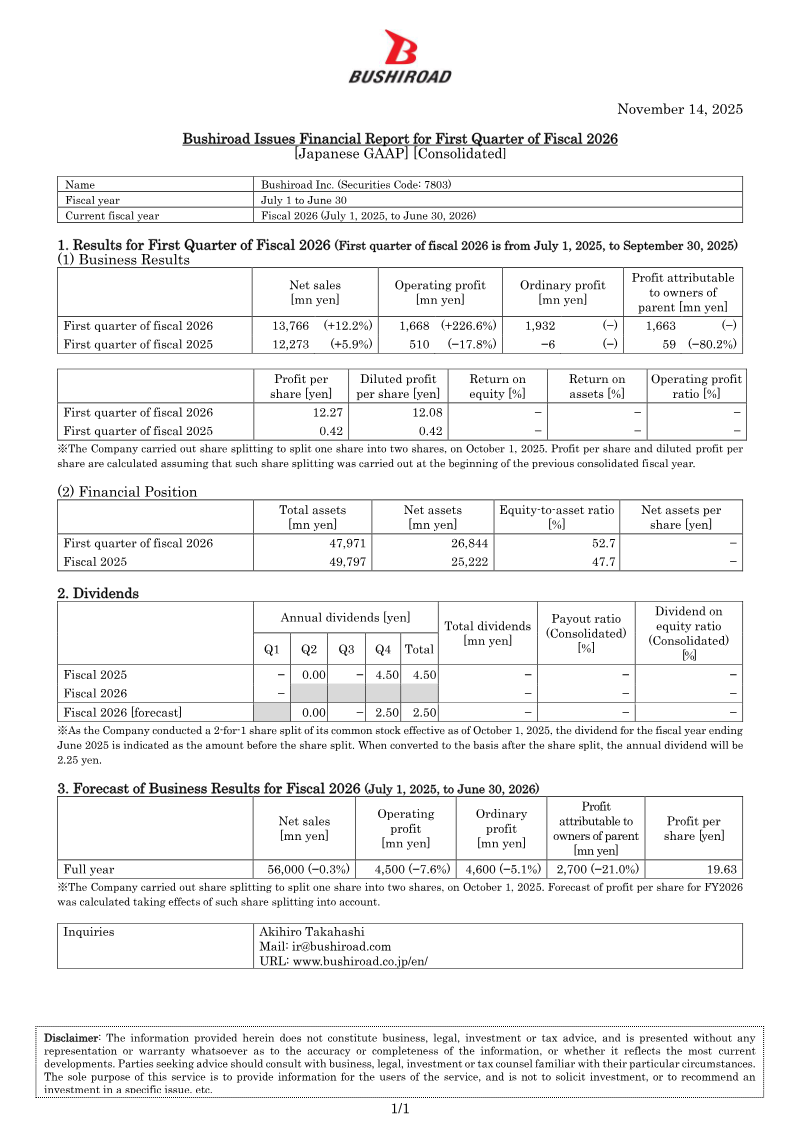

Bushiroad Issues Financial Report for First Quarter of Fiscal 2026

Bushiroad · 2025

Legal

Bushiroad Announces “Bushiroad EXPO 2026”: Expanding on a Global Scale

Bushiroad · 2025

Financial

FY2026 1Q Financial Results Briefing Material

Bushiroad · 2025

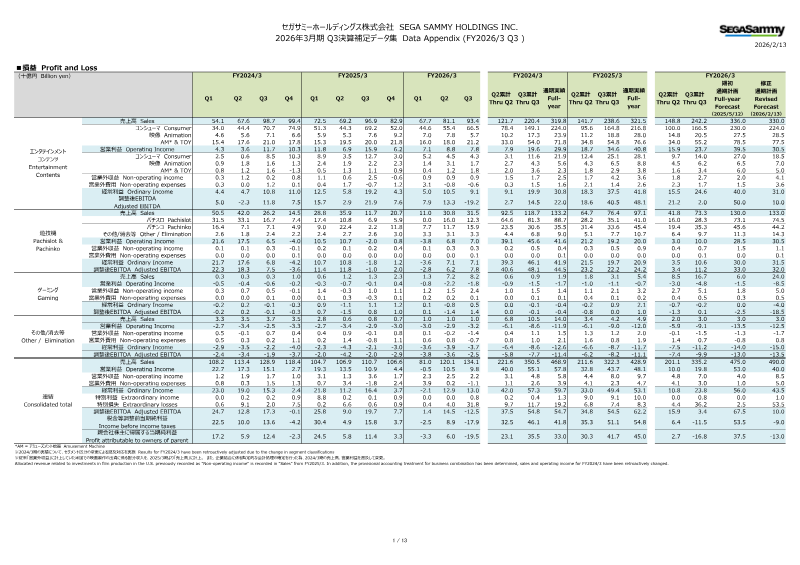

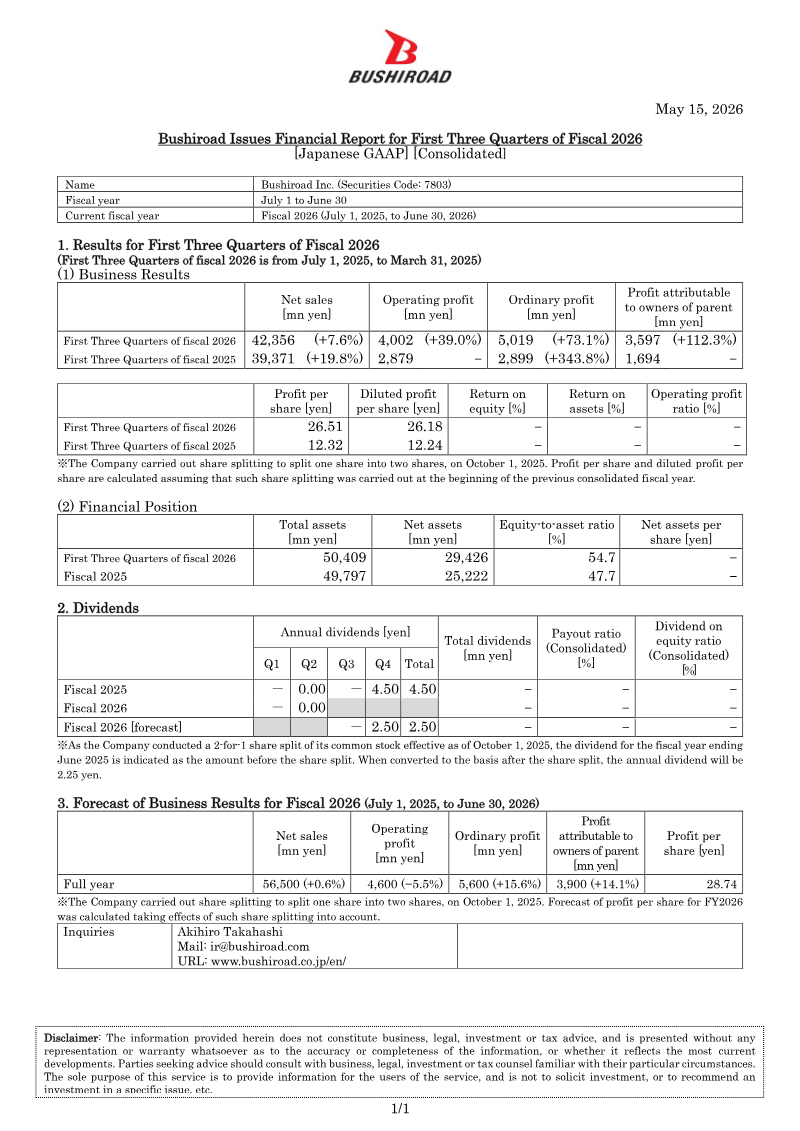

Financial

Financial Results for the First Three Quarters of Fiscal 2026: Japan

Bushiroad

Financial

FY2026 3Q Financial Results Briefing Material

Bushiroad

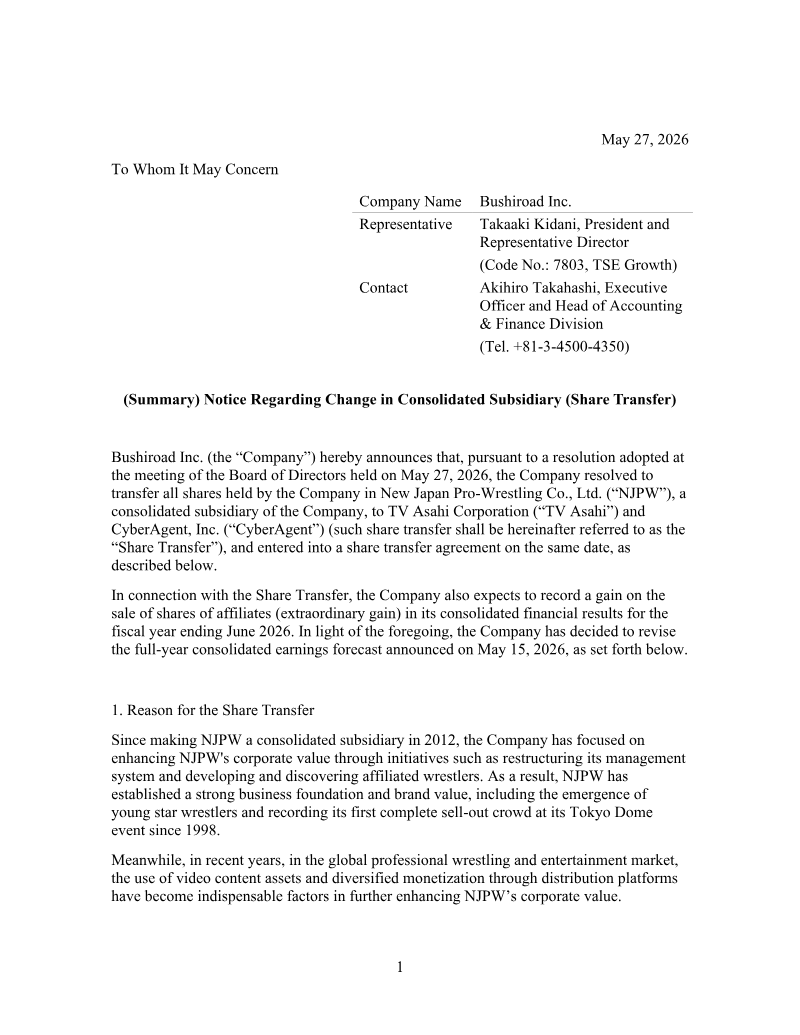

Financial

Notice Regarding Change in Consolidated Subsidiary: Share Transfer

Bushiroad

Bushiroad Strengthens Global Expansion:

Article

Bushiroad Strengthens Global Expansion: Overseas TCG Sales Ratio Projected to Exceed 50%

Bushiroad

Financial

FY2026 1Q Financial Results Briefing Material: Japan

Bushiroad

Report

Financial Report for First Two Quarters: Fiscal 2026

Bushiroad

Report

Financial Report for First Quarter of Fiscal 2026: Japan

Bushiroad