FinancialAiming

Consolidated Financial Results for the First Quarter of the Fiscal Year Ending December 31, 2025 (Japanese GAAP)

14 May 202510 pages~6 min full read

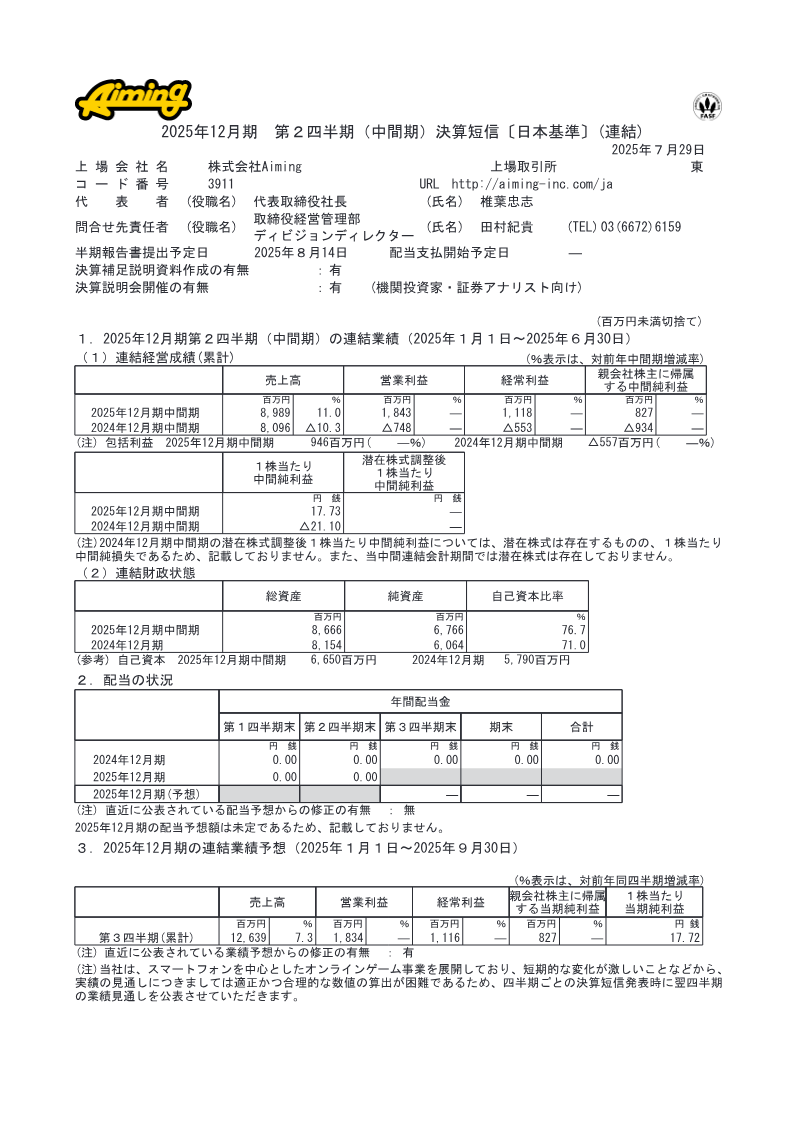

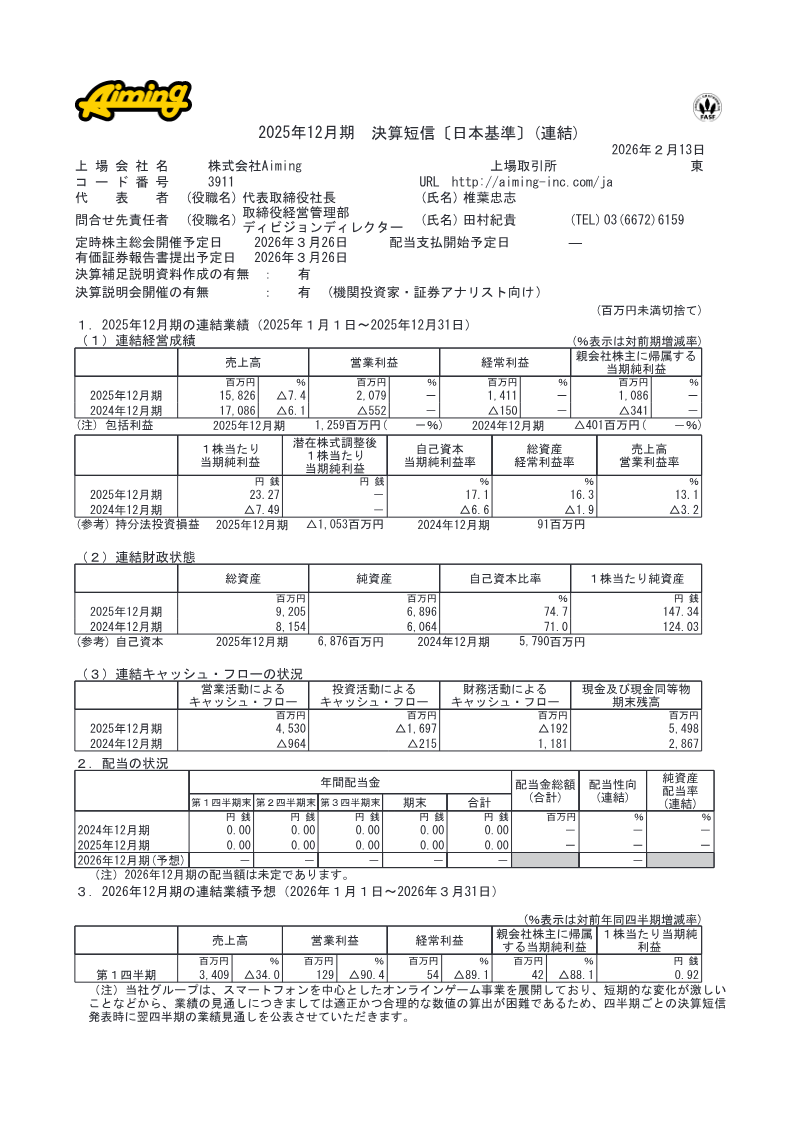

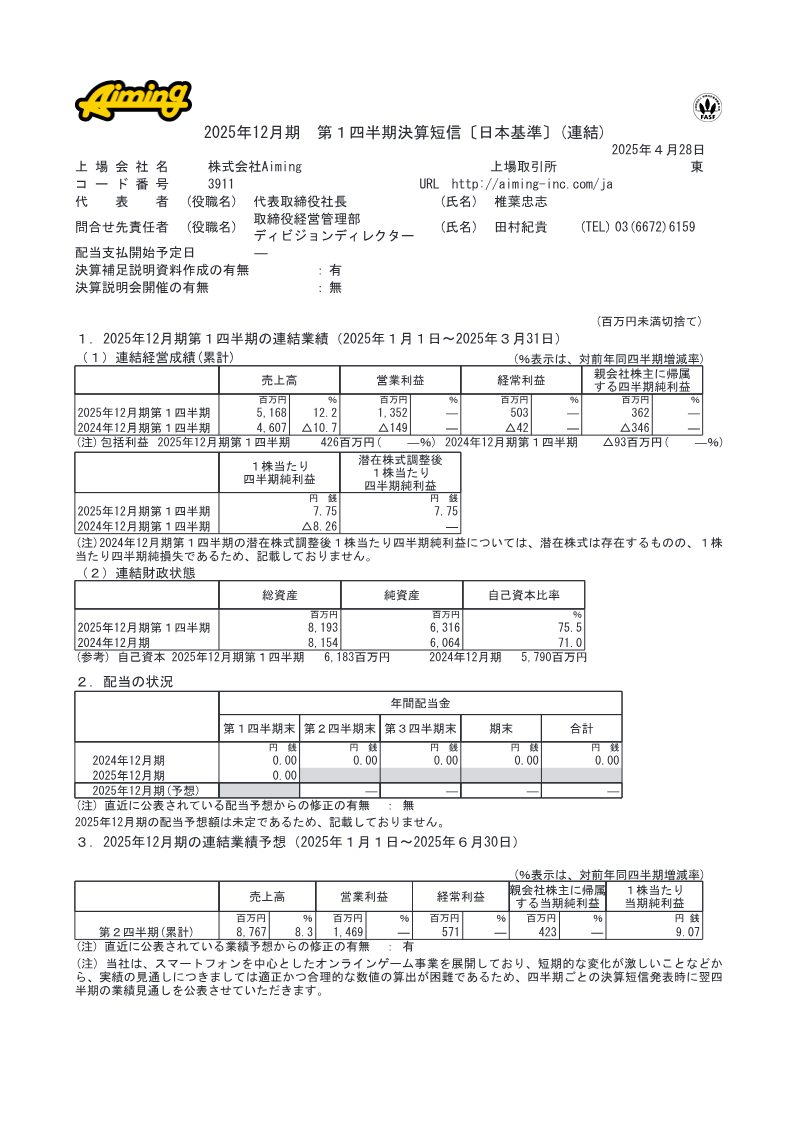

Aiming Inc. achieved a financial turnaround in Q1 2025, reporting net sales of 5,168 million yen (a 12.2% year-over-year increase) and an operating profit of 1,352 million yen, compared to a 149 million yen loss in Q1 2024.

See it on page 3Net income attributable to owners of the parent reached 362 million yen for the quarter, reversing the 346 million yen loss recorded during the same period in 2024.

See it on page 8Performance was driven by established titles including 'Dragon Quest Tact' and 'The Eminence in Shadow: Master of Garden,' alongside the March 2025 launch of 'WIND BREAKER: Heroic Spirits.'

See it on page 4The company is diversifying beyond gaming by acquiring a 42.85% stake in the keirin portal business KPJ Planning Co., Ltd. for 549 million yen to enter the public sports betting market.

See it on page 10Financial stability improved significantly, with the equity ratio rising to 75.5% and cash and deposits increasing by 1,689 million yen.

See it on page 6For the first half of the fiscal year ending June 30, 2025, the company forecasts net sales of 8,767 million yen and an operating profit of 1,469 million yen.

See it on page 1Aiming Inc. reported a significant financial turnaround in its consolidated results for the first quarter of the fiscal year ending December 31, 2025. Covering the period from January 1 to March 31, 2025, the results show a transition from a loss-making position to profitability. Net sales reached 5,168 million yen, a 12.2% increase year-over-year. Operating income swung from a 149 million yen loss in the previous year to a profit of 1,352 million yen, while net income attributable to owners of the parent reached 362 million yen, compared to a 346 million yen loss in the same period of 2024.

The performance was driven by the stability of existing titles and the strategic management of new releases within the competitive smartphone online game market. Key contributors included Dragon Quest Tact, which maintained active and paying user bases through its 4.5-anniversary event, and The Eminence in Shadow: Master of Garden. The company also launched WIND BREAKER: Heroic Spirits in March 2025. Despite high development costs and intensifying competition from high-quality overseas titles and major IP-based games, Aiming successfully optimized its business schemes and expanded its title portfolio.

Financially, the company strengthened its position, with total assets increasing to 8,193 million yen and the equity ratio rising to 75.5%. Cash and deposits saw a substantial increase of 1,689 million yen. Looking forward, Aiming issued a forecast for the first half of the fiscal year ending June 30, 2025, projecting net sales of 8,767 million yen and an operating profit of 1,469 million yen.

A notable strategic development involves a 549 million yen investment in KPJ Planning Co., Ltd., a keirin (bicycle racing) portal business. By acquiring a 42.85% stake, Aiming intends to apply its game development and operational expertise to the public sports betting market, seeking to diversify revenue streams beyond the traditional online gaming sector.