Back to Writers

Koei Tecmo

Game Co.

212 documents

Japanese developer/publisher. Dynasty Warriors, Nioh, Dead or Alive, Atelier, Romance of the Three Kingdoms.

Documents

Report

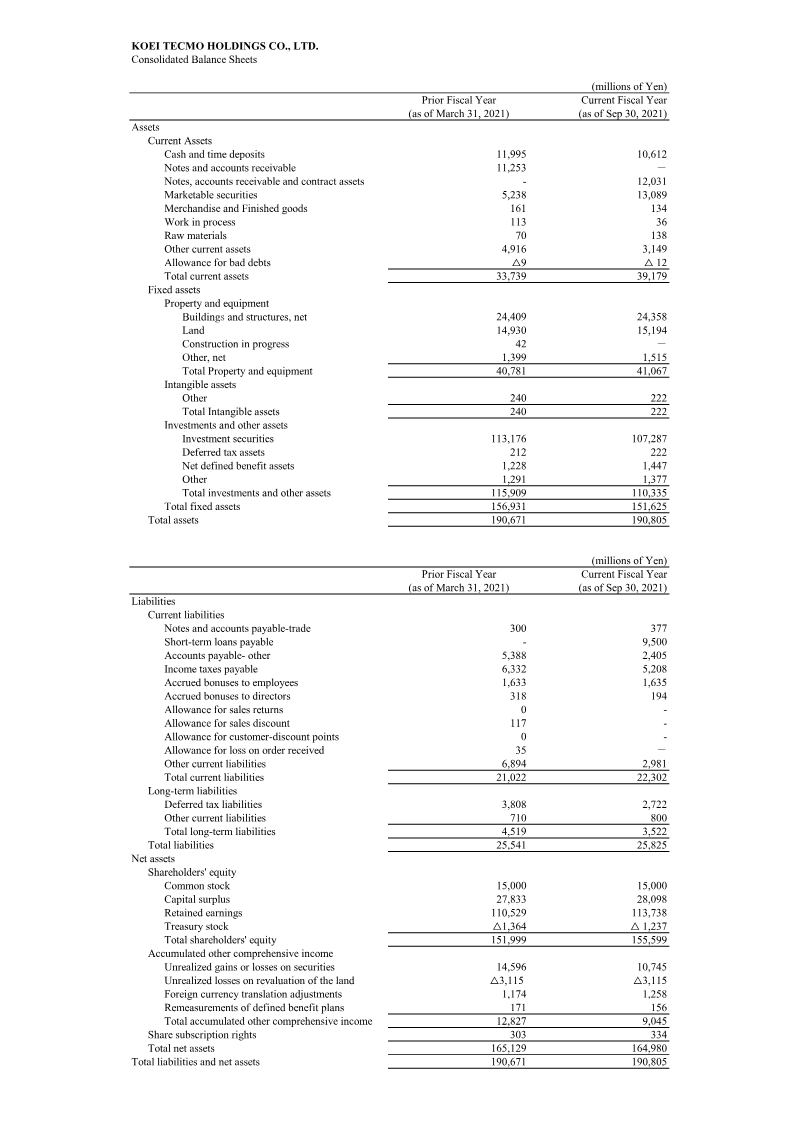

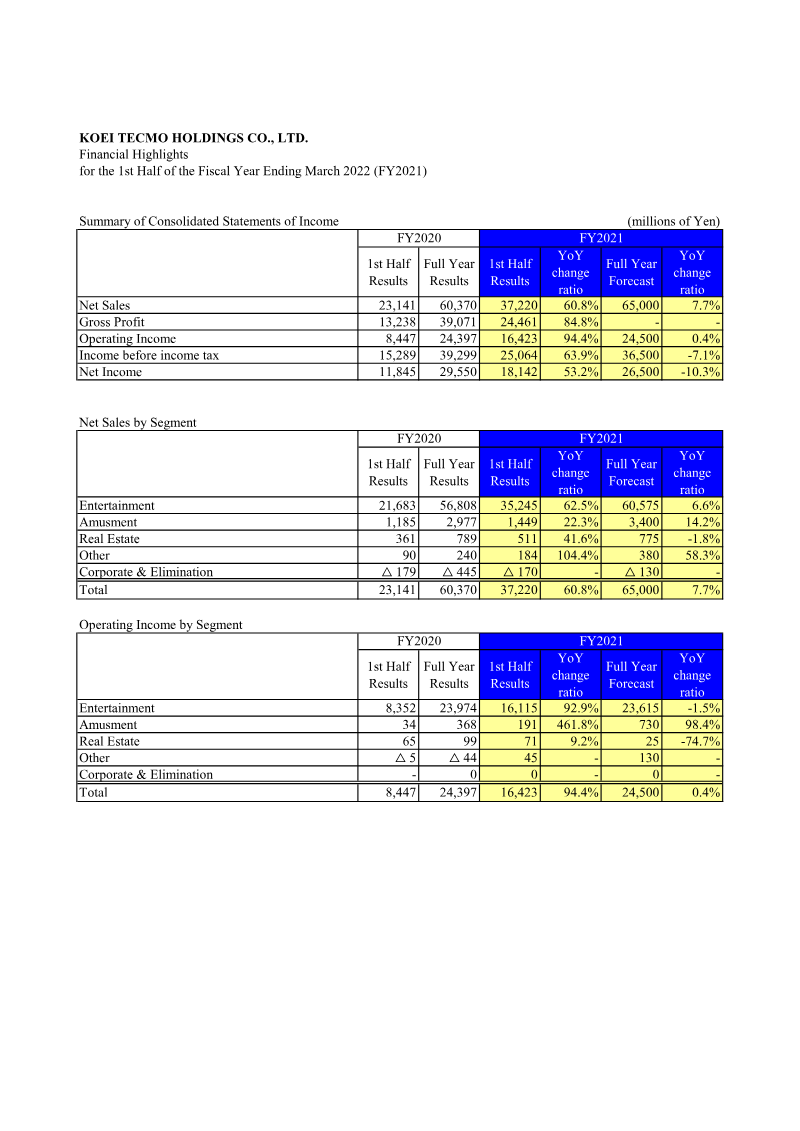

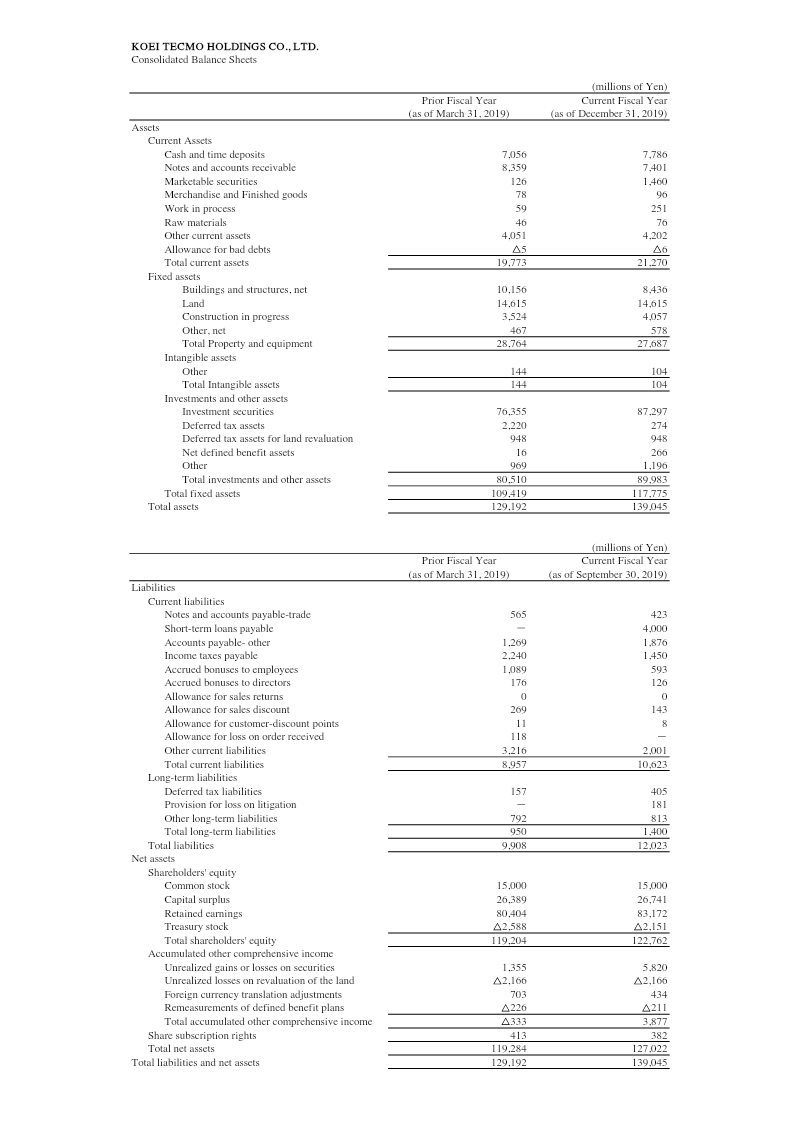

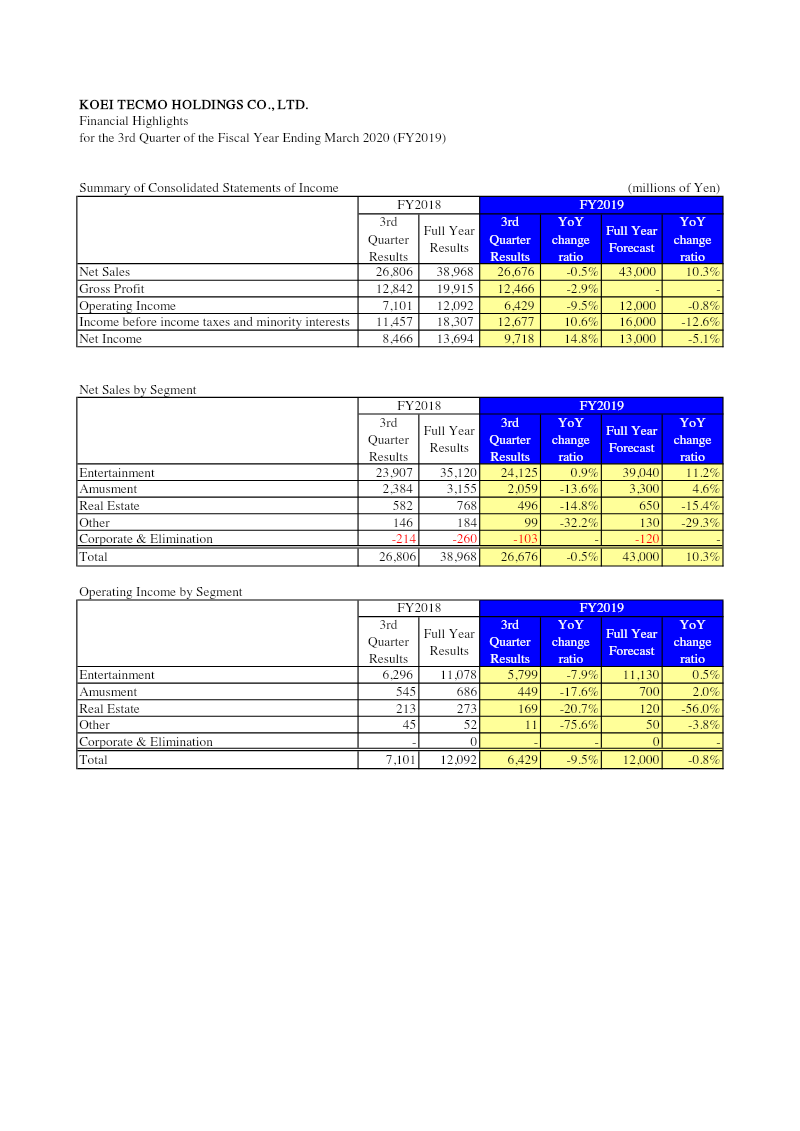

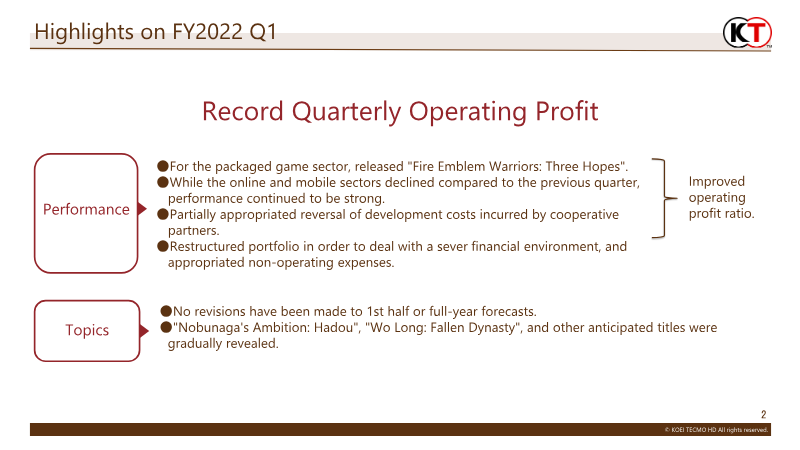

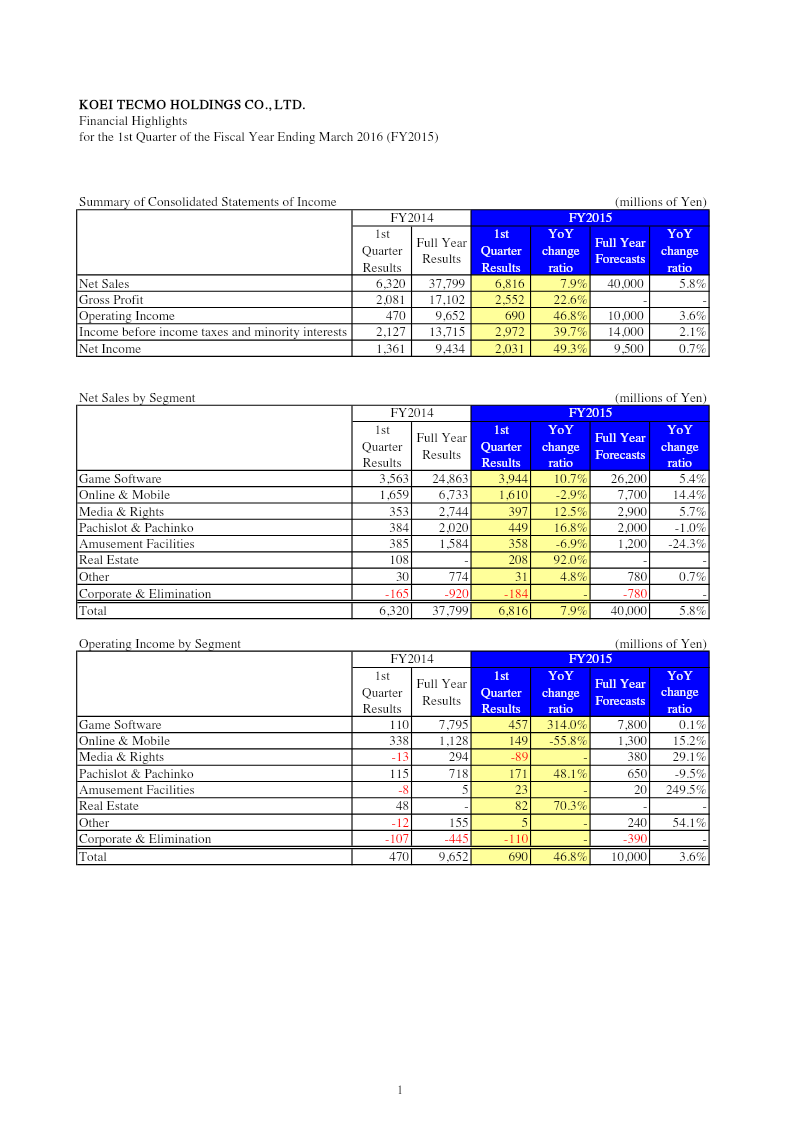

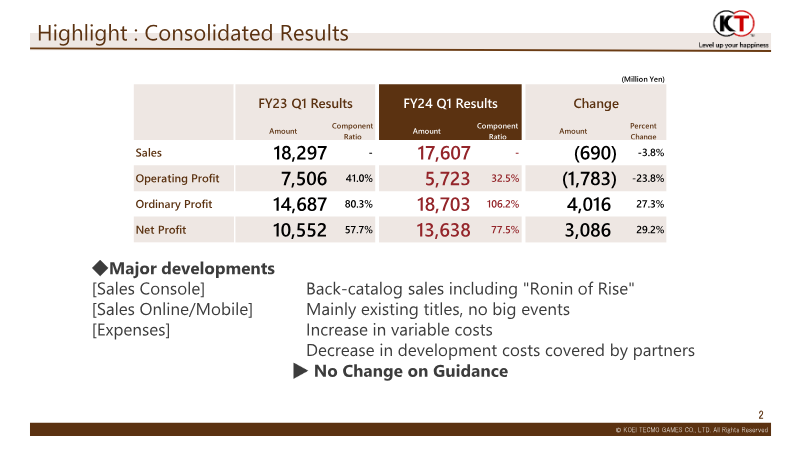

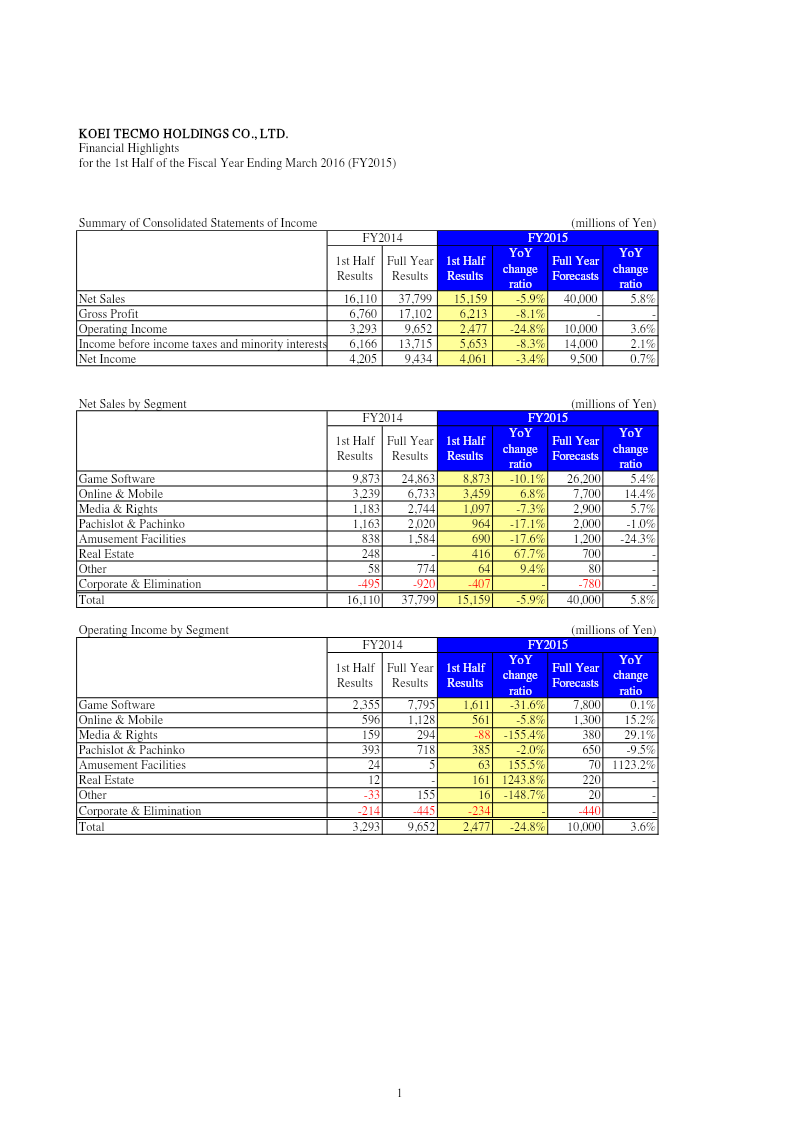

Financial Highlights: 1st Half of the Fiscal Year Ending March 2016

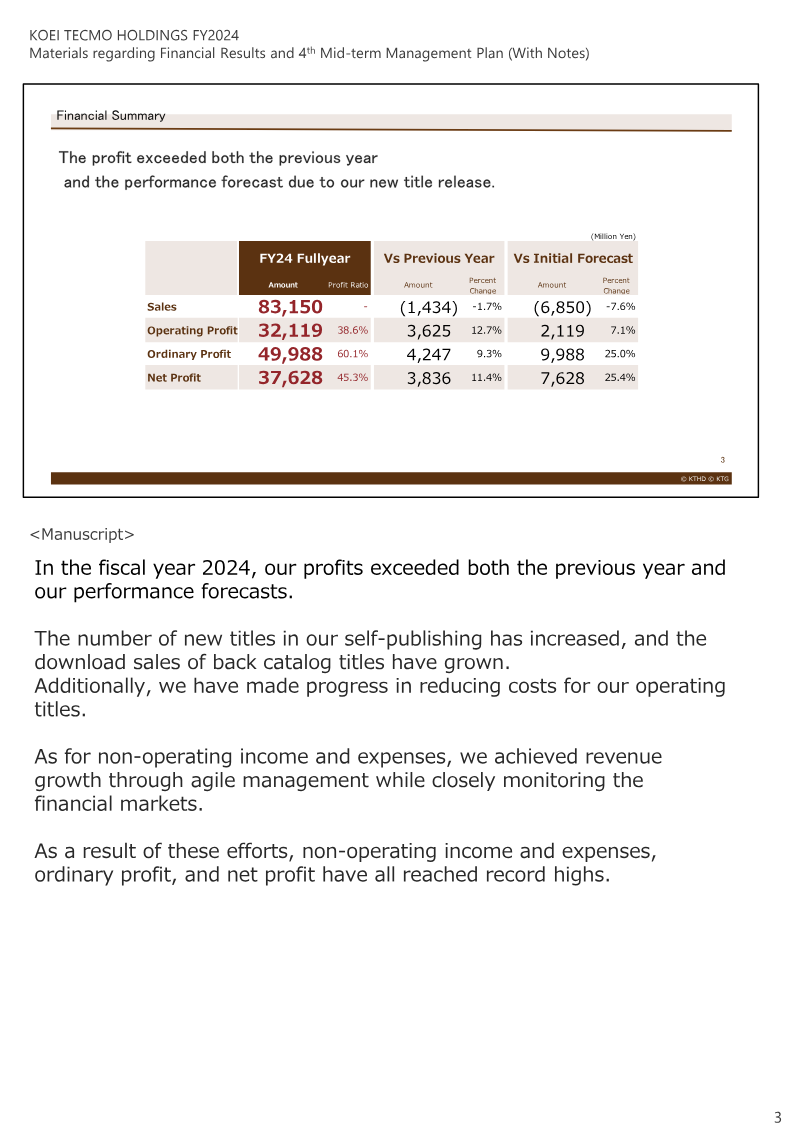

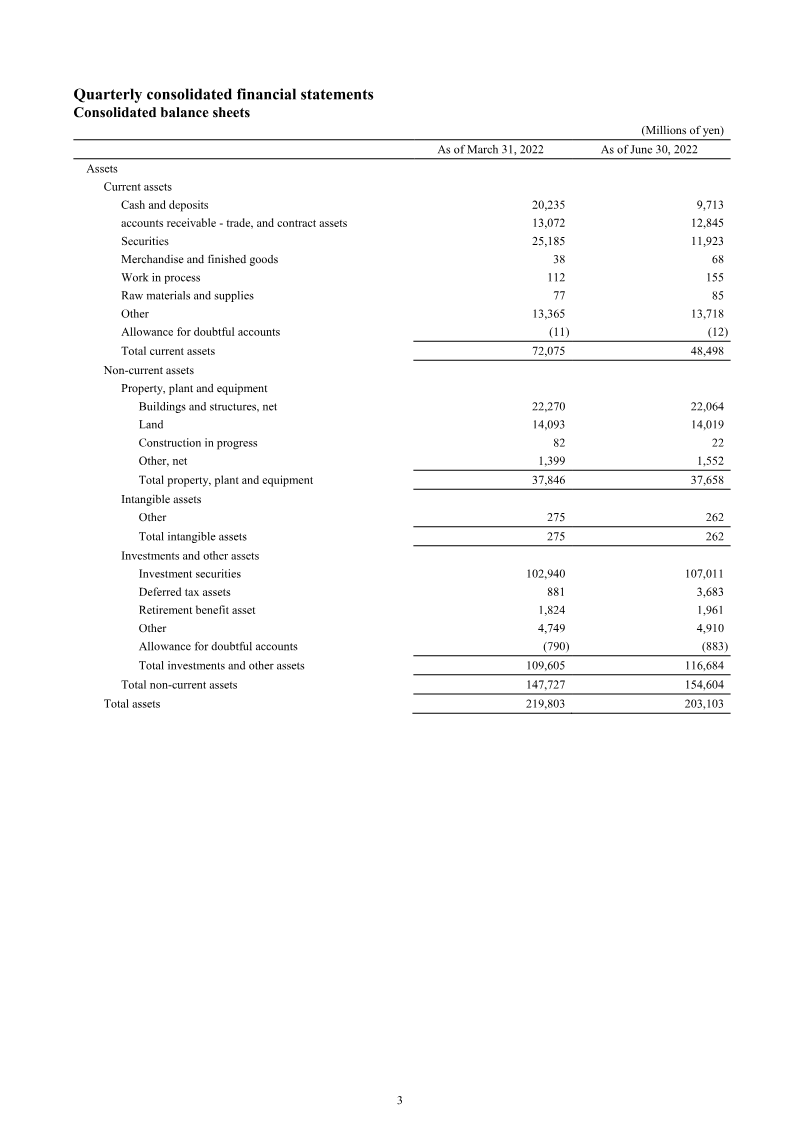

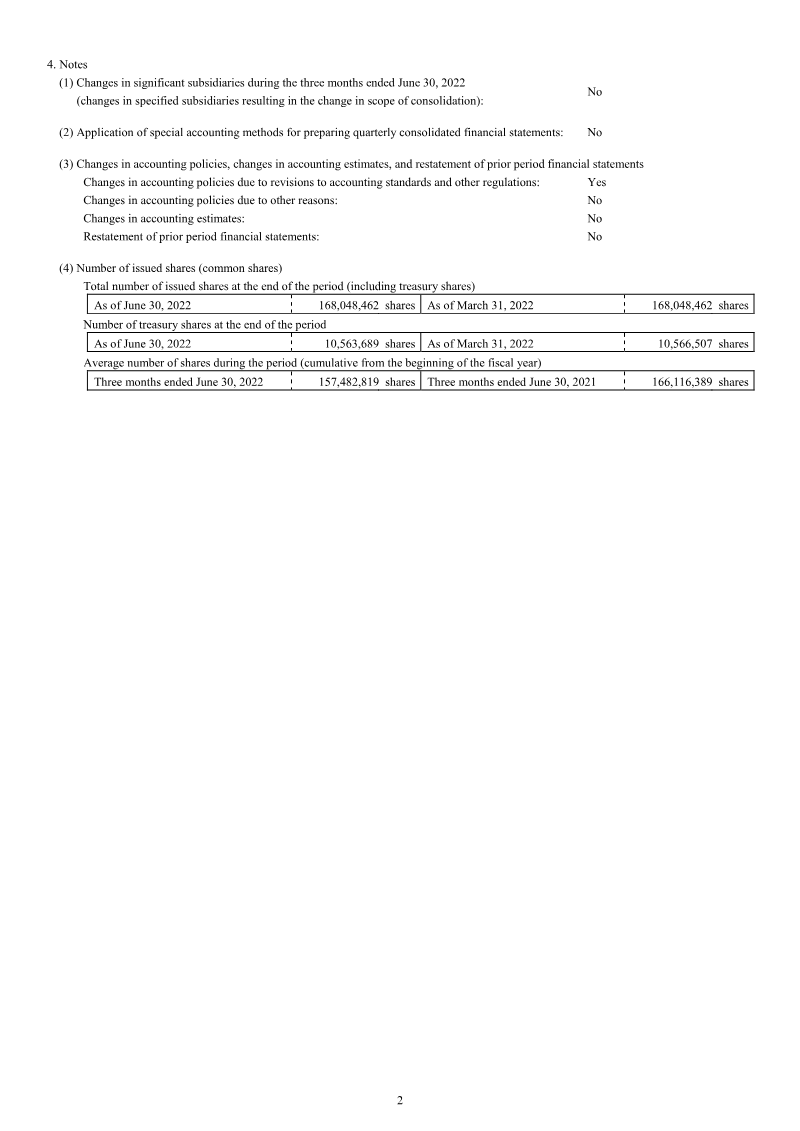

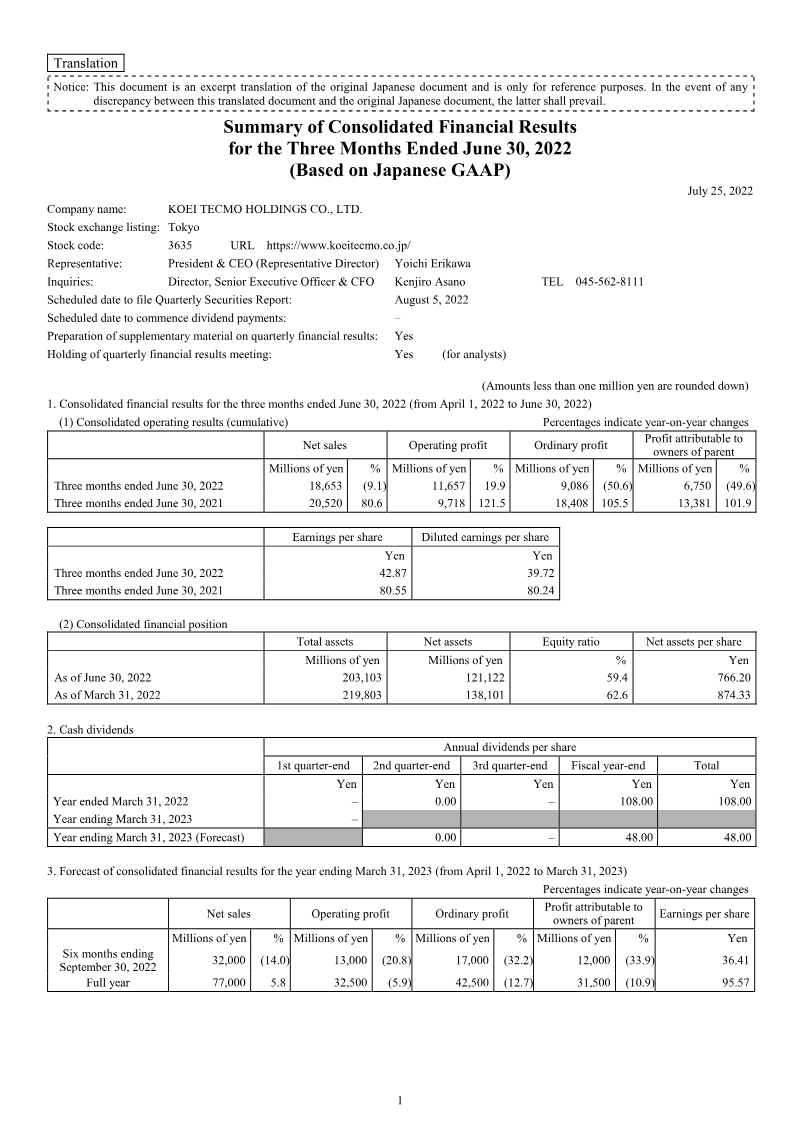

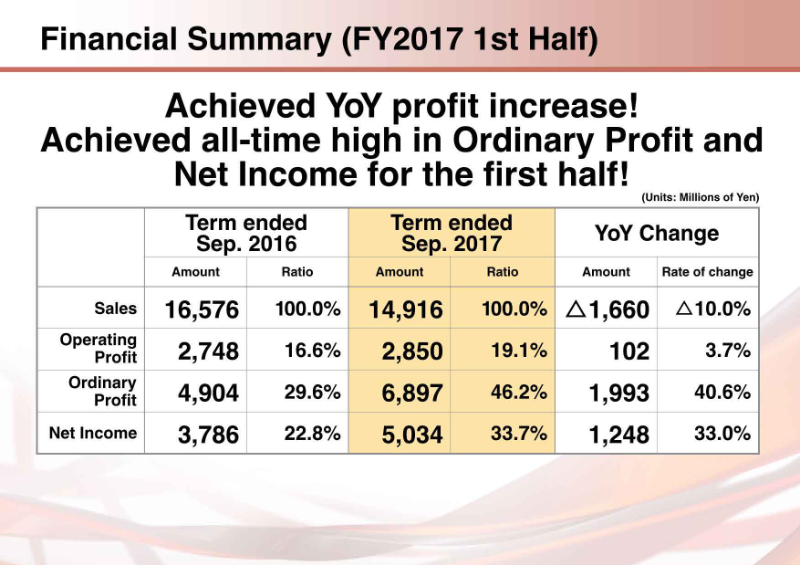

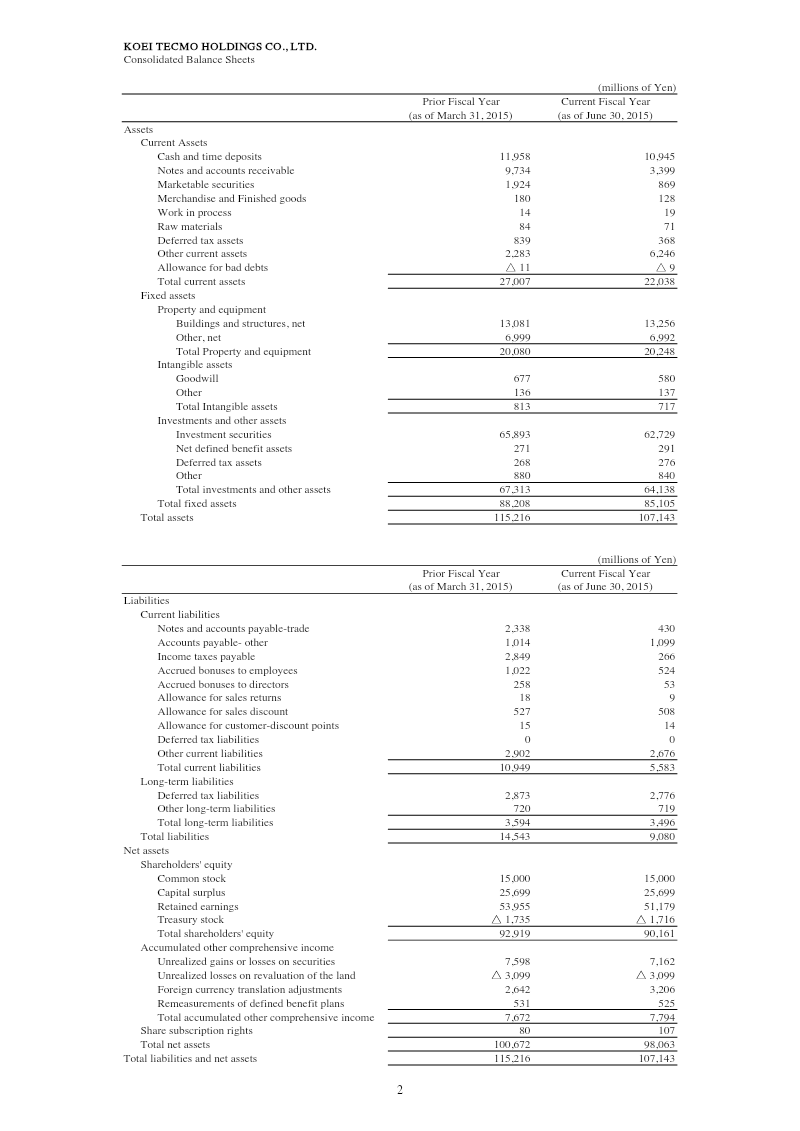

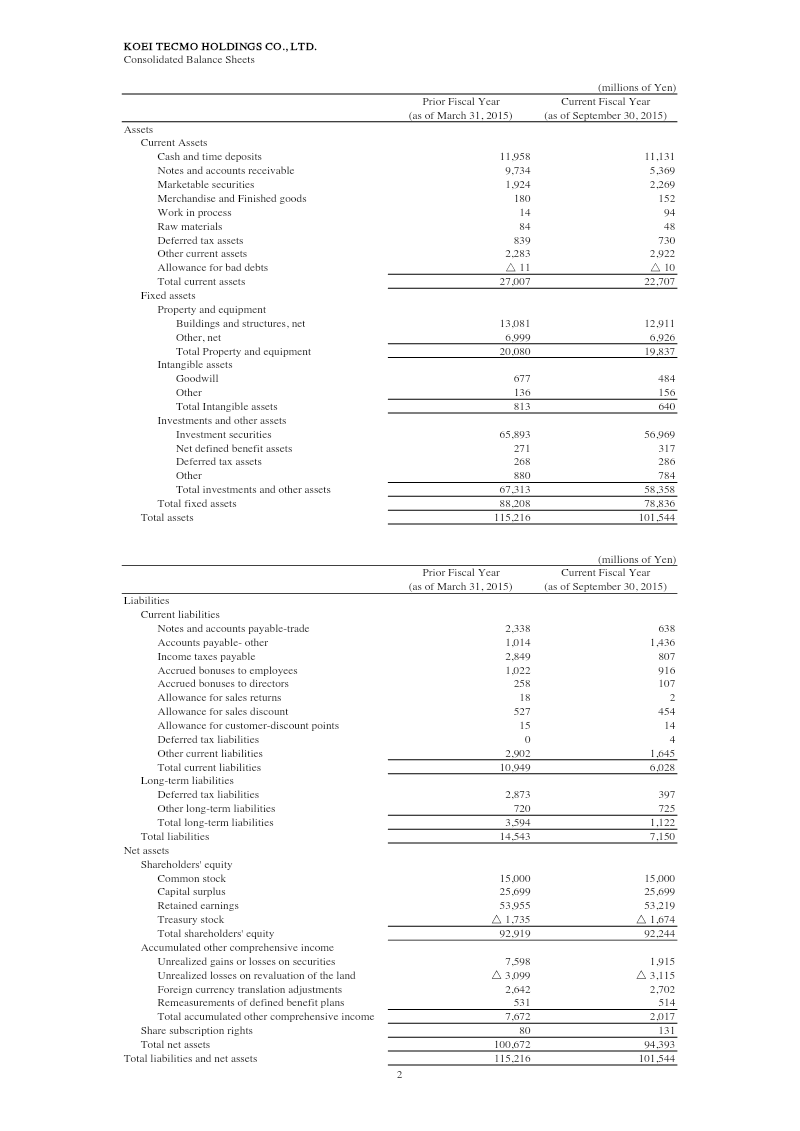

Koei Tecmo Holdings reported its first‑half financial results for the fiscal year ending March 2016, showing a 5.9 % decline in net sales to ¥37.8 billion compared with the same period a year earlier, while full‑year sales are projected to rise 5.8 % to ¥40 billion. Gross profit fell 8.1 % to ¥17.1 billion, and operating income dropped 24.8 % to ¥9.7 billion; net income decreased 3.4 % to ¥9.4 billion, reflecting a modest 0.7 % increase over the full‑year forecast of ¥9.5 billion. Segment analysis indicates that Game Software sales declined 10.1 % to ¥24.9 billion, whereas Online & Mobile sales grew 6.8 % to ¥6.7 billion, and Media & Rights sales rose 5.4 % to ¥26.2 billion. Pachislot & Pachinko and Amusement Facilities segments experienced sharp declines of 17.1 % and 17.6 %, respectively, while Real Estate sales increased 67.7 %. Operating income was strongest in Game Software (¥7.8 billion) and Online & Mobile (¥1.3 billion), with Media & Rights showing a 155.4 % decline. Balance‑sheet highlights show total assets reduced from ¥115.2 billion to ¥101.5 billion, largely due to a drop in investment securities and current assets. Current liabilities fell from ¥10.9 billion to ¥6.0 billion, and long‑term liabilities decreased from ¥3.6 billion to ¥1.1 billion, improving liquidity and leverage ratios. Shareholders’ equity remained stable at ¥92.2 billion, with retained earnings slightly lower. The company’s financial position remains solid, though operating performance is pressured by declines in core gaming and amusement segments.

Koei Tecmo

Report

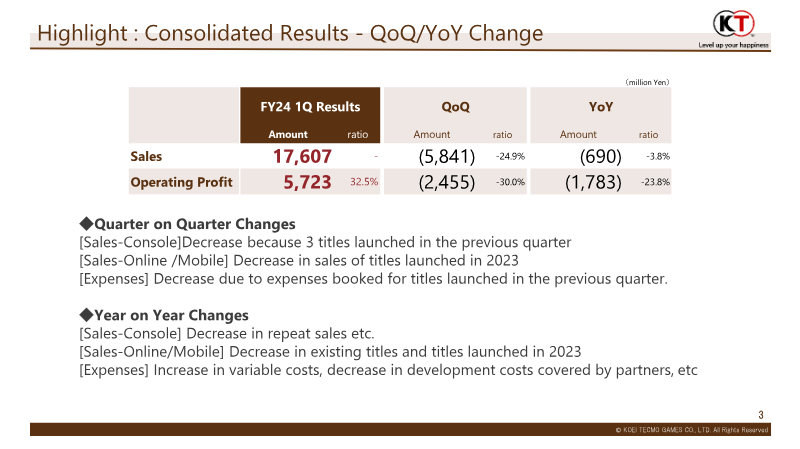

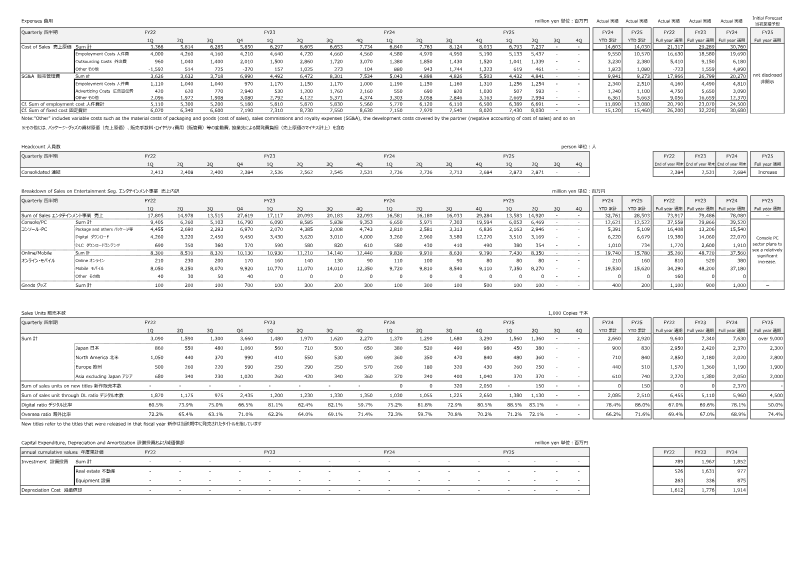

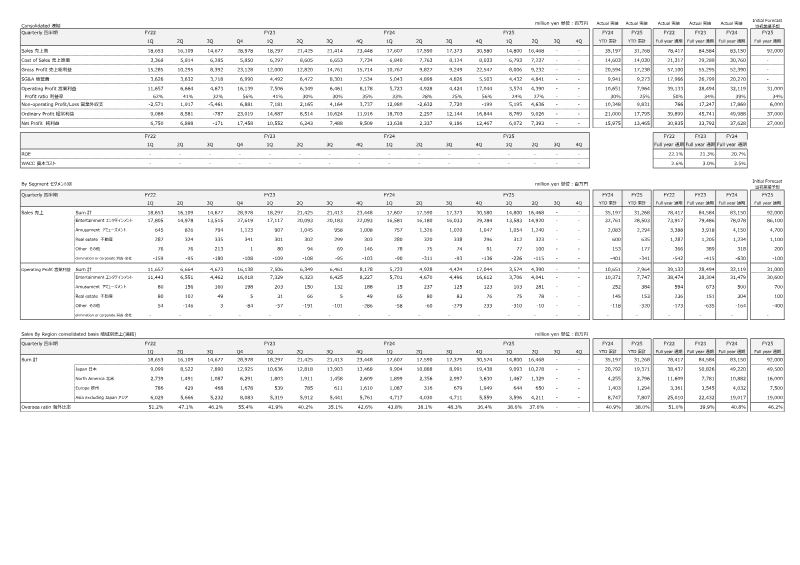

Consolidated Financial Results: FY2025 2nd Quarter Data Appendix

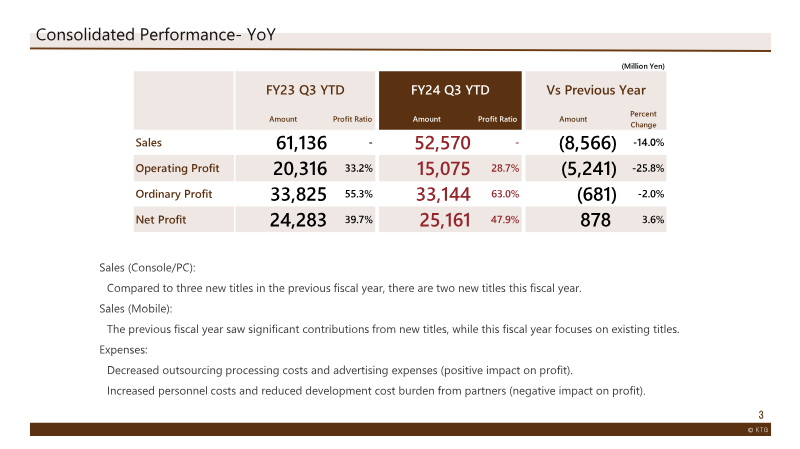

The consolidated financial appendix presents quarterly and annual performance for FY22 through FY25, focusing on sales, cost of sales, gross profit, SG&A, operating profit, and net profit across entertainment, amusement, real‑estate, and other segments. Sales peaked in FY25 Q4 at ¥28,978 million, driven largely by the entertainment segment (¥27,619 million), while cost of sales rose proportionally, resulting in a gross profit margin decline from 62 % in FY22 Q1 to 30 % by FY25 Q2. Operating profit fluctuated, with a notable dip in FY24 Q3 (¥4,673 million) before rebounding to ¥16,139 million in FY25 Q4. Net profit followed a similar pattern, reaching ¥17,458 million in FY25 Q4 after a negative result in FY24 Q3. Segment analysis shows entertainment consistently dominates revenue, contributing over 90 % of total sales, with amusement and real‑estate providing modest but stable contributions. Geographic revenue distribution indicates Japan remains the largest market (≈49 % of total sales), followed by North America and Asia excluding Japan, with overseas ratios ranging from 35 % to 55 %. Headcount grew from 2,413 employees in FY22 Q1 to 2,873 by FY25 Q4, reflecting expansion. Capital expenditure totals ¥789 million in FY22 and increased to ¥1,967 million in FY24, with real‑estate and equipment investments comprising the bulk. Digital sales maintain a high digital ratio (≈70 %) and online/mobile units account for 60–80 % of total sales units, underscoring a strategic shift toward digital platforms. Overall, the data illustrate robust revenue growth driven by entertainment titles, moderate margin compression due to rising costs, and a strategic emphasis on digital distribution across multiple regions.

Koei Tecmo