Back to Writers

PCF Group

Game Co.

601 documents

Documents

Report

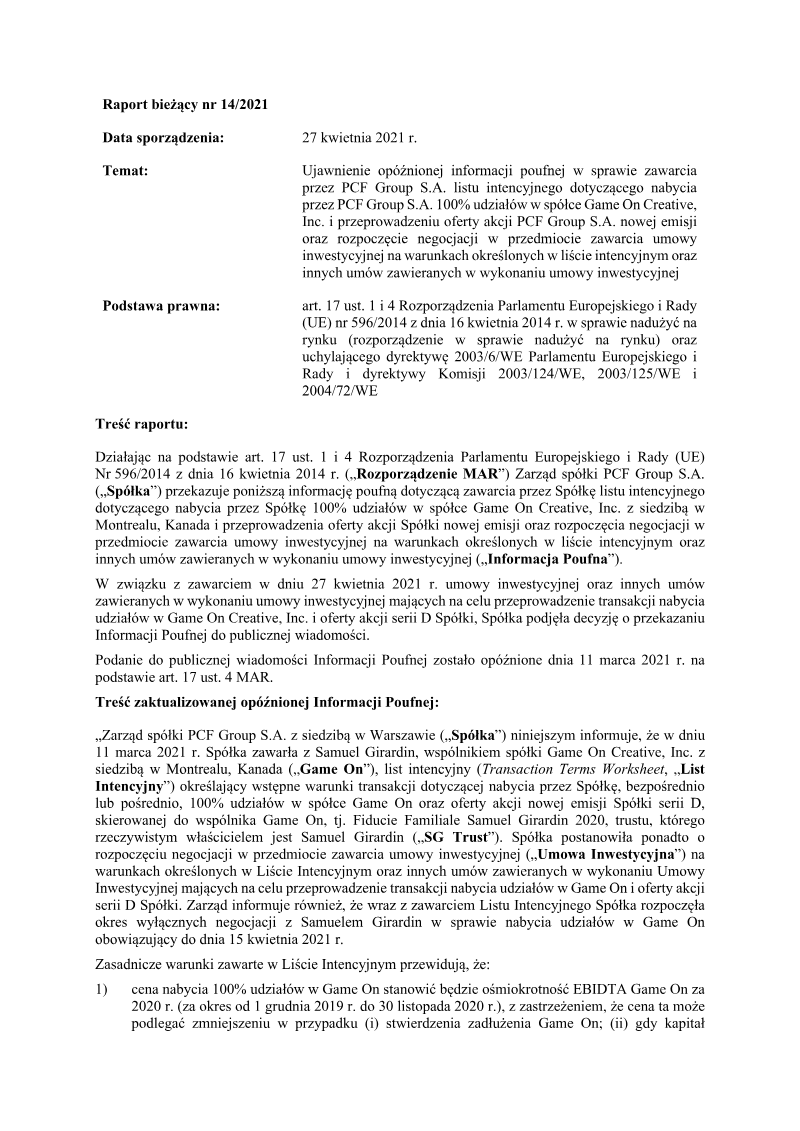

List of Proposed Amendments to the Statutes: PCF Group S.A.

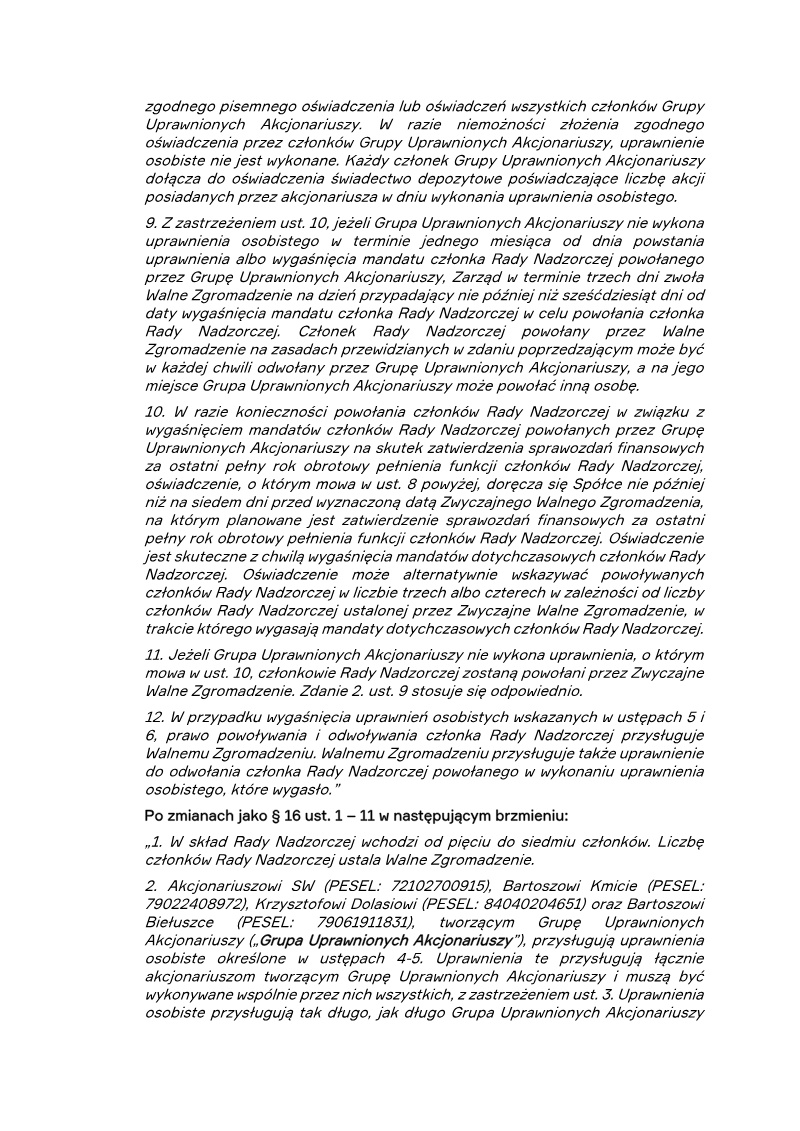

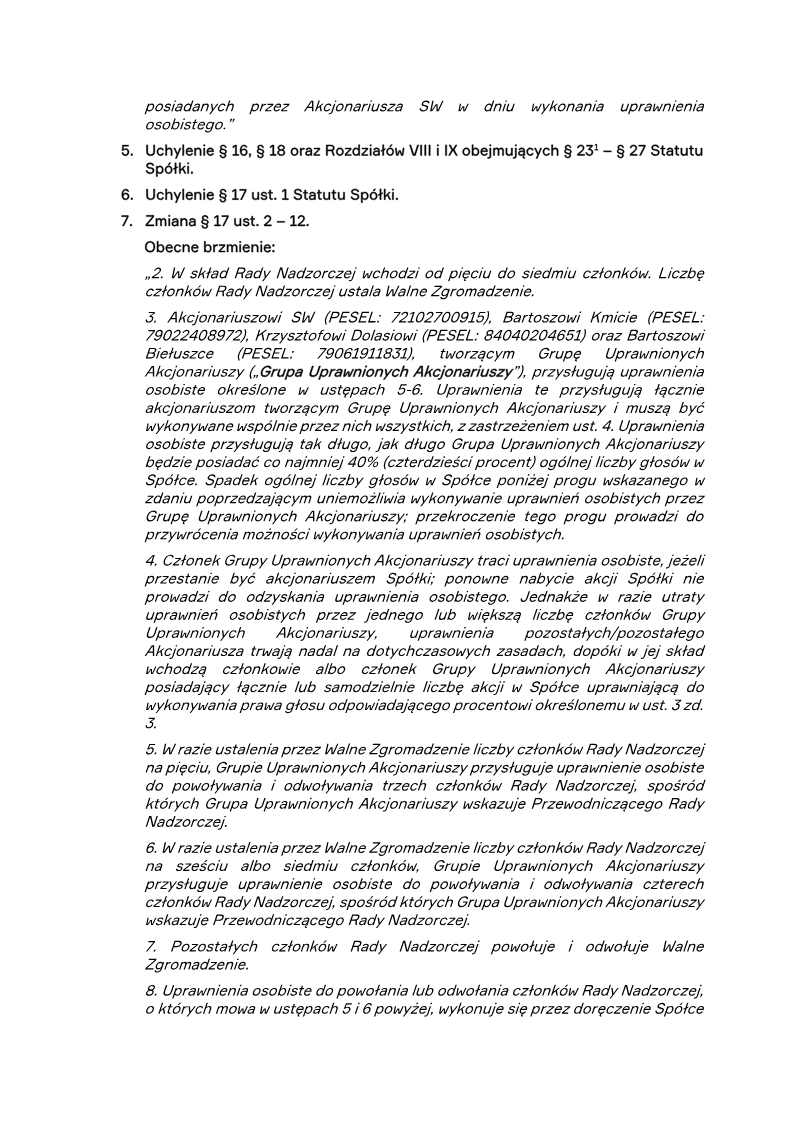

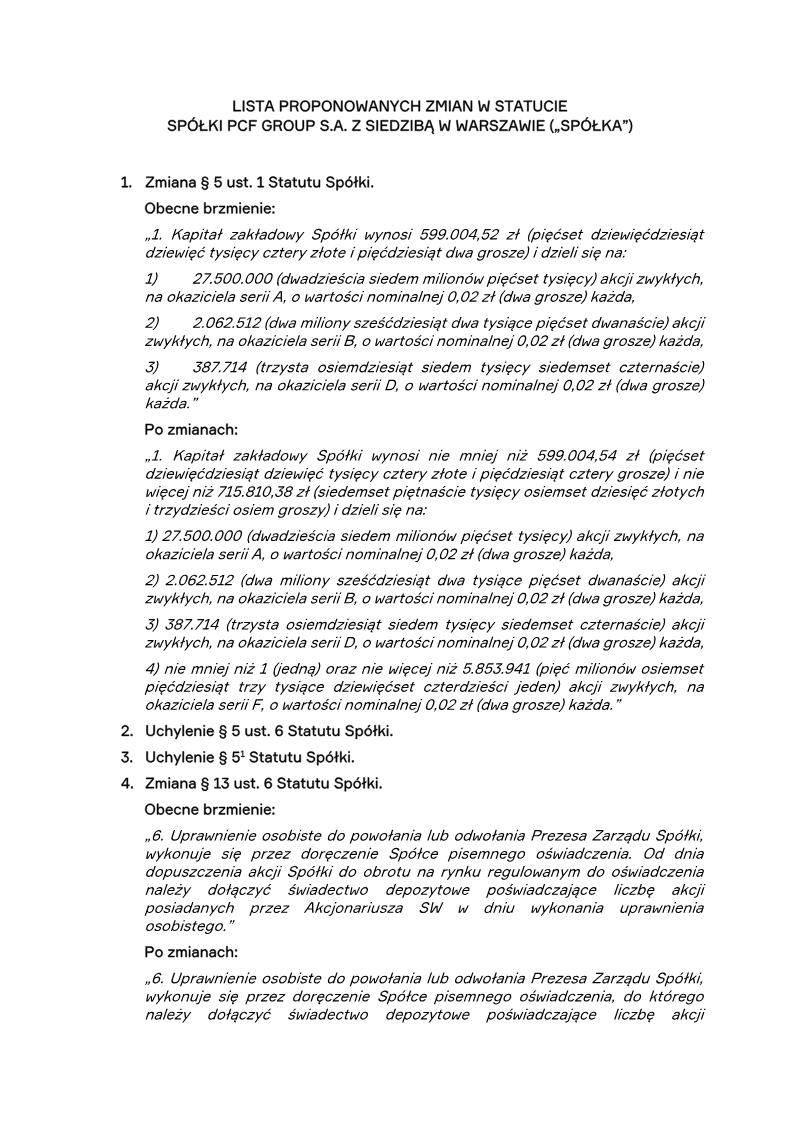

The proposed amendments to the statutes of PCF Group S.A., a Warsaw‑based company, aim to revise capital structure limits, governance provisions, and audit committee requirements. Capital changes set a minimum of PLN 599,004.54 and a maximum of PLN 715,810.38 for the share capital, while maintaining existing share series A (27,500,000 shares), B (2,062,512 shares), D (387,714 shares) and adding a new series F with a range of 1 to 5,853,941 shares. The amendments eliminate several statutory paragraphs (e.g., § 5 6, § 1, §§ 16, 18, and chapters VIII‑IX) and modify others to streamline shareholder rights. Key governance adjustments introduce a “Group of Qualified Shareholders” comprising four named individuals, granting them collective personal rights to appoint or dismiss board members. The group’s authority depends on holding at least 40 % of voting rights and is exercised through joint written declarations accompanied by deposit certificates. If the group fails to act within a month, the board may be appointed by ordinary shareholders; if the group’s rights lapse, ordinary shareholders regain full appointment powers. The amendments also refine board composition rules, allowing five to seven members and specifying the number of directors the group can influence based on board size. Audit and supervisory provisions are tightened to align with public interest entity standards. The company must maintain at least two independent board members and, upon admission to a regulated market, establish an audit committee with a majority of independent members. These changes ensure compliance with Polish public‑interest entity regulations and enhance shareholder influence over board composition while clarifying audit oversight responsibilities.

PCF Group

Report

Raport z przeglądu skróconego śródrocznego skonsolidowanego sprawozdania finansowego: H1 2025

The review confirms that the consolidated interim financial statements for PCF Group Spółka Akcyjna, covering the period from 1 January to 30 June 2025, have been prepared in accordance with International Financial Reporting Standard 34 for interim reporting as adopted by European Union regulations. No material misstatements or omissions were identified during the review, which was conducted in accordance with Polish Standard 2410 (the local equivalent of International Standard on Review Engagements). The review involved inquiry procedures directed at financial and accounting personnel, analytical procedures, and other review activities. Because the scope of a review is narrower than that of an audit, no assurance is provided beyond the conclusion that nothing has come to the reviewers’ attention that would lead them to believe the statements are not prepared in all material respects. Key disclosures highlighted include a valuation test for a cash‑generating unit related to capitalised development costs for a new game, with uncertainties noted regarding the assumptions underpinning projected cash flows and actual sales under an early‑access model. Additionally, a deferred tax asset of PLN 53,543 thousand is subject to uncertainty due to potential changes in the group’s tax‑profit forecasts over a five‑year horizon, reflecting doubts about the feasibility of current strategic plans. No modifications to these disclosures were recommended by the reviewers. The review covers the entire PCF Group, headquartered in Warsaw, and was completed on 30 September 2025 by Grant Thornton Polska Prosta Spółka Akcyjna, a member of the Grant Thornton International network.

PCF Group