FinancialAkatsuki

Consolidated Financial Statements for the First Quarter of Fiscal Year Ending March 31, 2026 (Japanese GAAP)

1 Aug 202511 pages~22 min full read

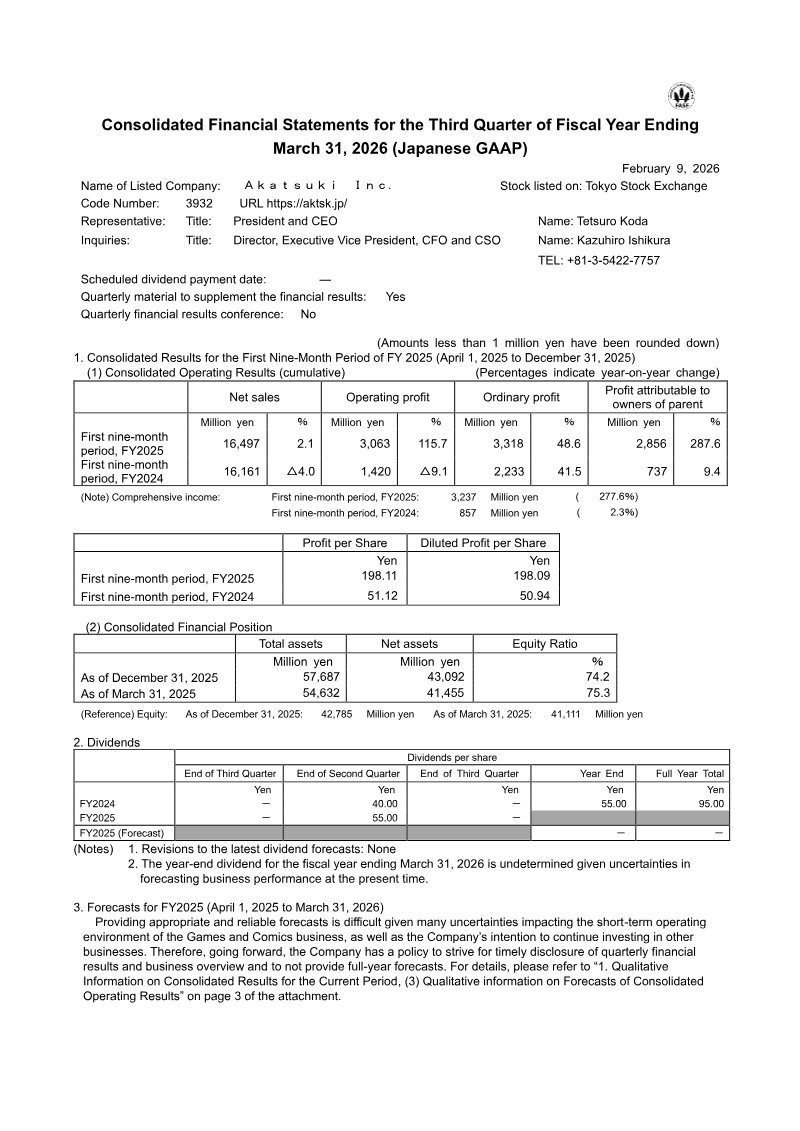

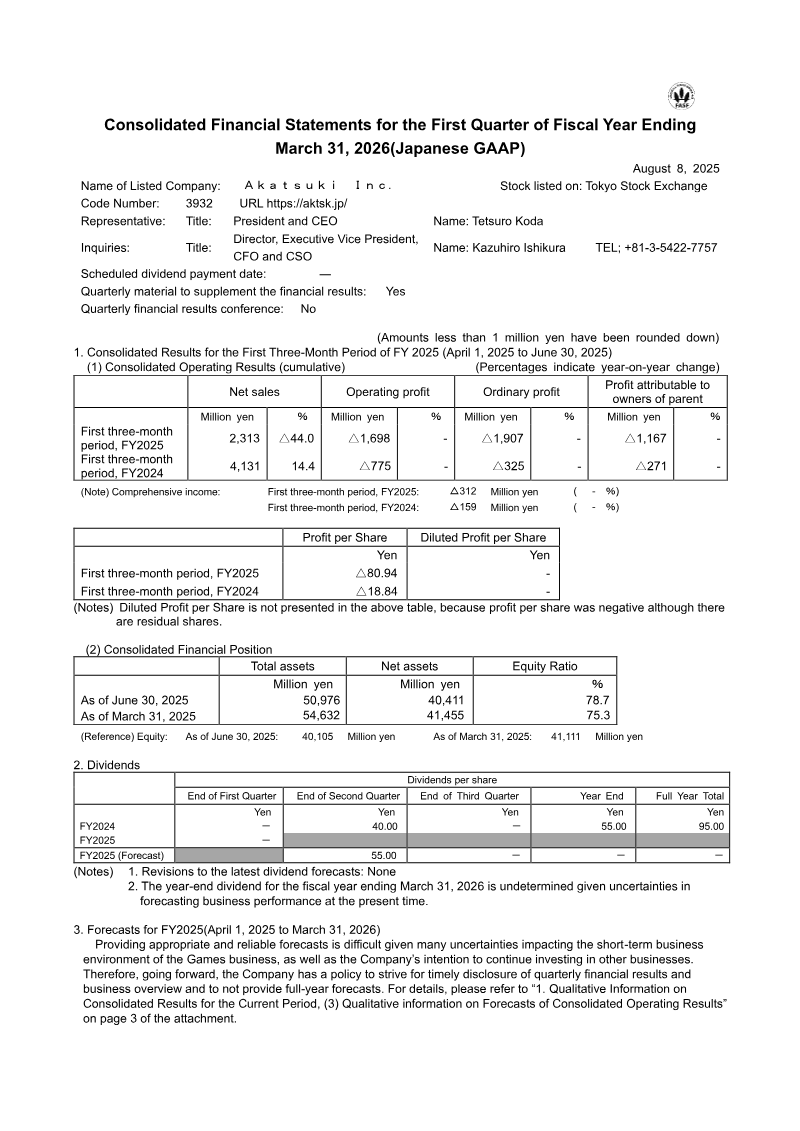

Akatsuki Inc. reported a 44.0% year-on-year decline in net sales to ¥2,313 million for Q1 of the fiscal year ending March 31, 2026, resulting in a net loss of ¥1,167 million.

See it on page 4The Games business segment drove the downturn with a 52.3% revenue drop to ¥1,782 million and a segment loss of ¥1,643 million, largely due to a strategic portfolio review and transitions for flagship titles like Dragon Ball Z Dokkan Battle.

See it on page 4The company recorded a ¥103 million extraordinary loss attributed to the discontinuation of a specific game title and associated organizational restructuring.

See it on page 9The IP Solutions segment emerged as a growth driver, increasing revenue by 167.2% to ¥298 million and generating a segment profit of ¥122 million following the consolidation of CRAYON, Inc.

See it on page 5The Comics business returned to a segment profit of ¥20 million despite an 18.3% year-on-year decline in revenue.

See it on page 4Despite a total asset decrease of ¥3,656 million, the company maintains a stable financial position with an equity ratio of 78.7%.

See it on page 1Strategic focus is shifting toward large-scale, 3D multi-device projects for global markets to reduce reliance on traditional mobile constraints.

See it on page 4Akatsuki Inc. experienced a significant downturn in financial performance during the first quarter of the fiscal year ending March 31, 2026, characterized by a 44.0% year-on-year decline in net sales to ¥2,313 million. This contraction led to a widened operating loss of ¥1,698 million and a net loss of ¥1,167 million. The primary driver of this decline was the Games business, where revenue plummeted 52.3% to ¥1,782 million. This segment’s performance was impacted by a strategic portfolio review and a transition period for flagship titles such as Dragon Ball Z Dokkan Battle, resulting in a segment loss of ¥1,643 million. Furthermore, the company recorded a ¥103 million extraordinary loss stemming from the discontinuation of a specific game title and subsequent organizational restructuring.

Despite these challenges in the core gaming sector, the newly reclassified IP Solutions segment emerged as a growth driver, with revenue increasing 167.2% to ¥298 million and achieving a segment profit of ¥122 million following the consolidation of CRAYON, Inc. Conversely, the Comics business saw an 18.3% revenue decline, though it successfully returned to a modest segment profit of ¥20 million. Total assets decreased by ¥3,656 million during the period, settling at ¥50,976 million, yet the company maintains a robust financial foundation with a high equity ratio of 78.7%.

The current strategic trajectory involves a pivot toward large-scale, 3D multi-device projects designed for global markets. This shift aims to stabilize the Games segment by moving beyond traditional mobile constraints while leveraging the momentum found in IP-driven solutions. While the immediate financial results reflect the costs of reorganization and the volatility of existing game lifecycles, the emphasis remains on long-term scalability and the diversification of revenue streams across the broader entertainment landscape.