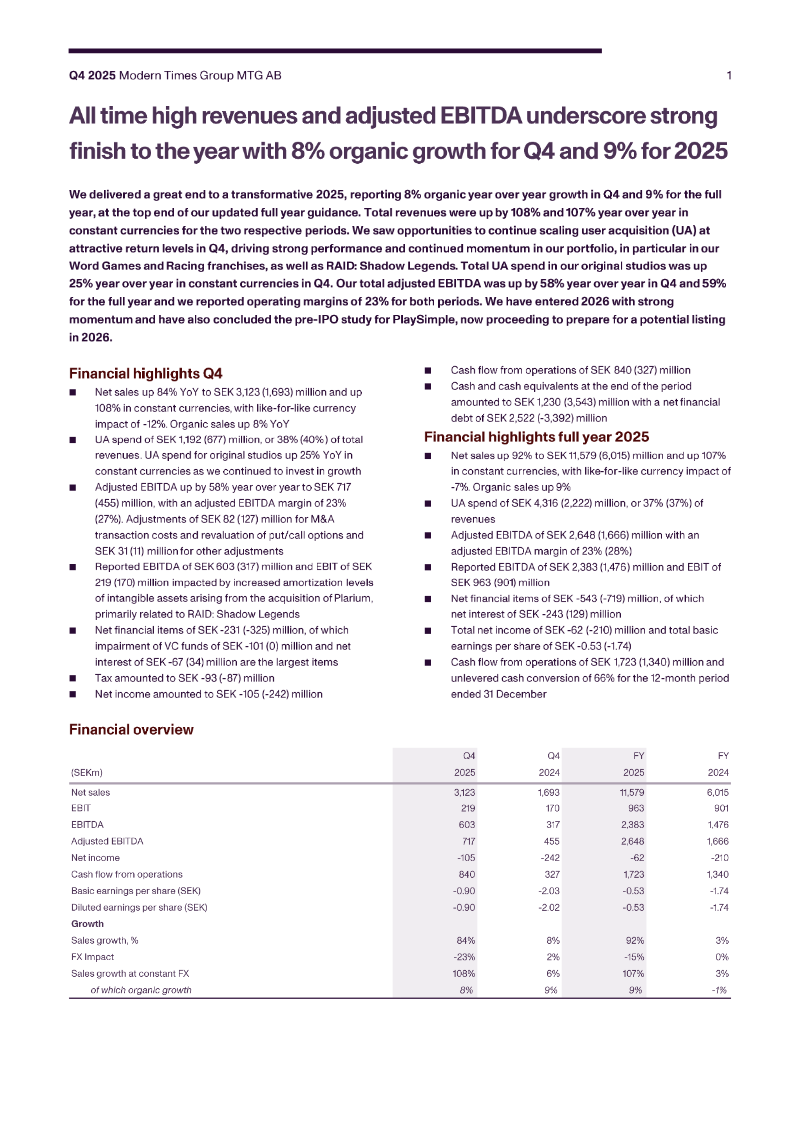

FinancialModern Times Group

Conference Call Q1 2023

1 May 202311 pages~4 min full read

MTG reported Q1 2023 net revenues of SEKm 1,306, marking a 4% year-on-year decrease and an 11% organic decline driven by difficult comparisons against pandemic-era performance.

Adjusted EBITDA reached SEKm 263 with a 20% margin, which represents an underlying margin increase on a like-for-like basis when excluding prior-year platform bonuses.

PlaySimple’s Word Games franchise maintained its position as the company’s strongest performer for the fifth consecutive quarter, while Ninja Kiwi’s Tower Defense IP showed continued resilience.

User engagement metrics saw a slight decline in Monthly Active Users (MAU) to 29.4 million, while Daily Active Users (DAU) remained stable at 6.4 million.

The company maintains a strong liquidity position with approximately SEK 6 billion available for debt and earn-out capacity to support future M&A and shareholder value creation.

Despite a negative free cash flow of SEKm 329 after earn-out payments, the company achieved a 51% cash conversion rate from operations.

Modern Times Group (MTG) reported a mixed financial performance for the first quarter of 2023, characterized by strong results in specific gaming franchises despite an overall decline in organic revenue. Net revenues reached SEKm 1,306, representing a 4% decrease year-on-year and an 11% organic decline. This downturn was primarily attributed to challenging year-on-year comparisons for InnoGames, which benefited from a post-pandemic boost in early 2022, and a non-recurring platform incentive payment received by PlaySimple in the previous year.

The company’s portfolio showed divergent trends across its core segments. The Word Games franchise, led by PlaySimple, remained the strongest performer for the fifth consecutive quarter, while Ninja Kiwi’s Tower Defense IP demonstrated continued resilience. Conversely, the Strategy & Simulation and Racing segments faced difficulties, particularly in attracting new players during the first half of the quarter. However, management noted signs of stabilization for InnoGames and gradual improvements in Strategy & Simulation performance toward the end of the period.

Financial health remains stable with an adjusted EBITDA of SEKm 263 and a margin of 20%. While the reported margin was lower than the 25% seen in Q1 2022, the underlying margin increased slightly on a like-for-like basis when adjusting for the prior year’s platform bonuses. User metrics showed a slight decline in Monthly Active Users (MAU) to 29.4 million, though Daily Active Users (DAU) remained relatively stable at 6.4 million.

MTG maintains a robust balance sheet with a strong cash position and a total debt and earn-out capacity of approximately SEK 6 billion. This liquidity is intended to support future M&A activities and shareholder value creation. Despite a negative free cash flow after earn-out payments of SEKm 329 for the quarter, the company reported a 51% cash conversion rate from operations, signaling a solid foundation for its ongoing portfolio diversification strategy.